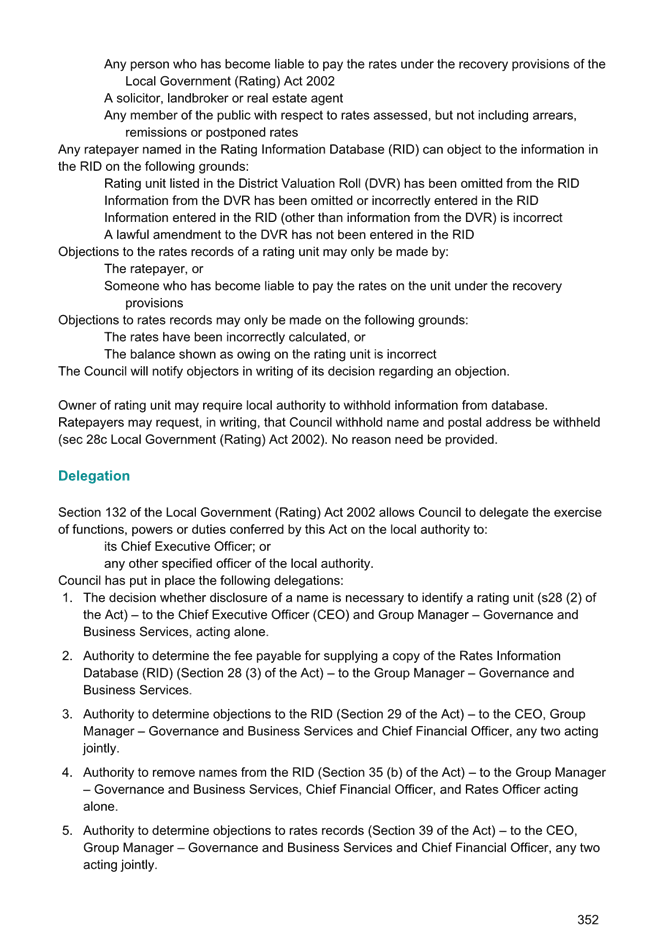

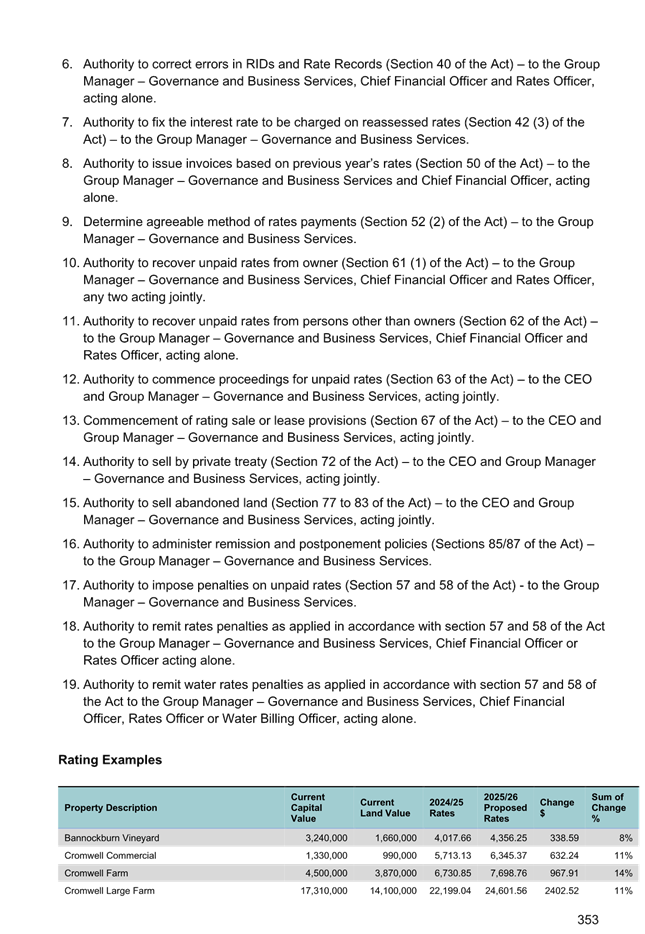

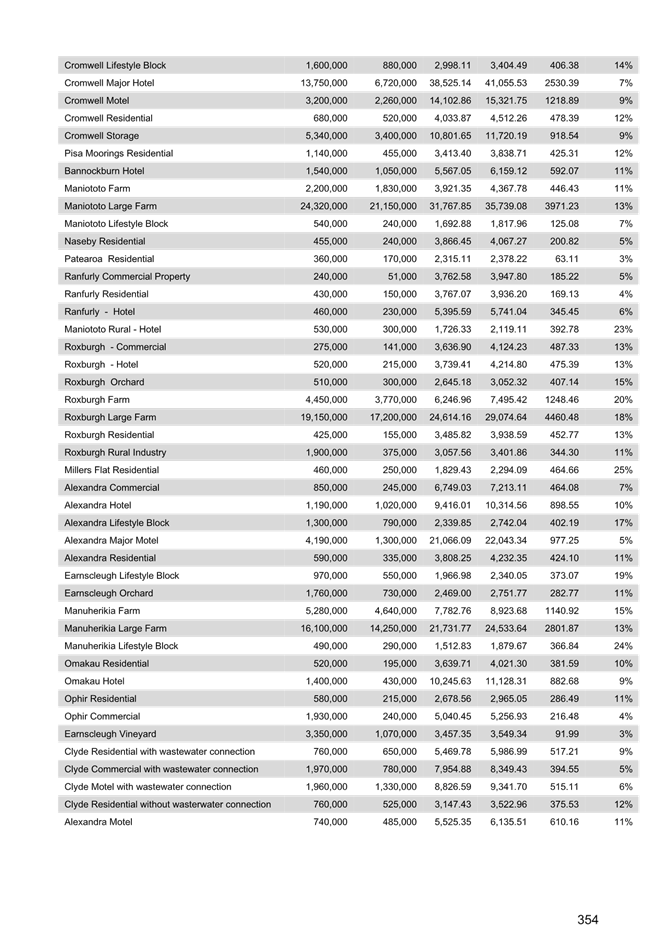

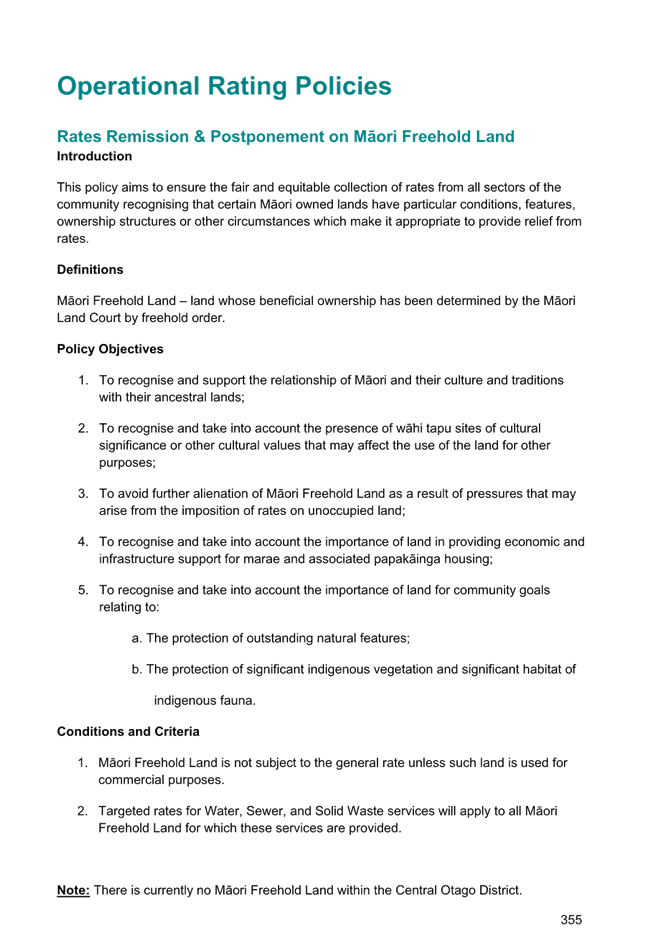

5 Reports

25.13.2 Adoption

of the 2025-34 Long-term Plan

Doc ID: 2497596

|

Report Author:

|

Donna McKewen, Acting Chief

Financial Officer

|

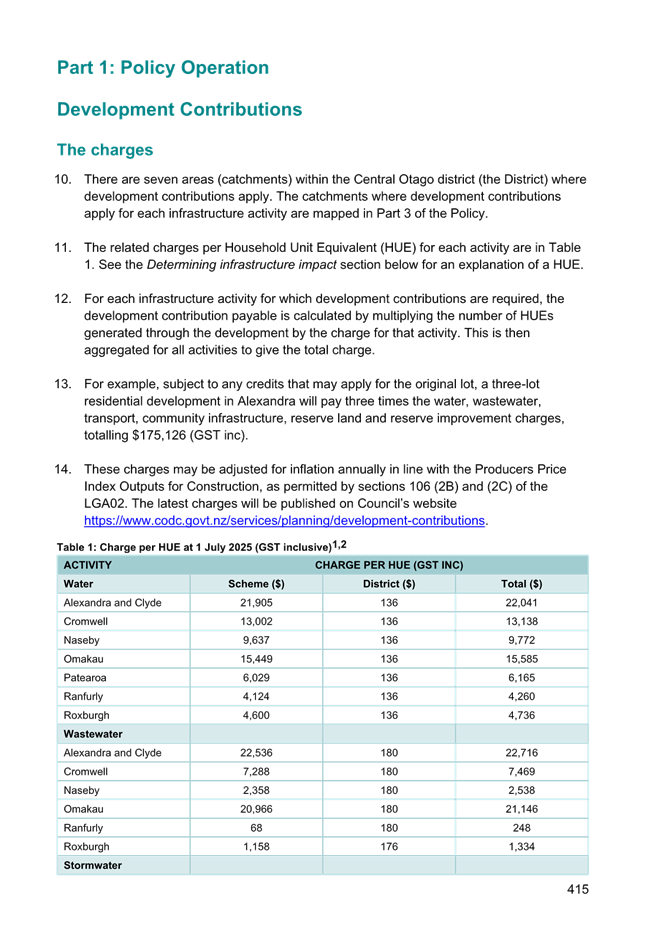

|

Reviewed

and authorised by:

|

Saskia Righarts, Group Manager –

Governance and Business Services

|

1. Purpose

of Report

To adopt the 2025-34

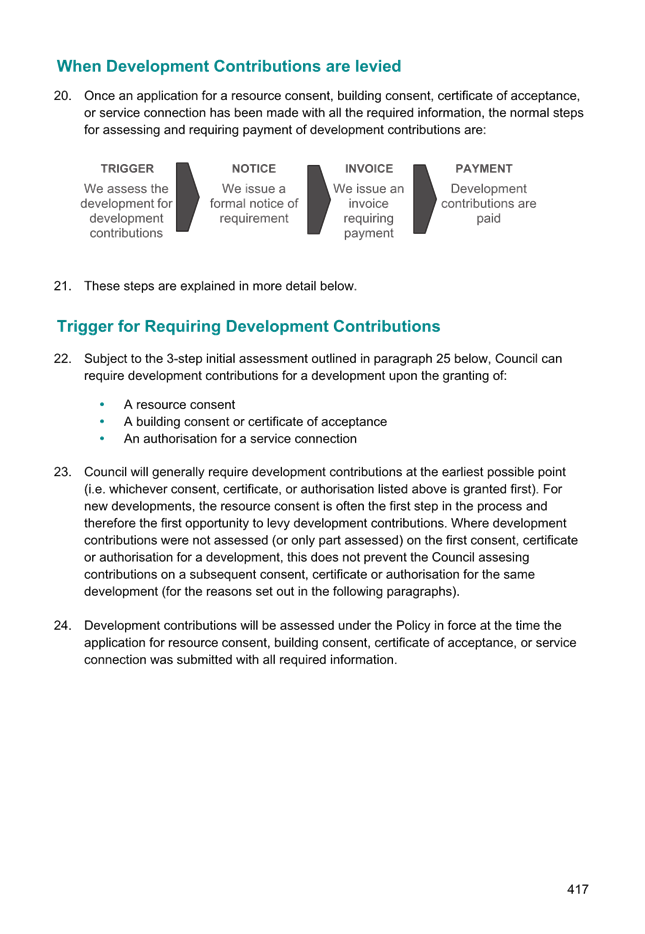

Long-term Plan along with the 2025-26 fees and charges schedule.

|

Recommendations

That the Council

A. Receives

the report and accepts the level of significance.

B. Approves

and adopts the revenue and financing policy 2025-31 for inclusion in the

2025-34 Long-term Plan

C. Approves

the Long-term Plan 2025-34 detailed

in Appendix 1, including the 2025-26 fees and charges as

detailed in Appendix 2

D. Receive

the auditor’s opinion for the 2025-34 Long-term plan

E. Adopts

the 2025-34 Long-term Plan and auditors’ opinion in accordance with Section 95 of the Local Government Act

2002.

F. Requests the Chief Executive Officer to prepare

the final 2025-34 Long-term Plan including any amendments from the Council,

auditors and legal representative.

G. Requests

the Chief Executive Officer to formally advise the submitters of

Council’s decisions.

|

2. Background

The Local Government Act

2002 (S 93 and 93A) requires Council to prepare and adopt a Long-term Plan

(LTP) every three years. Under normal circumstances Council would have prepared

an LTP for adoption 30 June 2024.

Due to the new

Government’s significant policy changes and uncertainty around proposed

delivery of water services (drinking water, wastewater and stormwater), councils

across the country were given the option to delay Long-term Plans by one year

and prepare instead an enhanced Annual Plan. Council took this option. There is

now more clarity on expectations from Government and Council is developing a

plan for delivery of water services. Council’s long-term plan is for nine

years and covers the period from 2025 to 2034 and reflects those changes to the

delivery of water services.

3. Discussion

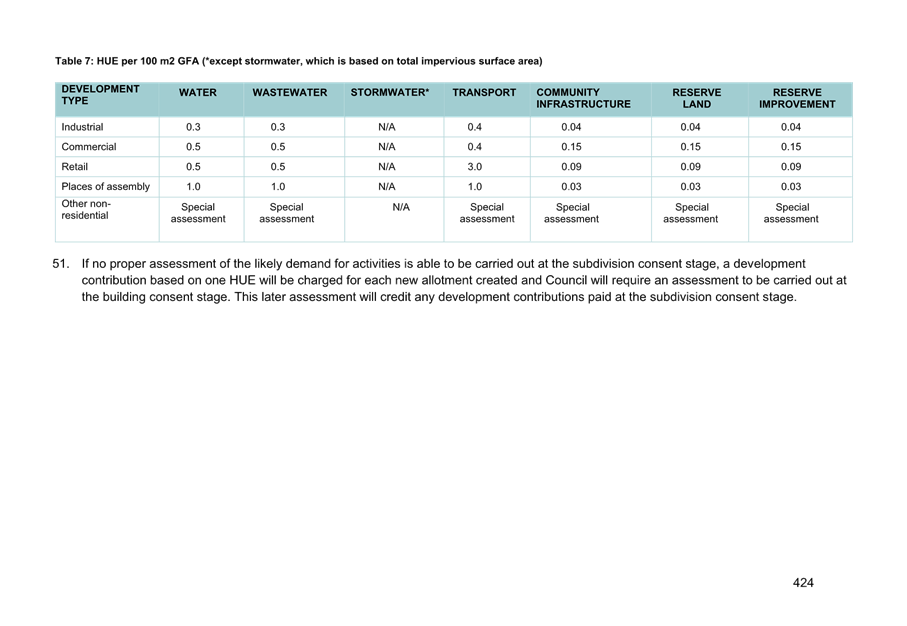

Following the 2025-34

Long-term Plan consultation period the Council met on the 15 May

2025 to listen to submitters that wished to be heard. Overall 903 submissions,

and one staff submission was received. For this Long-term Plan a youth survey

was run, which asked similar questions about the consultation topics. A total

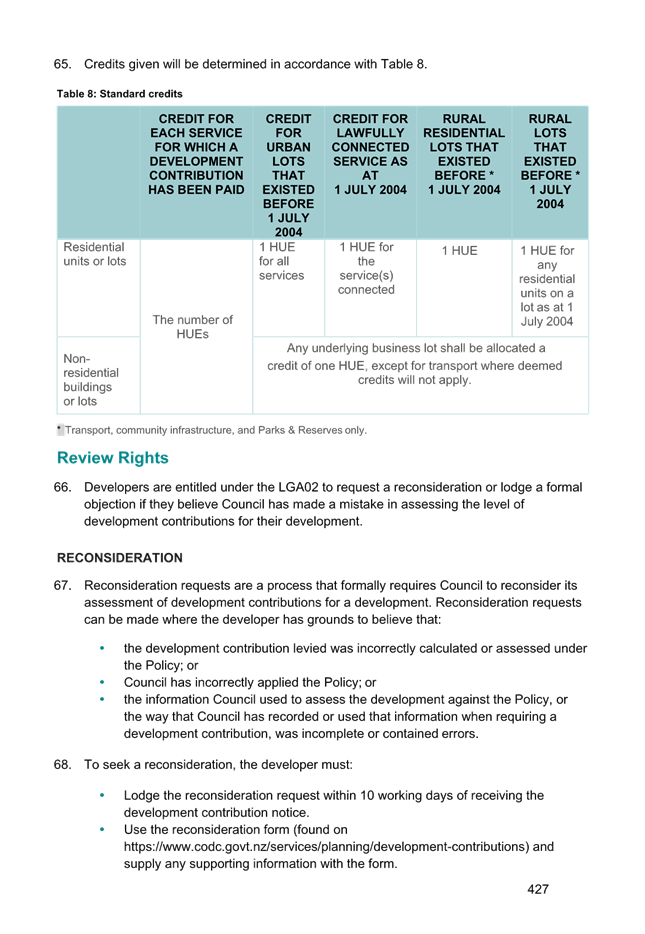

of 313 youth submissions were received.

In the deliberations meeting

held on the 20 May 2025 the councillors reflected on the community’s

feedback on the consultations key issues. As a result the following decisions

were made:

· Volumetric water charge was set at $1.60 per cubic

meter for 2025/26 and then increasing to the proposed $2.40 per cubic meter for

2026/27.

· Community halls and facilities:

o The following halls and facilities to remain under

council ownership: Ophir hall; Poolburn hall; Becks hall; Clyde hall; Clyde

Museum (Blyth st); Clyde Railway station; Millers Flat hall; Ranfurly hall;

Wallace Memorial rooms; Naseby hall; Naseby General Store and Centennial Milk

Bar.

o Fenton Library building to remain under council

control

o The following halls and facilities to be divested

subject to further discussion: Patearoa hall; Waipiata hall and Wedderburn

hall.

o The following halls and facilities to be divested:

Vallance Cottage; Clyde Police Lock Up; Briar Herb Museum and Cottage; Clyde

Goods Shed; Millers Flat Bowling club and Roxburgh Squash club.

o The old Alexandra Riding for the Disabled building to

be demolished.

o The Ranfurly Service Centre to be divested as part of

the Long-term Plan 2027-37.

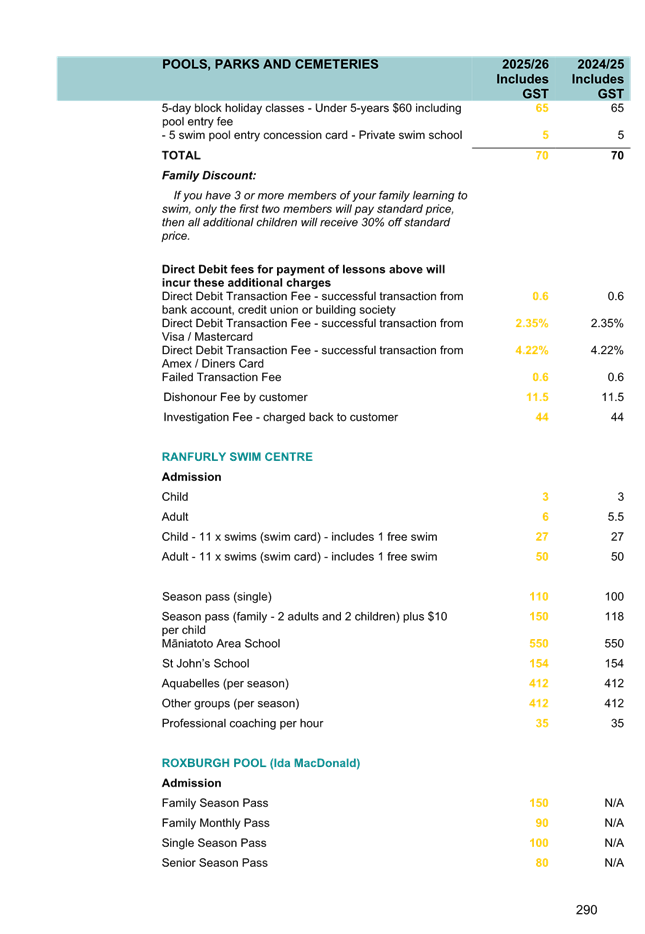

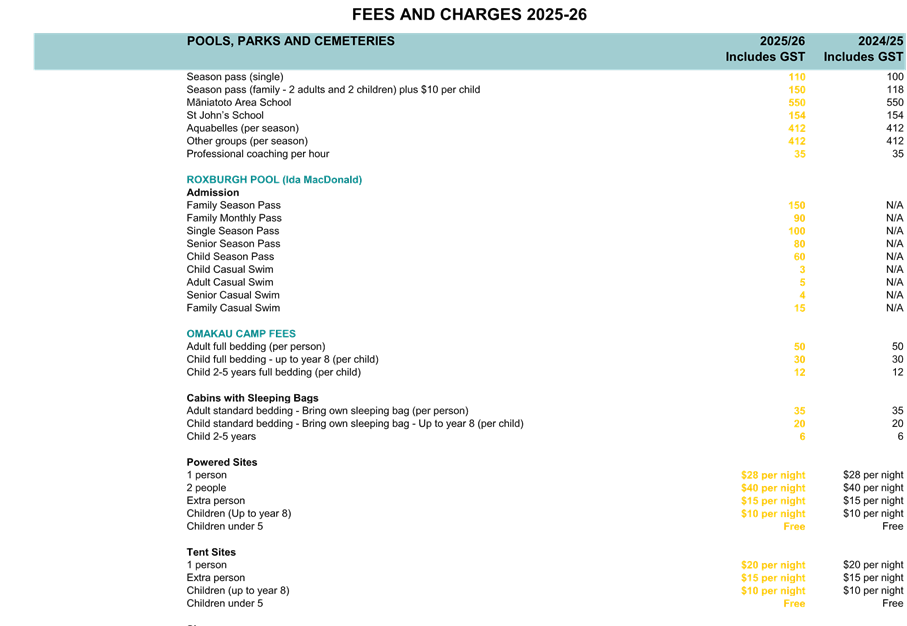

· Agreed to accept the Ida MacDonald Roxburgh Pool

Punawai Ora to be vested to Council.

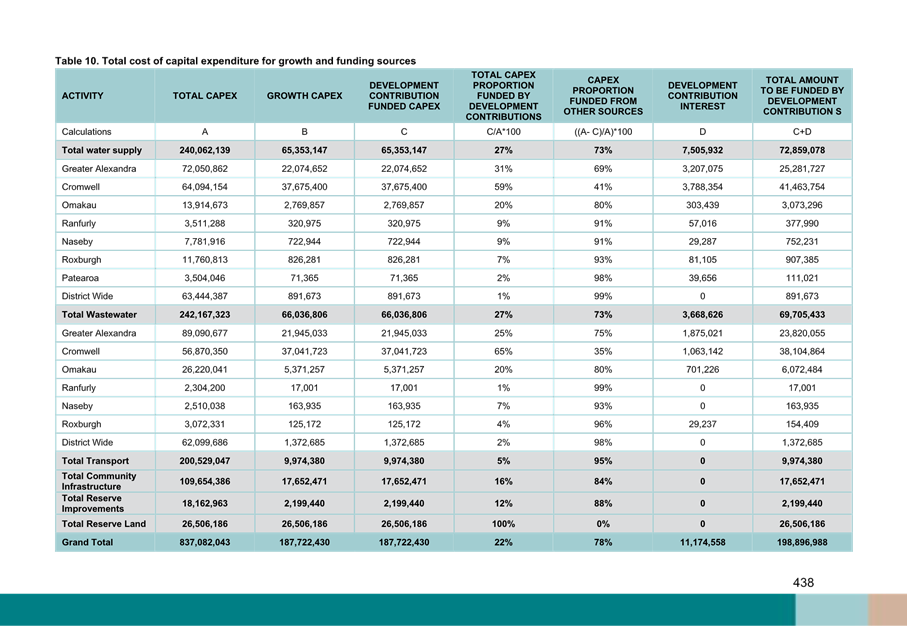

· Agreed to retain the Alexandra outdoor pool with

further review in the 2027-37 Long-term plan.

· Agreed to fund up to $1.6M of additional funding for

the completion of the Manuherekia Valley Community Hub.

· On the basis that there is no offer for Central Otago

to host a South Island supercars event no funding is to be allocated.

· Agreed to support both the Dunstan High School and

Maniototo Area School artificial turf grants.

· Agreed to continue investigation a joint CCO model for

water services delivery.

· Agreed to allocate income from mining agreements with

Hawkwood mining to the roading emergency works fund and the emergency event

fund.

· Agreed to reduce the rates contribution towards the

roading emergency works fund from $165k to $100k for 2025/26.

· Agreed to fund the Blossom Festival $24,500 from the

District Tourism reserve fund for 2025/26 and 2026/27.

As a result of the Ida

MacDonald Roxburgh Pool Punawai Ora vesting the Roxburgh Pool to the Council,

the admission charges for the pool have been added to the fees and charges. The

admission charges are consistent to those charged under the previous management.

The total average rates

increase for year one of the LTP is 12.47% (adjusted for growth of 2.1%). This

is a reduction of 0.54% from the average rates increase of 13.01% that was

consulted on. This was impacted from the decisions made during deliberations.

The individual rates’ increases will vary depending on the services

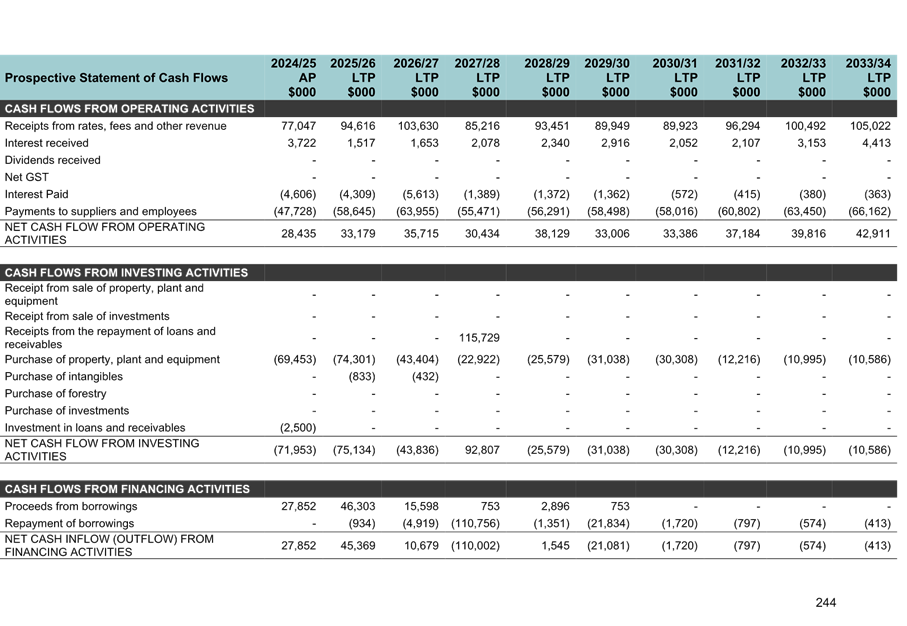

received and how the property valued. The LTP prospective financial forecasts

show a balanced budget for the LTP. To achieve this council will rely on land

sales across the 9 years of the plan. If these sales are not achieved the

council will not achieve a balanced budget in the 9 years of the plan.

The LTP considers the

transfer of Three waters assets to a council-controlled organisation (CCO) and

the financials show this impact. Rates will increase on average over the next

two years by 9.99% (adjusted for growth of 2.1%). This will decrease

significantly in year 3 of the LTP by (29.48%) when Central Otago District

Council is proposing to transfer three waters to the CCO and will no longer be

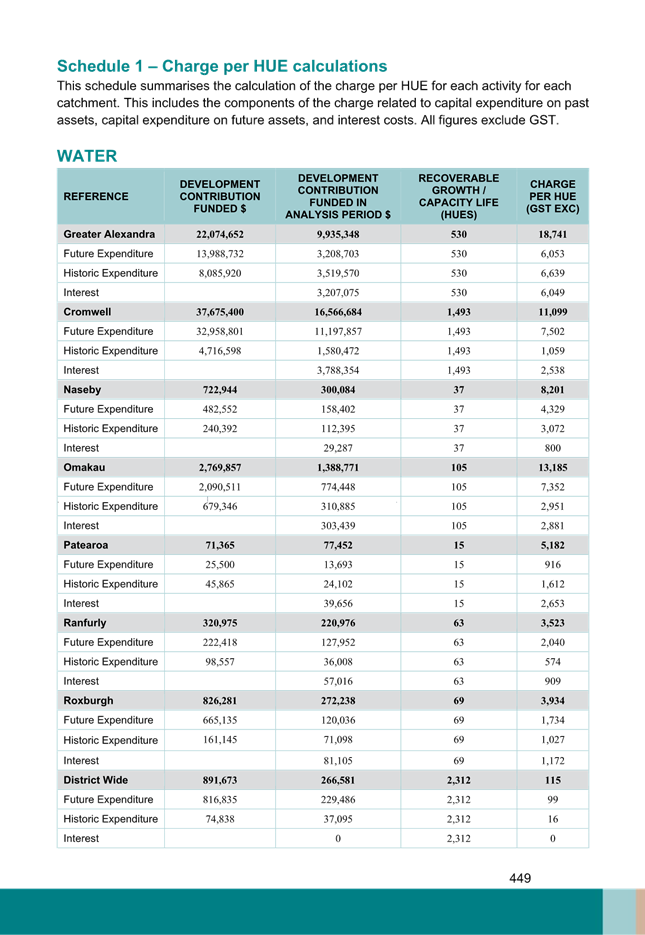

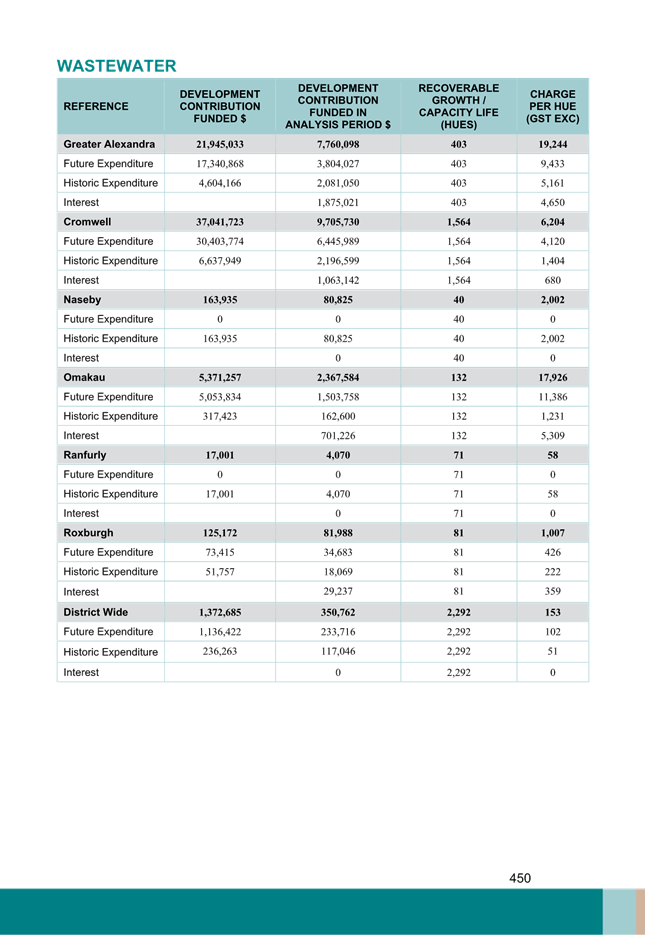

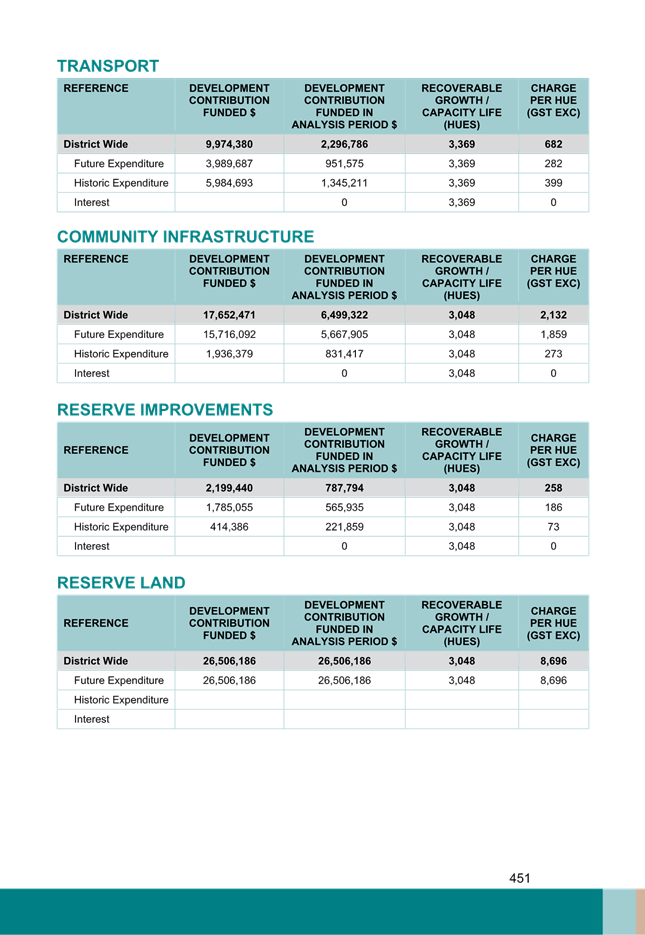

collecting rates for Three waters activities.

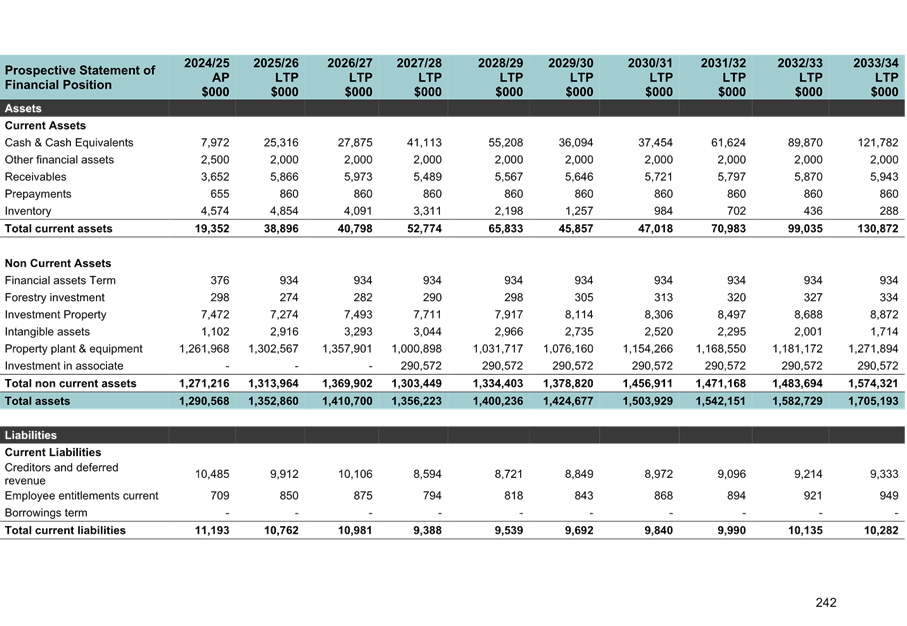

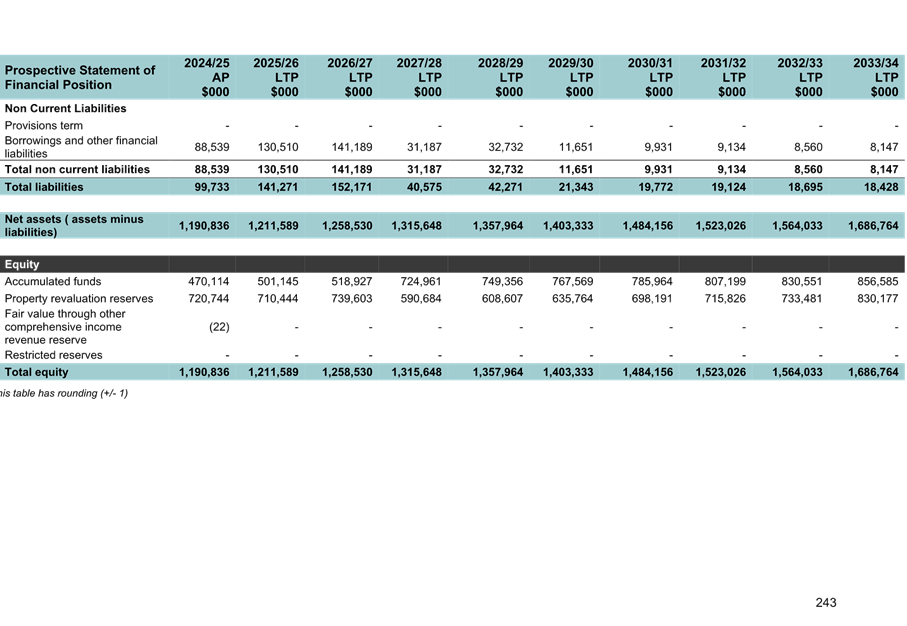

External debt is expected to

peak in year 2 at $141M, increasing from the Annual Plan 2024/25 planned debt

level of $88M. This will decrease to $31M in year 3 and further dropping to $8M

by year 9. It is expected that the three waters debt will transfer to the CCO

in year 3.

There are risks associated with

the proposal to create a regional CCO to deliver water services. Councils who

have indicated their preference to create a regional entity, may not join with

us. This will mean the Council will proceed to set up a single council CCO. Council

has undertaken a more extensive consultation around water reform to comply with

the current legislation and the preferred option is to create a regional CCO.

However, the outcome of this consultation will not be known until after 10 July

when council will hear submissions and decide which option it wishes to take.

Council will also be required to submit a water delivery plan to the Department

of Internal Affairs for approval. It is anticipated that approval will occur

after 3 September 2025.

The Council has employed a transition

manager to oversee the transition of the delivery of the three Water services

from Council ownership to CCO. There are many unknowns including the management

structure and fees, the Board and the Chief Executive, along with the

Council’s operating structure going forward. The shared investment in the

new CCO is calculated on the net asset assumption, which includes the fair

value of the assets less liabilities (borrowing). The percentage of the Council

ownership will be dependent on the final number of councils that join the CCO.

There is a key assumption that the level of ownership of the regional CCO will

be consistent with relative contributions of net assets by each council joining

the CCO.

4. Financial

Considerations

This decision is in-line with

the overall plans and budgets of the 2025-34 Long-term Plan. It also ensures

compliance of the Local Government Act 2002 and Local Government (Rating) Act

2002.

The financial impact of

adopting this plan and any amendments (if applicable) are significant as it

determines the operational and capital expenditure for the 2025-34 Long-term

Plan and how these are funded from rates, activity revenue, reserves and loans.

The average rates increase is 12.47% for year 1 of

this long-term plan. This

number includes the modelling for the preferred

options for each of the nine consultation items as well as an allowance of 2.1%

for growth.

5. Options

Option 1 –

(Recommended)

That Council adopts the

2025-34 Long-term Plan and sets the fees and charges for the 2025-26 financial

year.

Advantages:

· Meets

legislative requirements.

· Allows

Council to collect the relevant fees and charges.

· Continues

with the programme of work contained within the 2025-34 Long-term Plan.

Disadvantages:

· None.

Option 2

That Council does not adopt

the 2025-34 Long-term Plan, set the fees and charges for the 2025-26 financial

year.

Advantages:

· None.

Disadvantages:

· Breach

of Local Government Act 2002, Local authorities must have at

all times a Long-term Plan under Section 93 of the Local Government Act 2002.

· Does

not allow Council to assess and collect rates for 2025-26 which would result in

significant financial implications for council.

· Does

not allow Council to collect the relevant fees and charges.

6. Compliance

|

Local Government Act 2002 Purpose Provisions

|

Local authorities

must have at all times a Long-term Plan under Section 93 of the Local

Government Act 2002.

This

has been supported by a consultation process which enables democratic local

decision making and action by, and on behalf of the community.

AND

This decision promotes the

(social/cultural/economic/environmental) wellbeing of the community, in the

present and for the future by giving consideration to the communities

preference for their district included in the 2025-34 Long-term Plan.

|

|

Decision consistent with other Council plans and policies? Such as

the District Plan, Economic Development Strategy etc.

|

Yes

|

|

Considerations as to sustainability, the environment and climate

change impacts

|

These have all been considered as part of the 2025-34 Long-term

Plan.

|

|

Risks Analysis

|

The

risk if Council does not consider the setting of the

rates in conjunction with the 2025-34 Long-term Plan is that Council will be

in breach of the legislation.

|

|

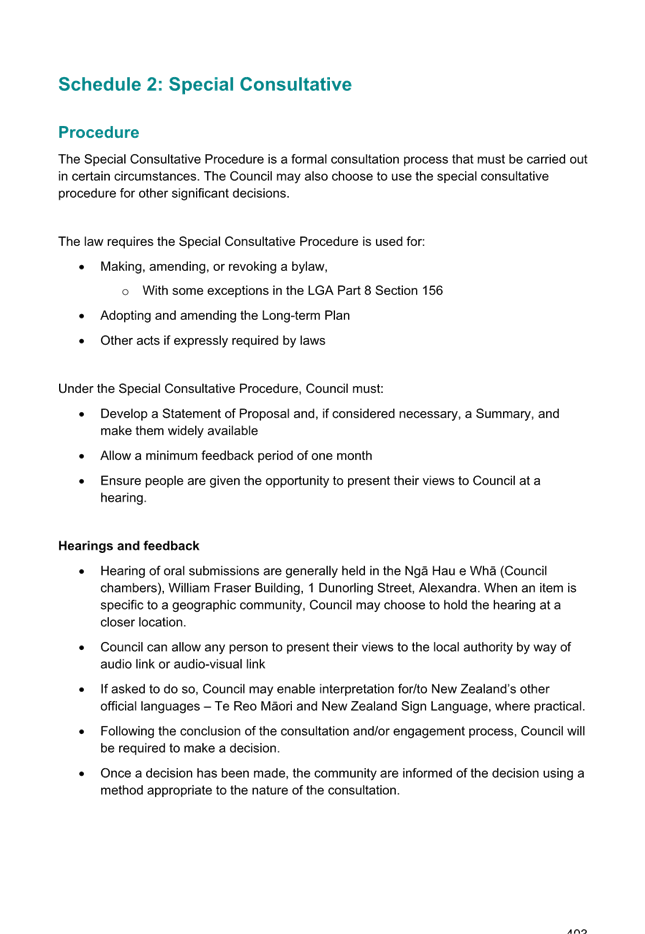

Significance, Consultation and Engagement (internal and external)

|

The decision to adopt this report is significant as

adoption will approve the 2025-34 Long-term Plan; and the confirmation of the

2025-26 fees and charges. The special consultative procedure was used in the

process in accordance with the Local Government Act 2002.

|

7. Next

Steps

The 2025-34 Long-term Plan

will come into effect on 1 July 2025 and will be used as the primary financial

and non-financial performance plan for the 2025-26 year.

Rates assessments and

invoices will be provided to ratepayers from July 2025 onwards, as required in

the Local Government (Rating) Act 2002.

The Rating Policy will be

made available on the Council website, along with Council’s resolution

from this report.

Once the 2025-34 Long-term

Plan has been adopted it will be published on our website and a notice placed

in Council’s Noticeboard in The News.

8. Attachments

Appendix 1 - 2025-34 Long-term

Plan ⇩

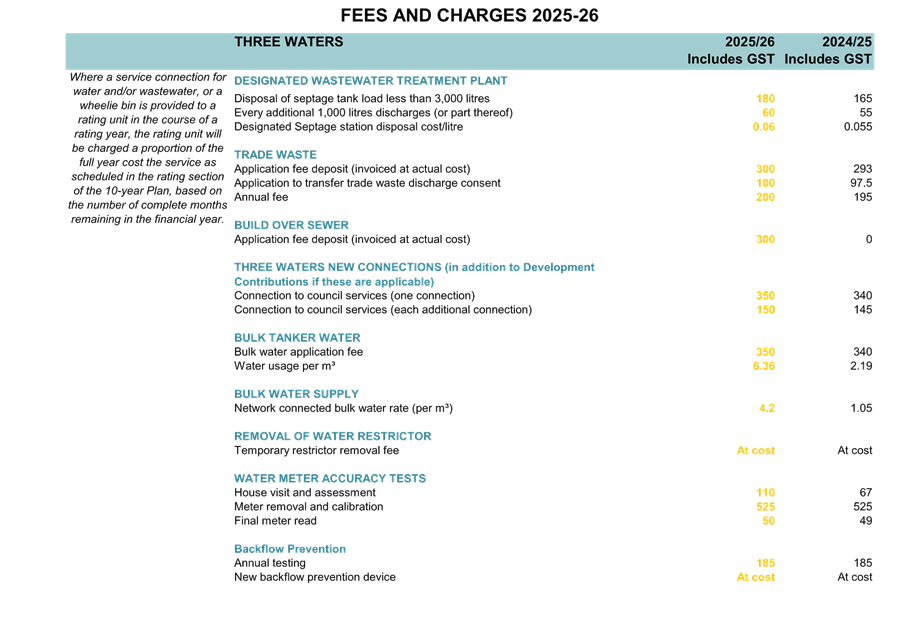

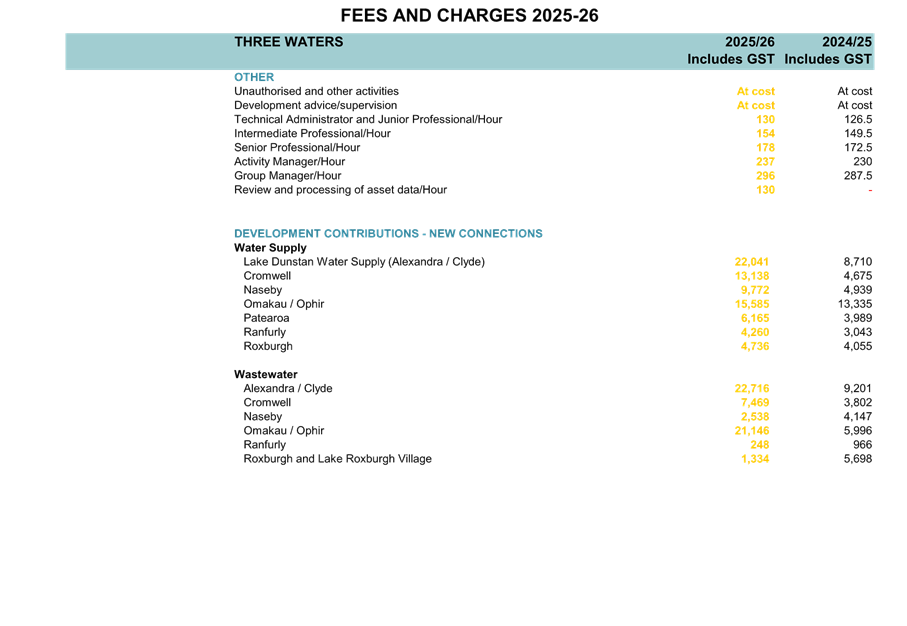

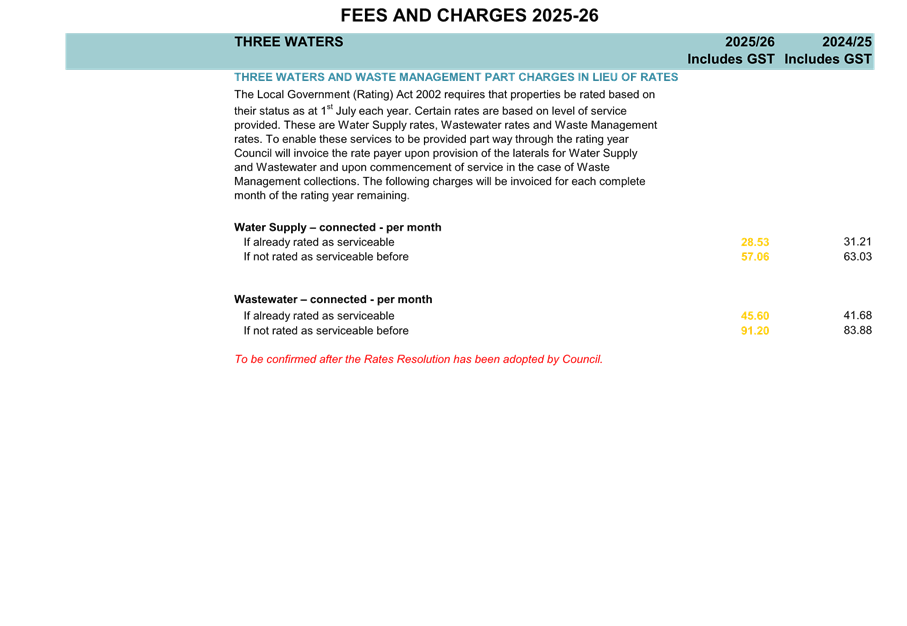

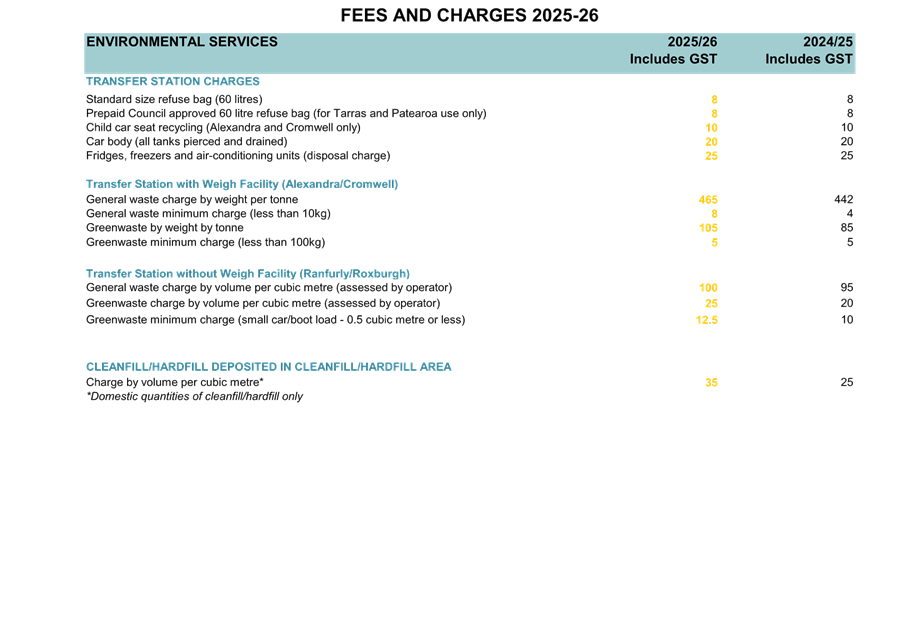

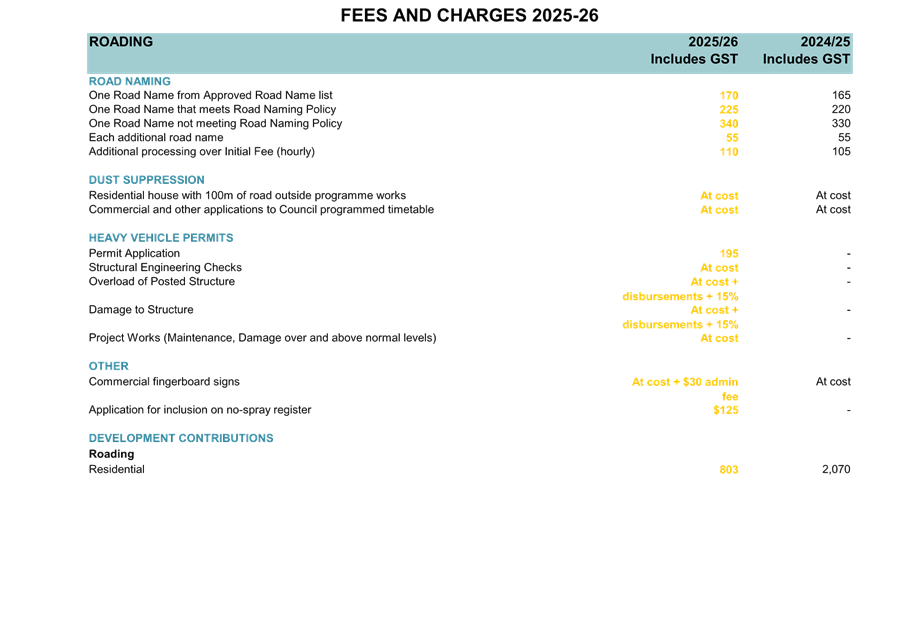

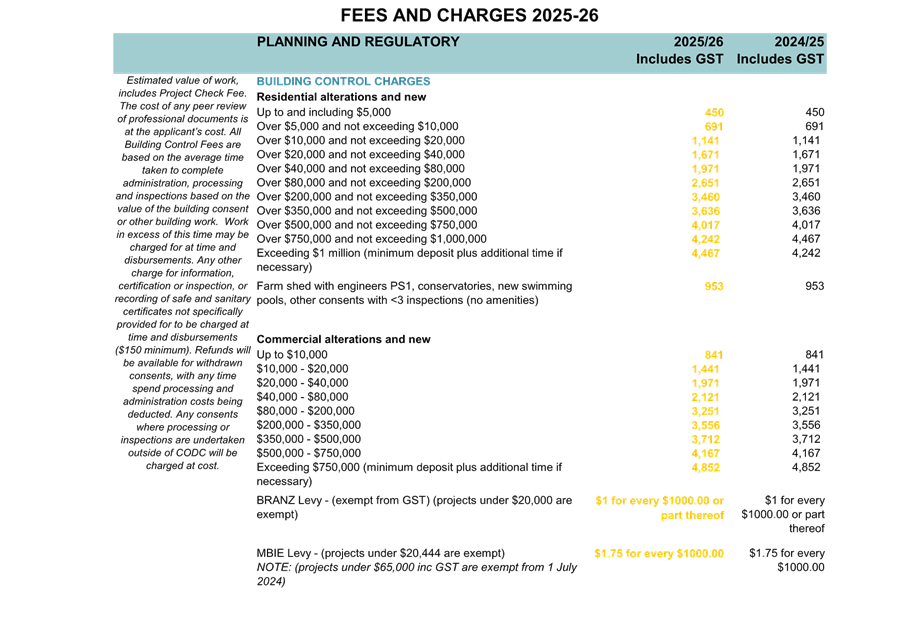

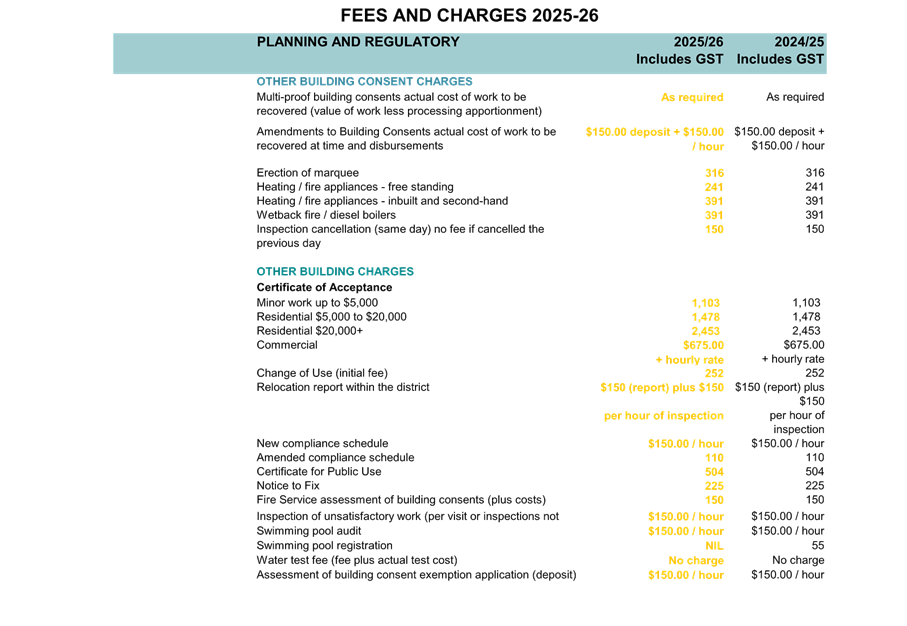

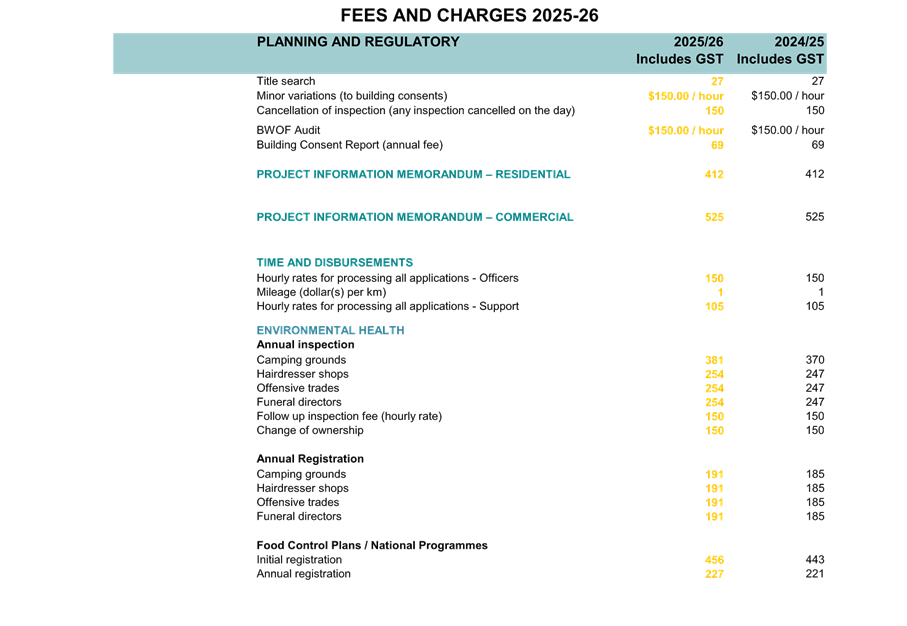

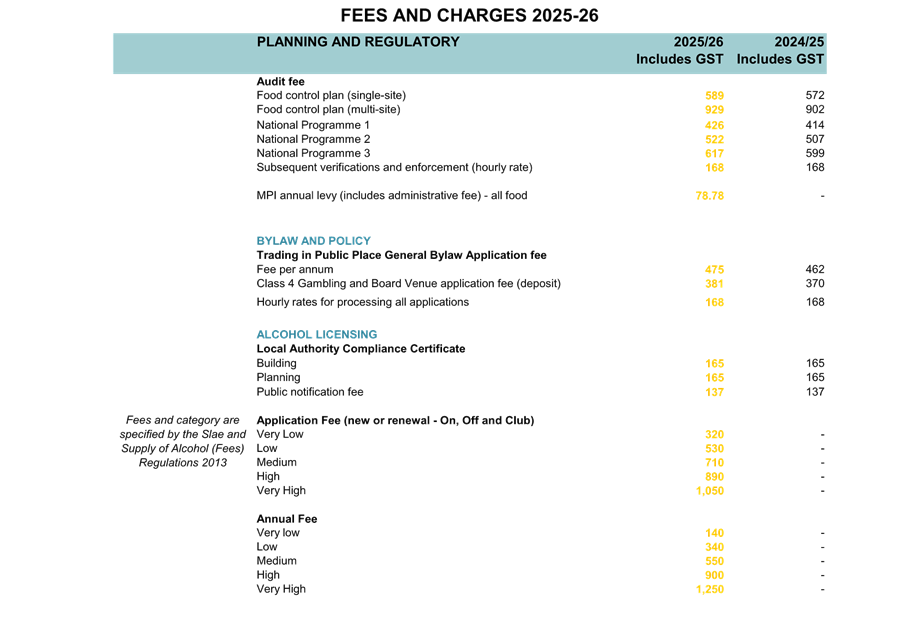

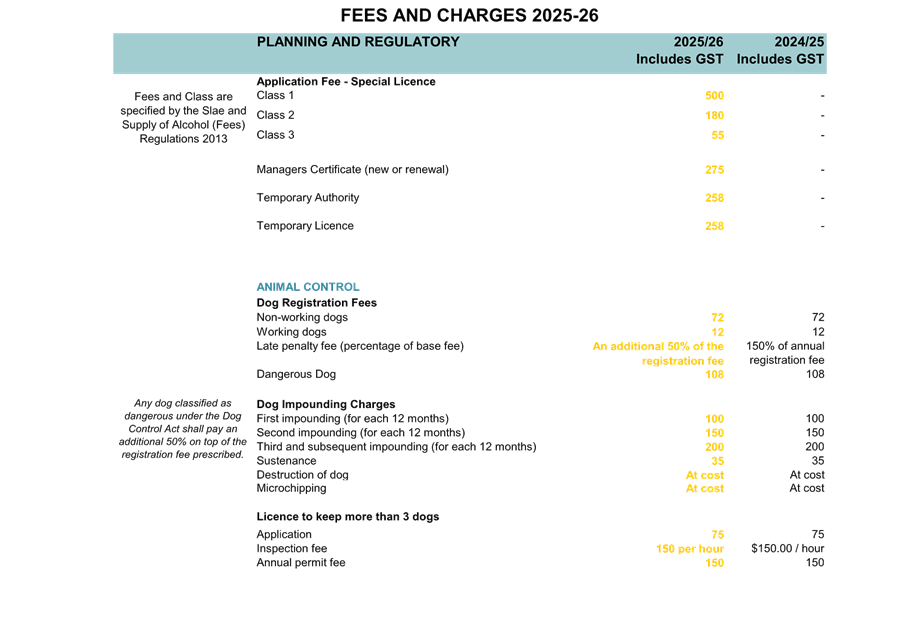

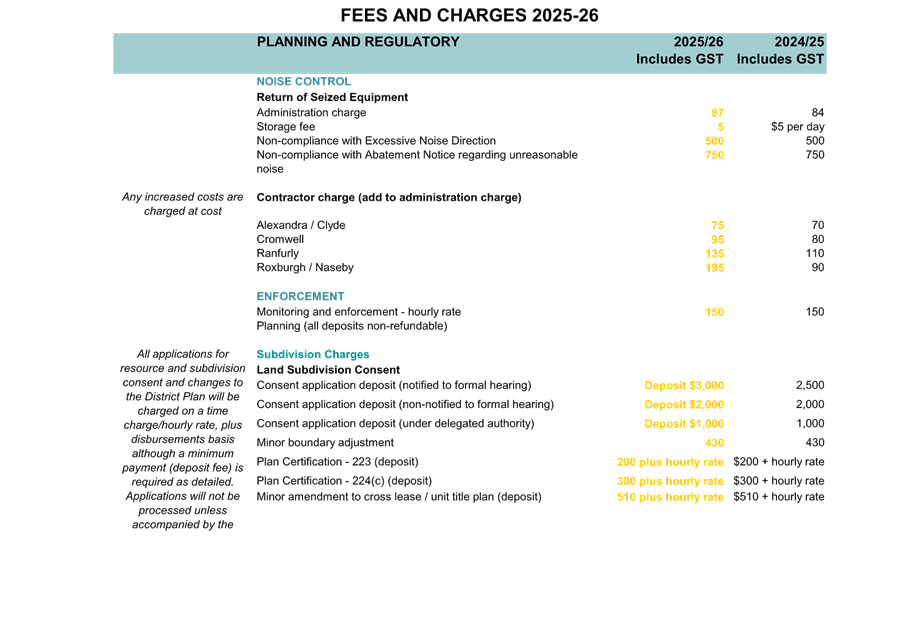

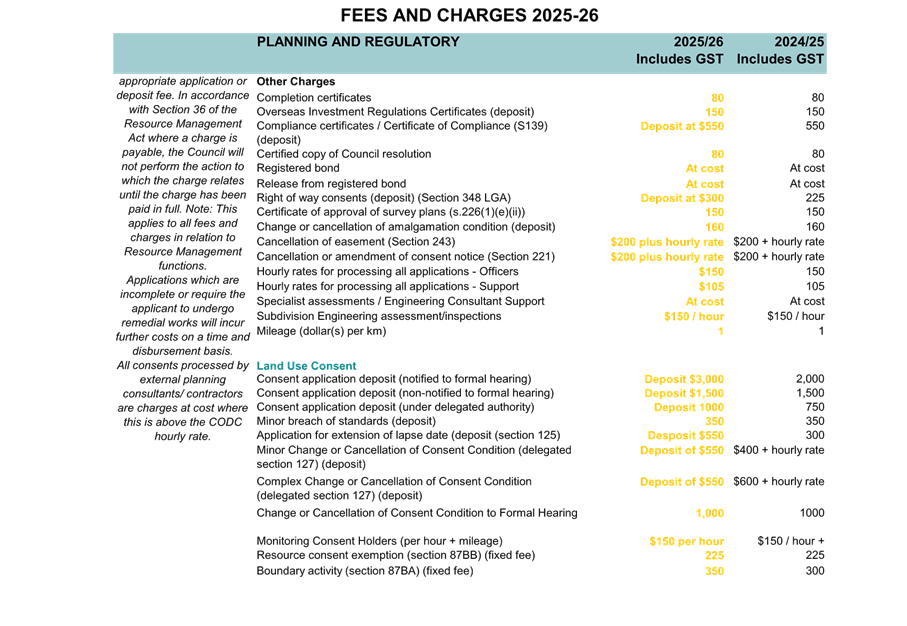

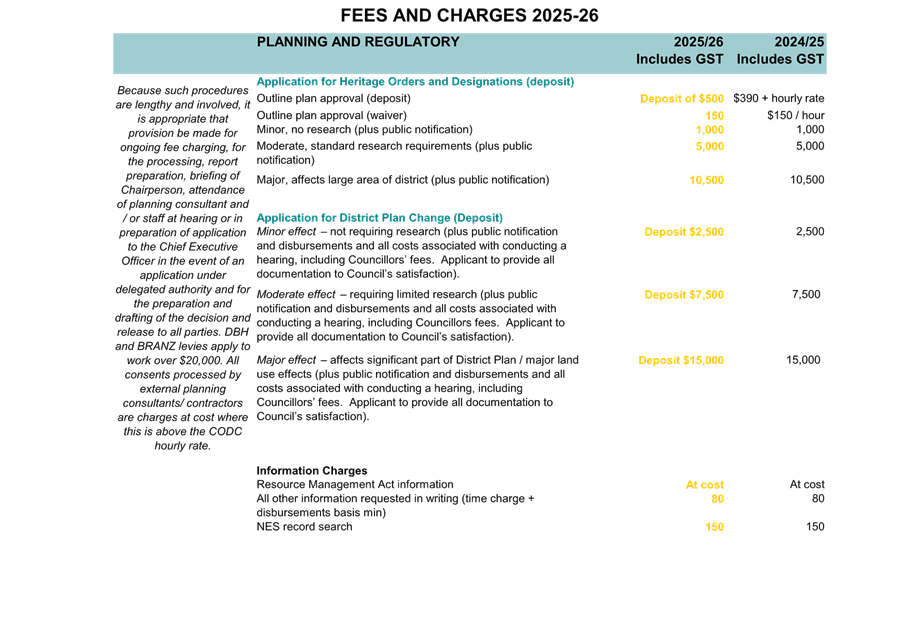

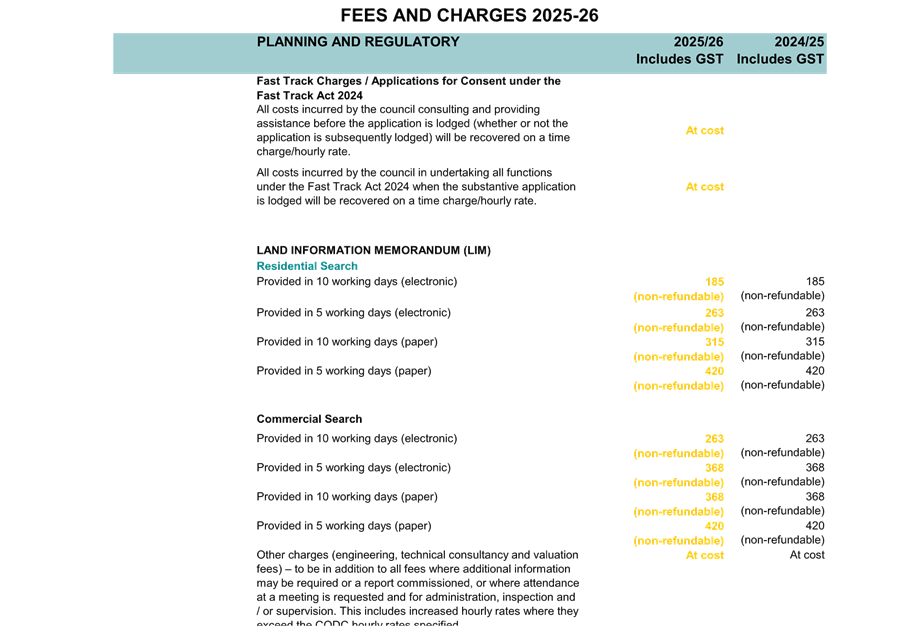

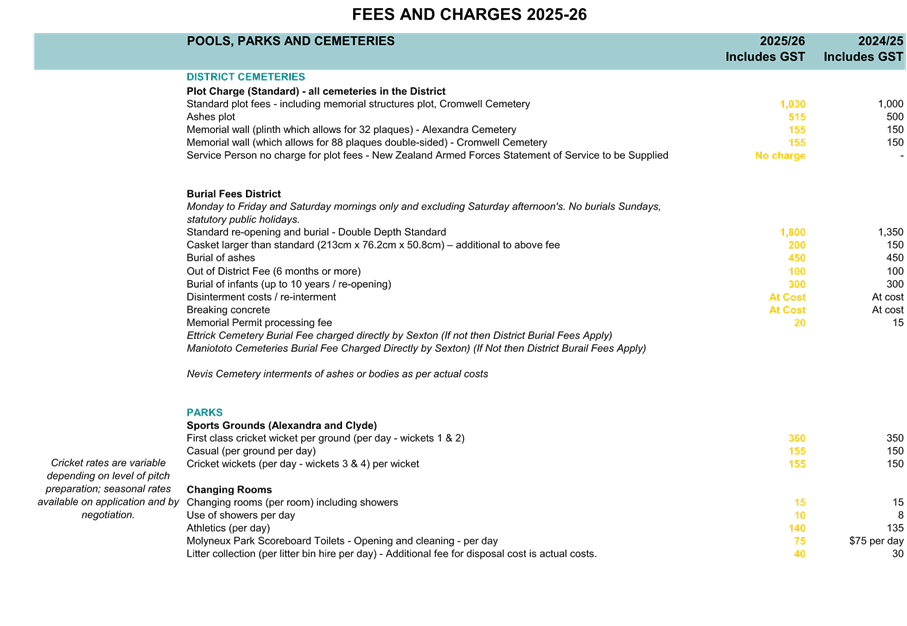

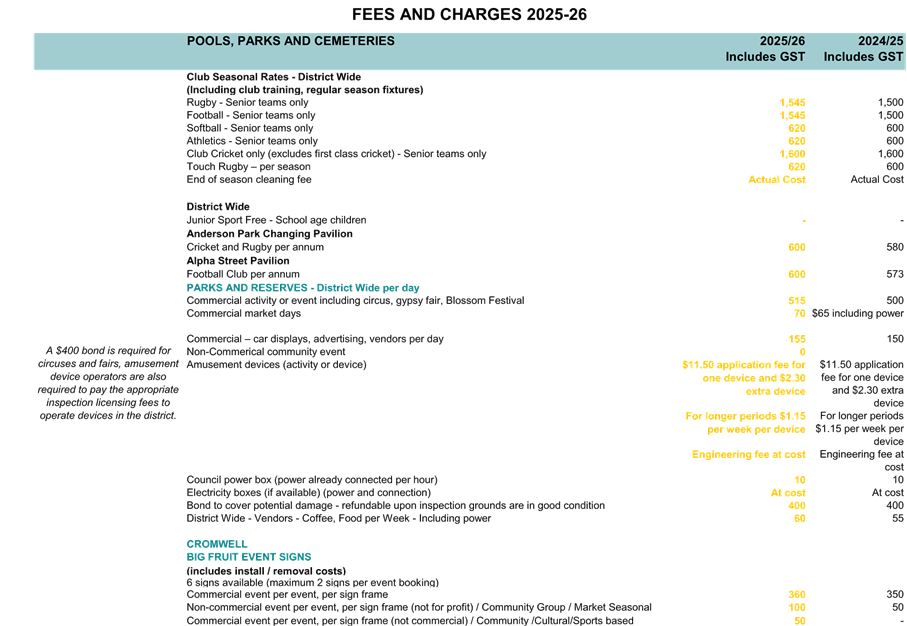

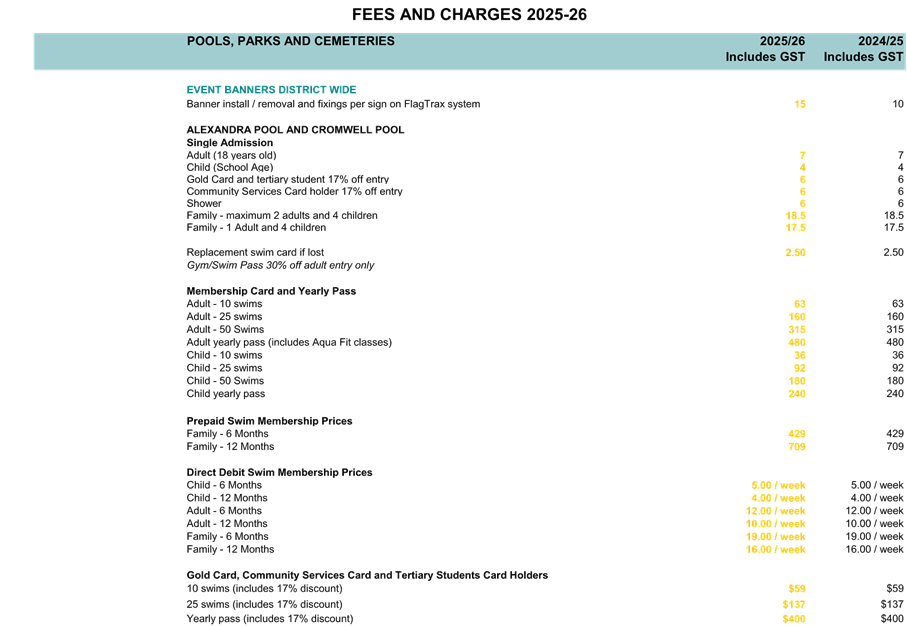

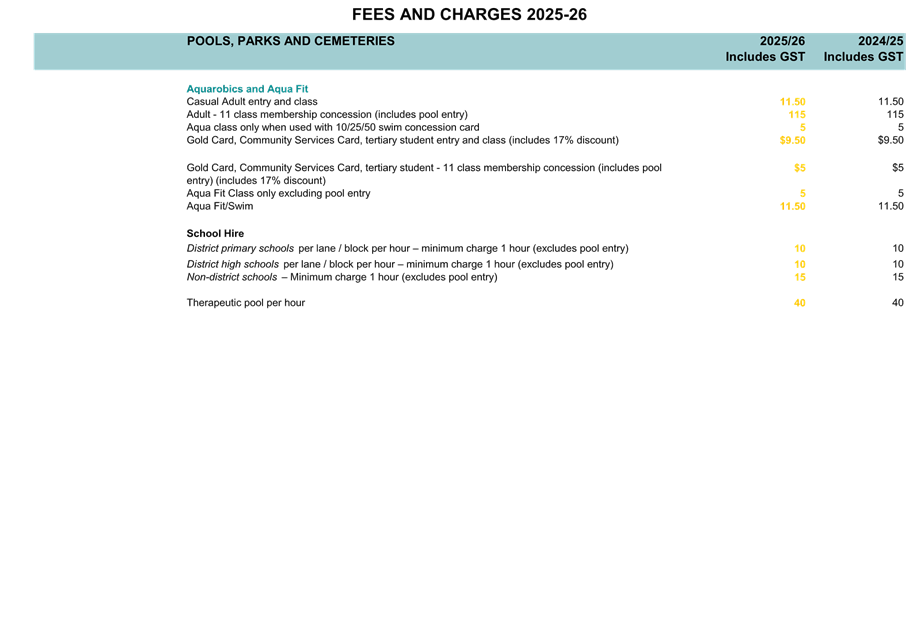

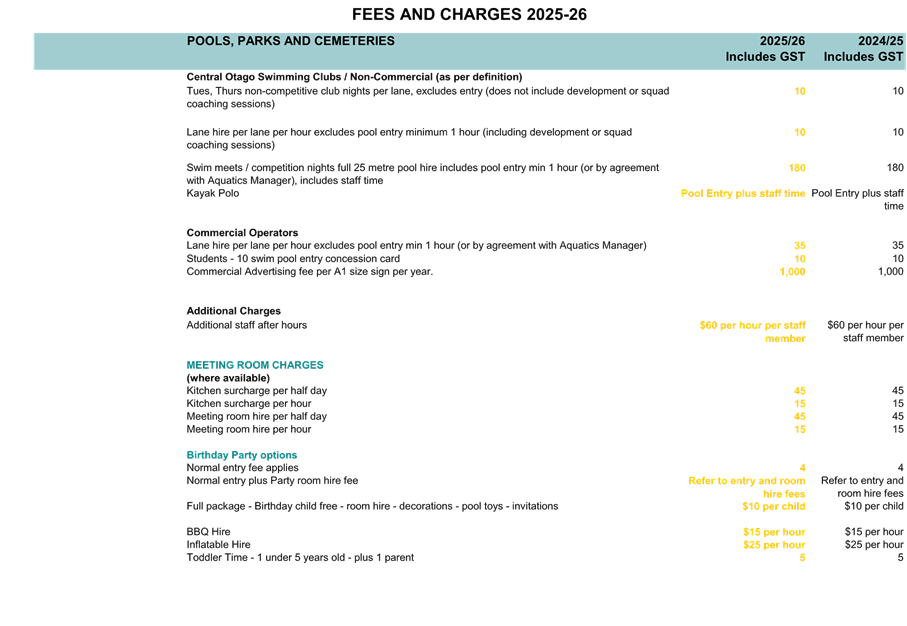

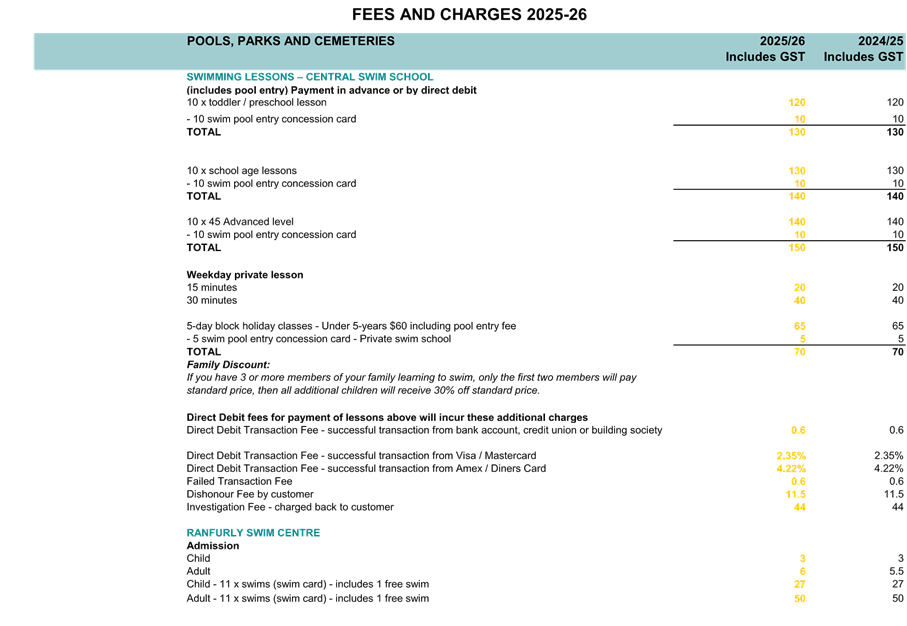

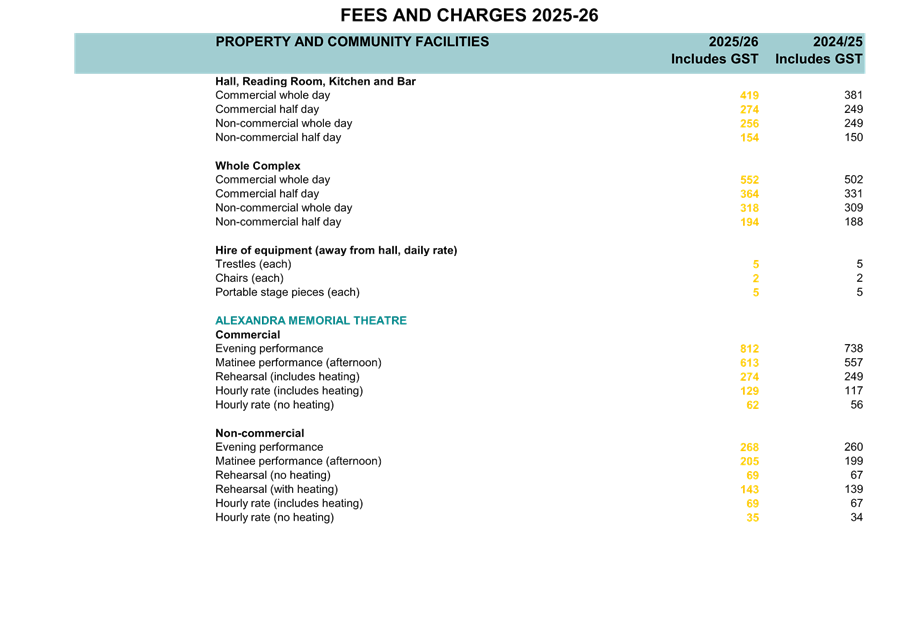

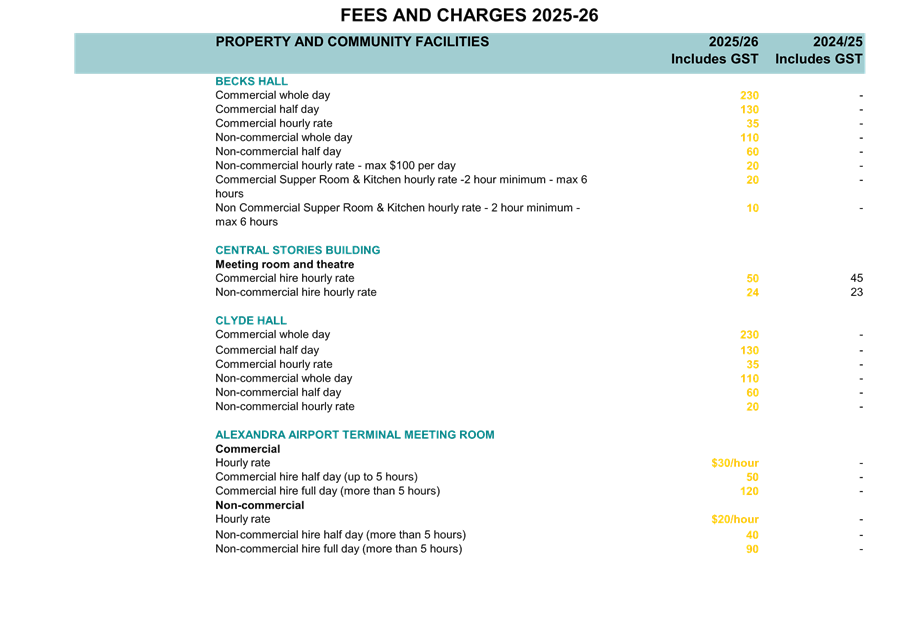

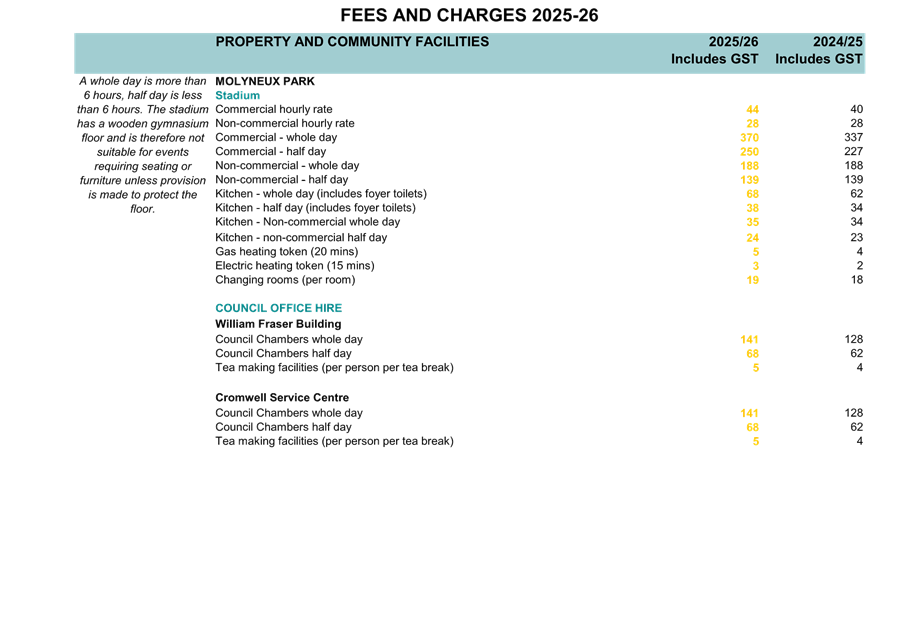

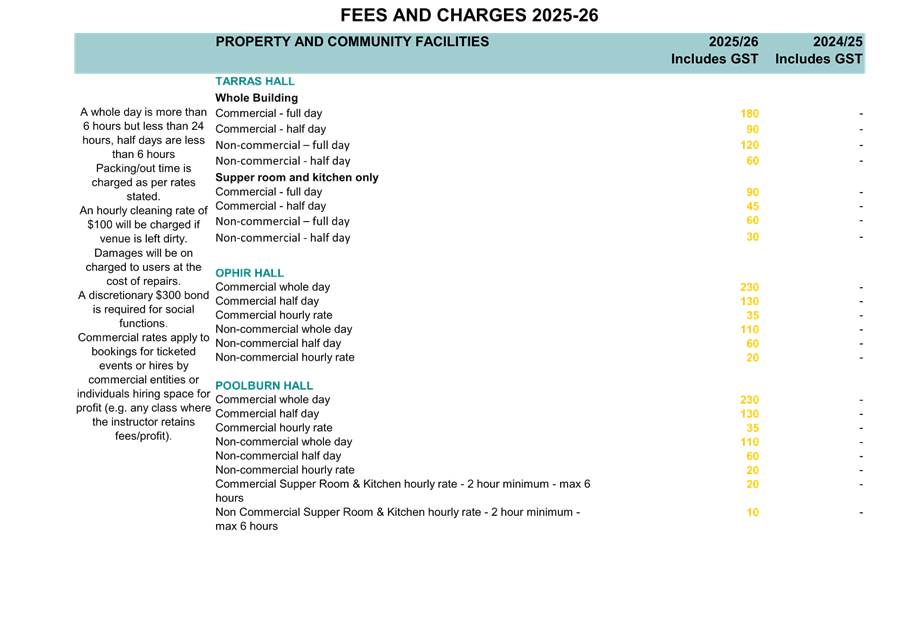

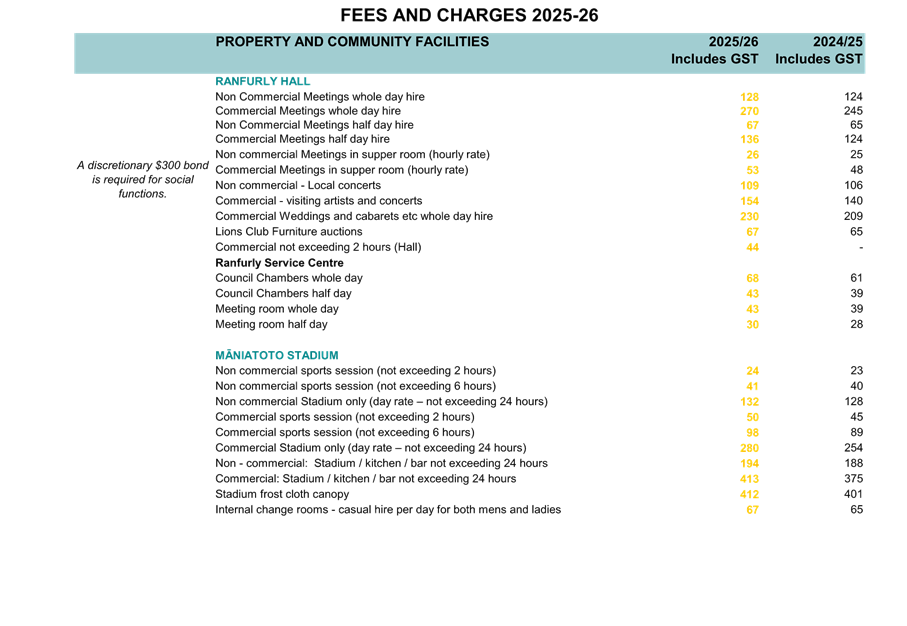

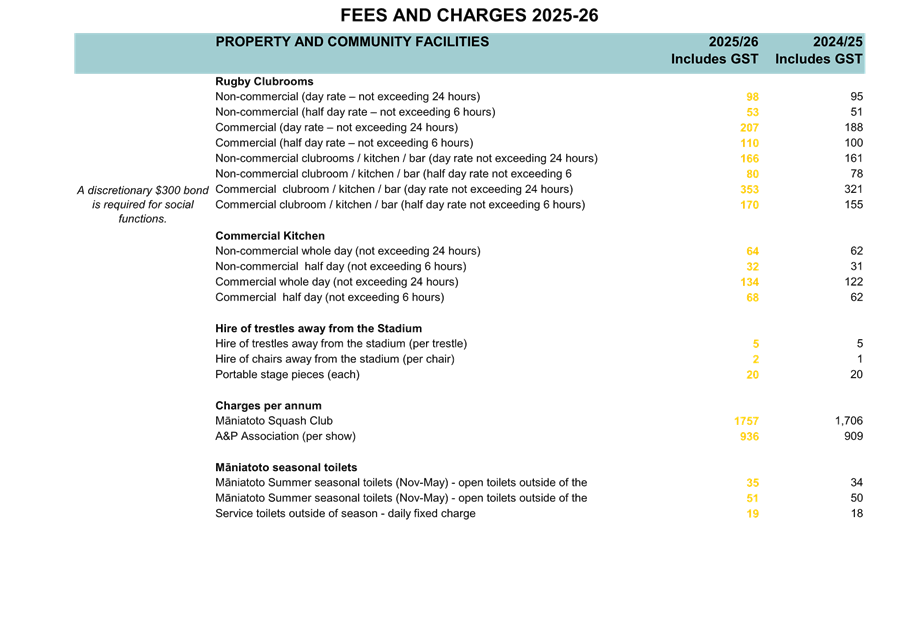

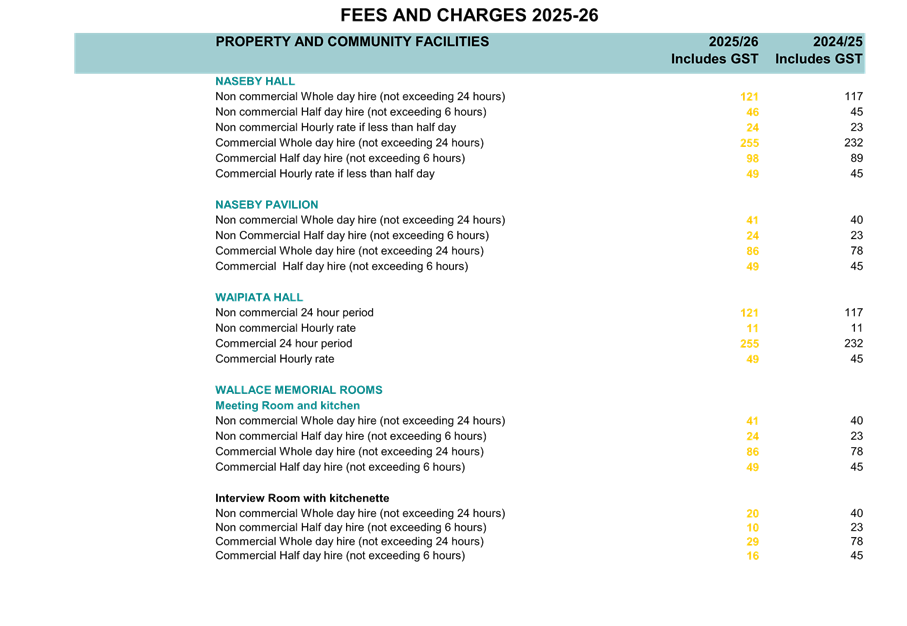

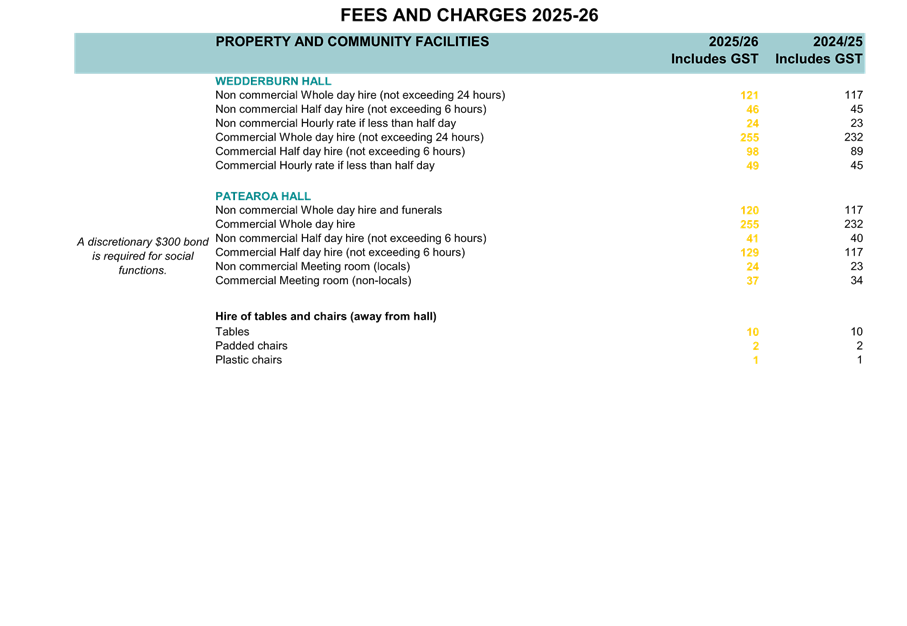

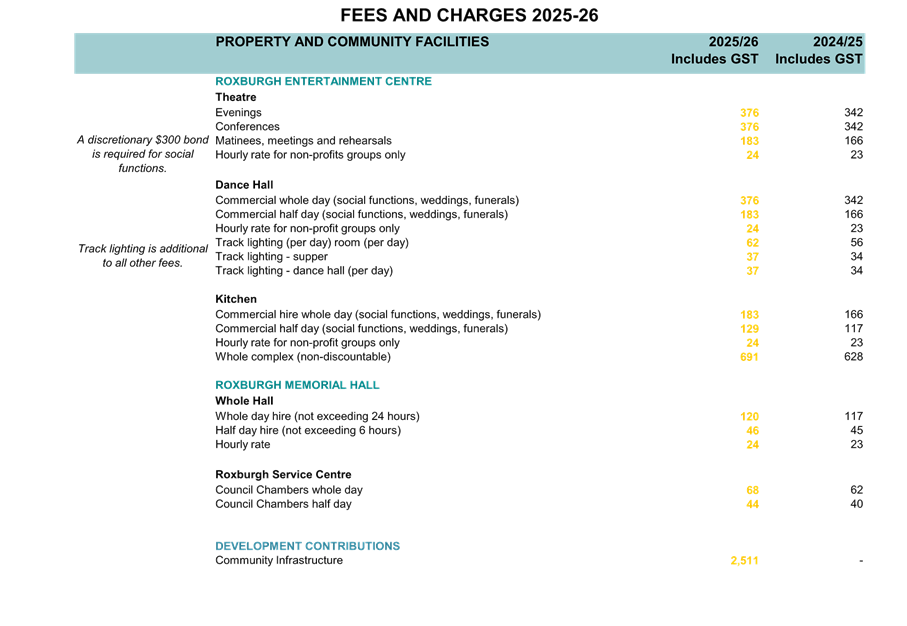

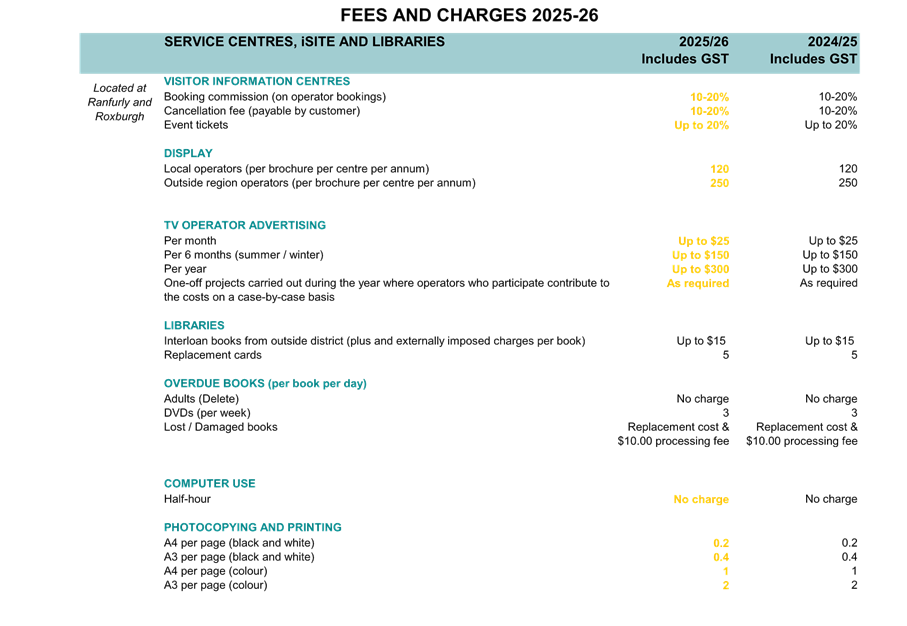

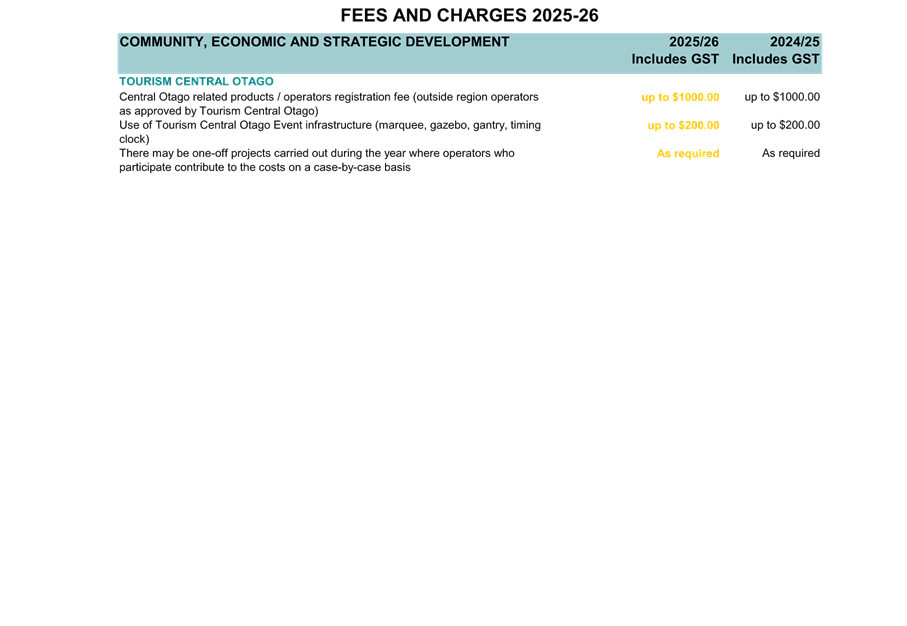

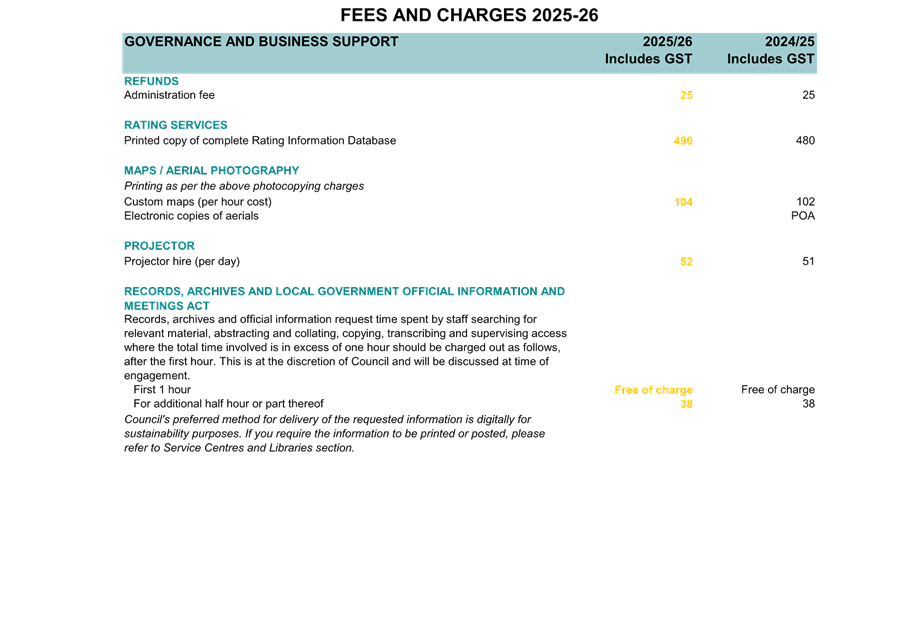

Appendix 2 - Fees and Charges

Schedule 2025-26 ⇩

|

30 June 2025

|

|

25.13.3 Setting of Rates

for the 2025/26 Financial Year

Doc ID: 2497874

|

Report Author:

|

Donna McKewen, Acting Chief

Financial Officer

|

|

Reviewed

and authorised by:

|

Saskia Righarts, Group Manager –

Governance and Business Services

|

1. Purpose

of Report

To resolve the setting of

the rates, due dates and penalties for rates for the 2025-26 financial year.

|

Recommendations

That the Council

A. Receives

the report and accepts the level of significance.

B. That

the Central Otago District Council resolves to set the following rates under

the Local Government (Rating) Act 2002, on rating units in the Central Otago

District for the financial year commencing 1 July 2025 and ending on 30 June

2026.

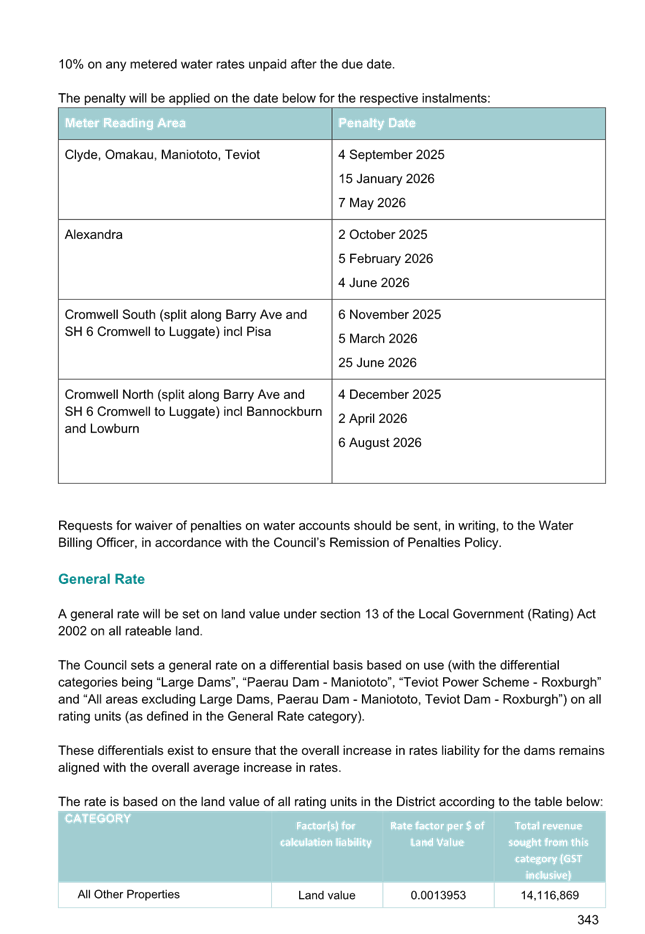

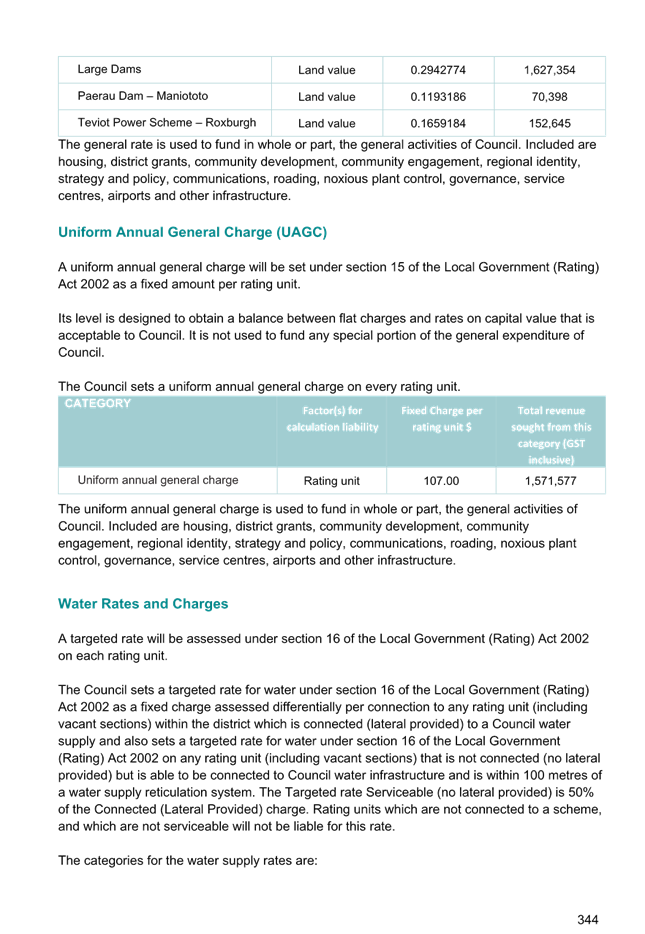

General

Rates

A General rate set on

land value of the land under section 13 of the Local Government (Rating) Act

2002 on all rateable land. The Council

sets a differential general rate on the land value of all rateable rating

units in the district as set out in the table below:

|

CATEGORY

|

Factor(s) for

calculation of liability

|

Rate per $ of Land Value

(GST inclusive)

|

Total revenue sought

from this category (GST inclusive)

|

|

All Other Properties

|

Land value

|

$0.0013953

|

$14,116,869

|

|

Large Dams

|

Land value

|

$0.2942774

|

$1,627,354

|

|

Paerau Dam – Maniototo

|

Land value

|

$0.1193186

|

$70,398

|

|

Teviot Power Scheme – Roxburgh

|

Land value

|

$0.1659184

|

$152,645

|

Uniform Annual General Charge

A Uniform Annual

General Charge set under section 15 of the Local Government (Rating) Act 2002

of $107.00 per rating unit.

|

CATEGORY

|

Factor(s) for calculation of liability

|

Fixed Charge per rating

unit (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

Uniform Annual General

Charge

|

Rating unit

|

$107.00

|

$1,571,577

|

Water Rates

The Council sets a

differential targeted rate set under section 16 of the Local Government

(Rating) Act 2002 on all rating units connected to or serviceable by a

Council water supply (as defined in the Rating Policy - Funding Impact

Statement (FIS)) as follows:

|

CATEGORY

|

Factor(s) for calculation liability

|

Fixed charge $ (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

Connected

(Lateral Provided)

|

Per connection

|

$684.66

|

$7,845,544

|

|

Serviceable

(No Lateral Provided)

|

Rating unit

|

$342.33

|

$29,928

|

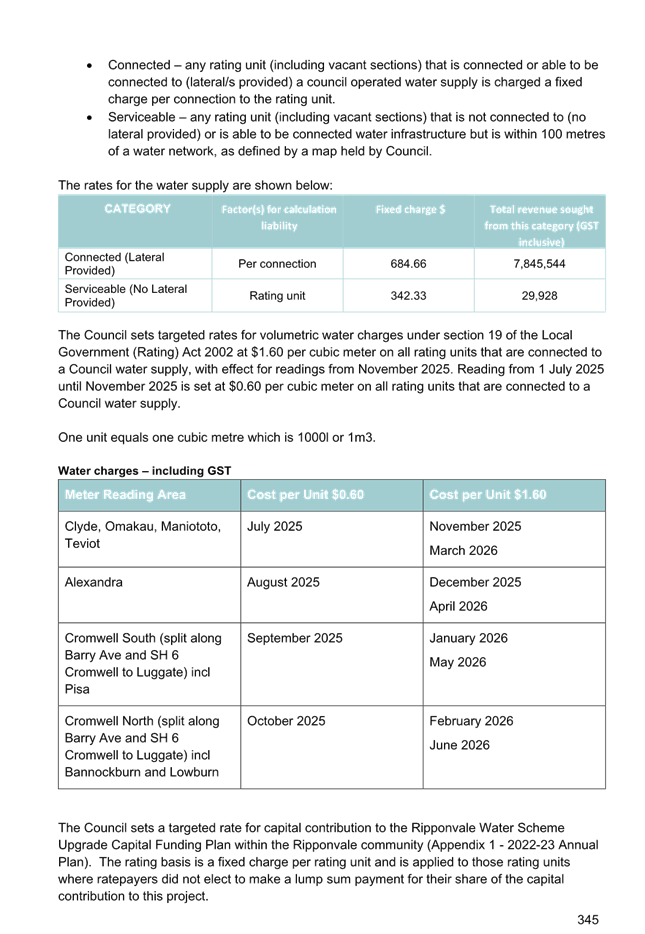

Volumetric Water Charges

The Council sets

targeted rates for volumetric water charges under section 19 of the Local

Government (Rating) Act 2002 at $1.60 per cubic meter on all rating units

that are connected to a Council water supply, with effect for readings from

November 2025. Reading from 1 July 2025 until November 2025 is set at $0.60

per cubic meter on all rating units that are connected to a Council water

supply. As defined in the FIS, as follows:

One unit

equals one cubic meter which is 1000l or 1m3.

Water charges – including GST

|

Meter Reading Area

|

Cost per Unit $0.60

|

Cost per Unit $1.60

|

|

Clyde, Omakau,

Maniototo, Teviot

|

July 2025

|

November 2025

March 2026

|

|

Alexandra

|

August 2025

|

December 2025

April 2026

|

|

Cromwell South (split

along Barry Ave and SH 6 Cromwell to Luggate) including Pisa

|

September 2025

|

January 2026

May 2026

|

|

Cromwell North (split

along Barry Ave and SH 6 Cromwell to Luggate) including Bannockburn and

Lowburn

|

October 2025

|

February 2026

June 2026

|

Ripponvale Water Management Rate

The Council sets a

targeted rate for capital contribution to the Ripponvale Water Scheme Upgrade

Capital Funding Plan within the Ripponvale community. The rating basis

is a fixed charge per rating unit and is applied to those rating units where

ratepayers did not elect to make a lump sum payment for their share of the

capital contribution to this project.

The Rates

Information Database identifies properties that have a targeted rate for

capital contribution, and those that made a lump sum payment and to which the

targeted rate for capital contribution does not apply.

Sections 117A-M of the Local Government

(Rating) Act 2002 relate to Lump sum payment contributions.

The targeted

rate is based as a fixed charge for each rating unit for a finite ten-year

period as follows:

|

CATEGORY

|

Factor(s) for calculation liability

|

Fixed charge $ (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

Ripponvale Water Management

(targeted rate payment per year)

|

Rating

unit

|

$602.57

|

$37,962

|

Wastewater Rates

The Council sets a

differential targeted rate set under section 16 of the Local Government

(Rating) Act 2002 on all rating units connected to or serviceable by a

Council wastewater supply (as defined in the Rating Policy - Funding Impact

Statement (FIS)) as follows:

|

CATEGORY

|

Factor(s) for calculation liability

|

Fixed Charge $ (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

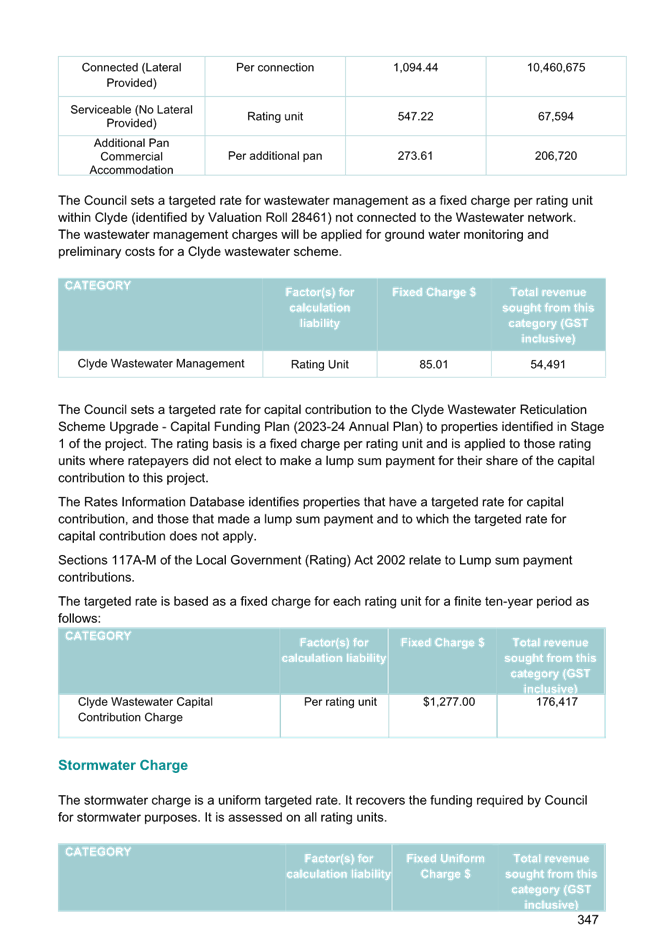

Connected (Lateral

Provided)

|

Per connection

|

$1,094.44

|

$10,460,675

|

|

Serviceable

(No Lateral Provided)

|

Rating unit

|

$547.22

|

$67,594

|

Additional Pan Commercial Accommodation Rate.

The Council sets a

targeted rate under section 16 of the Local Government (Rating) Act 2002 as a

fixed charge for each additional pan or urinal after the first, on connected

rating units providing commercial accommodation or commercial elderly rest

homes as defined by the rating valuations rules 2008. This is calculated at

25% of the Connected (Lateral Provided).

The rates for

this service are shown below:

|

CATEGORY

|

Factor(s) for calculation liability

|

Fixed Charge $

|

Total revenue sought from this category (GST inclusive)

|

|

Additional

Pan Commercial Accommodation

|

Per additional pan

|

$273.61

|

$206,720

|

Clyde Wastewater Management Rate

The Council sets a

targeted rate under section 16 of the Local Government (Rating) Act 2002 for

wastewater management as a fixed charge per rating unit within Clyde

(identified by Valuation Roll 28461) not connected to the Wastewater

network.

|

CATEGORY

|

Factor(s) for calculation liability

|

Fixed Charge $ (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

Clyde Wastewater Management

|

Rating

Unit

|

$85.01

|

$54,491

|

Clyde Wastewater Capital Contribution Charge Rate

The Council sets a

targeted rate under section 16 of the Local Government (Rating) Act 2002 for

capital contributions to the Clyde Wastewater Reticulation Scheme Upgrade -

Capital Funding Plan to properties identified in Stage 1 of the project. The

rating basis is a fixed charge per rating unit and is applied to those rating

units where ratepayers did not elect to make a lump sum payment for their

share of the capital contribution to this project.

The Rates Information Database

identifies properties that have a targeted rate for capital contribution, and

those that made a lump sum payment and to which the targeted rate for capital

contribution does not apply.

Sections 117A-M of the Local

Government (Rating) Act 2002 relate to Lump sum payment contributions.

The targeted rate is based as

a fixed charge for each rating unit for a finite ten-year period as follows:

|

CATEGORY

|

Factor(s) for calculation liability

|

Fixed Charge $ (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

Clyde Wastewater Capital

Contribution Charge

|

Per

rating unit

|

$1,277.00

|

$176,417

|

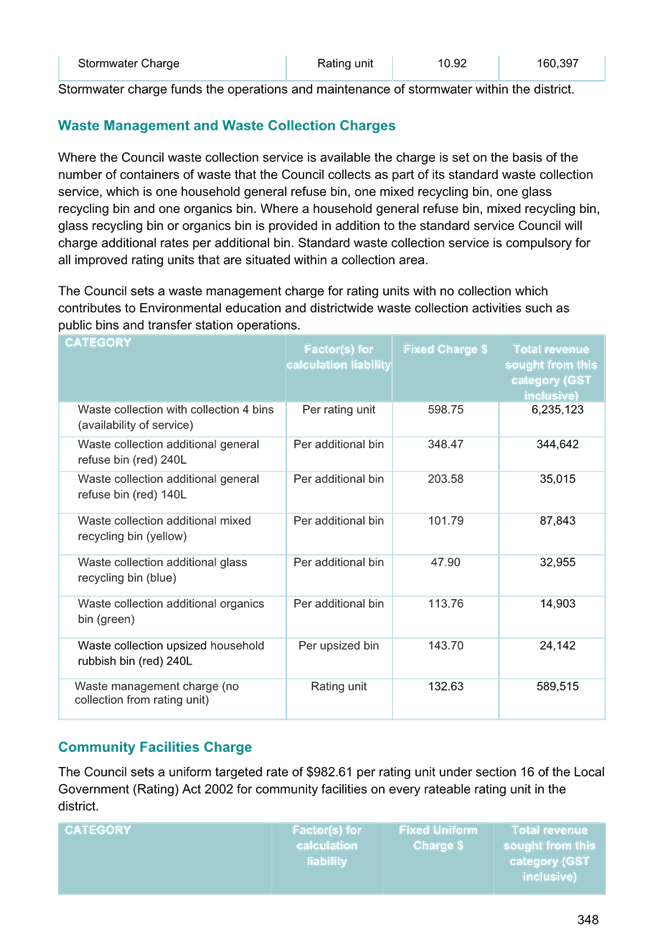

Stormwater charge

The stormwater charge

is a uniform targeted rate targeted rate under section 15 of the Local

Government (Rating) Act 2002. It recovers the funding required by Council for

stormwater purposes. It is assessed on all rating units.

|

CATEGORY

|

Factor(s) for calculation liability

|

Fixed Uniform Charge $ (GST Inclusive)

|

Total revenue sought from this

category (GST inclusive)

|

|

Stormwater Charge

|

Rating

unit

|

$10.92

|

$160,397

|

Waste Collection Charge

The Council sets

targeted rates under section 16 of the Local Government (Rating) Act 2002 for

waste collection for rating units (as per the FIS).

|

CATEGORY

|

Factor(s) for calculation liability

|

Fixed Charge $ (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

Waste collection with collection 4 bins (availability

of service)

|

Per rating unit

|

$598.75

|

$6,235,123

|

Waste Management Charge

The Council sets

targeted rates under section 16 of the Local Government (Rating) Act 2002 for

waste management for rating units with no collection (as per the FIS).

|

CATEGORY

|

Factor(s) for calculation liability

|

Fixed Charge $ (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

Waste management charge (no collection

from rating unit)

|

Rating unit

|

$132.63

|

$589,515

|

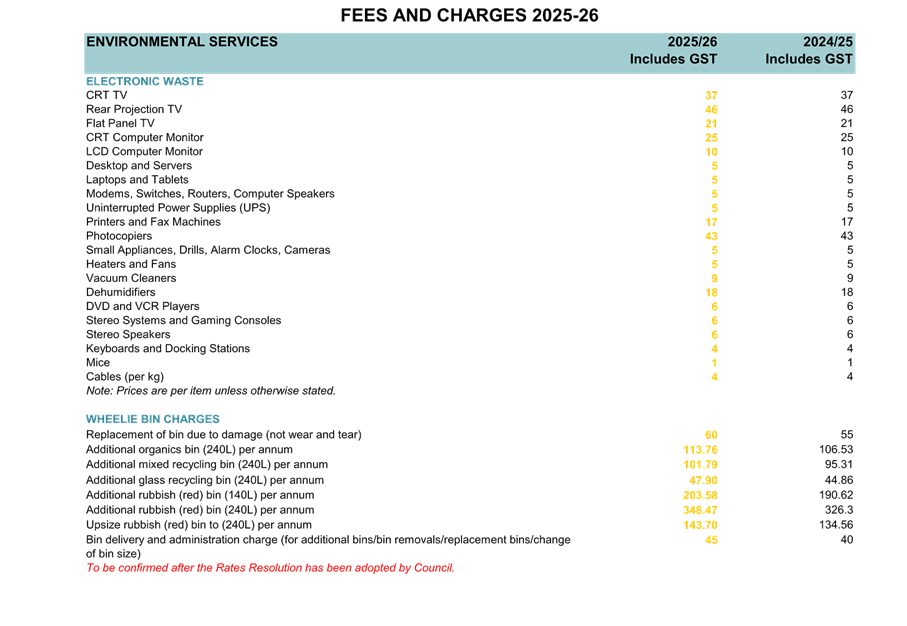

Waste Collection Additional Bins Charge

The Council sets

targeted rates under section 16 of the Local Government (Rating) Act 2002 on

rating units provided with any additional service, on a per additional

container basis as follows:

|

CATEGORY

|

Factor(s) for calculation liability

|

Fixed Charge $ (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

Waste collection additional general refuse bin (red)

240L

|

Per additional bin

|

$348.47

|

$344,642

|

|

Waste collection additional general refuse bin (red)

140L

|

Per additional bin

|

$203.58

|

$35,015

|

|

Waste collection additional mixed recycling bin

(yellow)

|

Per additional bin

|

$101.79

|

$87,843

|

|

Waste collection additional glass recycling bin

(blue)

|

Per additional bin

|

$47.90

|

$32,955

|

|

Waste collection additional organics bin (green)

|

Per additional bin

|

$113.76

|

$14,903

|

|

Waste

collection upsized household rubbish bin (red) 240L

|

Per upsized bin

|

$143.70

|

$24,142

|

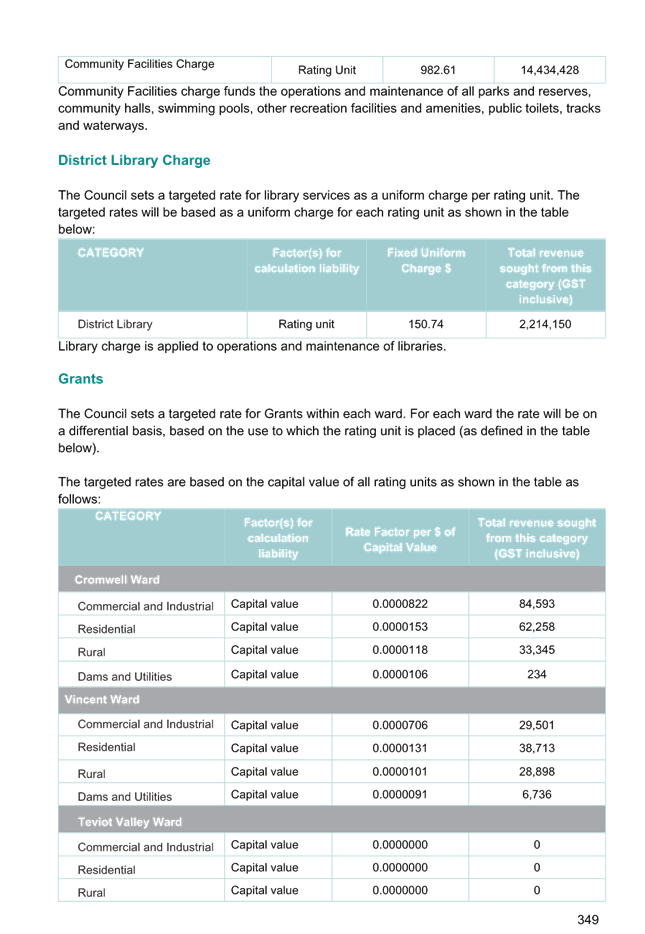

Community Facilities Charge

The Council sets a

uniform targeted rate of $982.61 per rating unit under section 16 of the Local

Government (Rating) Act 2002 for community facilities on every rateable

rating unit in the district.

|

CATEGORY

|

Factor(s) for calculation liability

|

Fixed Uniform Charge $ (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

Community Facilities Charge

|

Rating Unit

|

$982.61

|

$14,434,428

|

District Library Charge

The Council sets a

uniform targeted rate under section 16 of the Local Government (Rating) Act

2002 for library services within the District. The targeted rates will be

based as a uniform charge for each rating unit as shown in the table below:

|

CATEGORY

|

Factor(s) for calculation liability

|

Fixed Uniform Charge $ (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

District Library

Charge

|

Rating unit

|

$150.74

|

$2,214,150

|

Grants Rate

The Council sets a

targeted rate under section 16 of the Local Government (Rating) Act 2002 for

Grants within each ward, except Teviot Valley Ward.

For each ward the rate

will be on a differential basis, based on the use to which the rating unit is

placed (as defined in the table below).

The targeted rates are based on

the capital value of all rating units as shown in the table as follows:

|

CATEGORY

|

Factor(s) for calculation liability

|

Rate Factor per $ of Capital Value (GST Inclusive)

|

Total revenue sought from this category (GST

inclusive)

|

|

Cromwell Ward

|

|

Commercial and

Industrial

|

Capital value

|

$0.0000822

|

$84,593

|

|

Residential

|

Capital value

|

$0.0000153

|

$62,258

|

|

Rural

|

Capital value

|

$0.0000118

|

$33,345

|

|

Dams and Utilities

|

Capital value

|

$0.0000106

|

$234

|

|

Vincent

Ward

|

|

Commercial and

Industrial

|

Capital value

|

$0.0000706

|

$29,501

|

|

Residential

|

Capital value

|

$0.0000131

|

$38,713

|

|

Rural

|

Capital value

|

$0.0000101

|

$28,898

|

|

Dams and Utilities

|

Capital value

|

$0.0000091

|

$6,736

|

|

Teviot Valley Ward

|

|

Commercial and

Industrial

|

Capital value

|

$0.0000000

|

$0

|

|

Residential

|

Capital value

|

$0.0000000

|

$0

|

|

Rural

|

Capital value

|

$0.0000000

|

$0

|

|

Dams and Utilities

|

Capital value

|

$0.0000000

|

$0

|

|

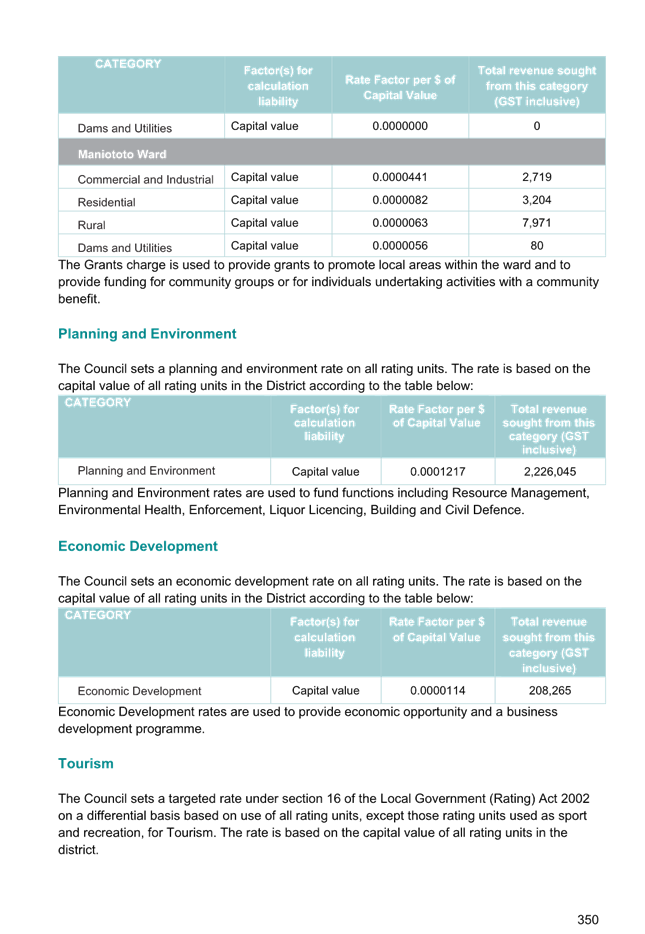

Maniototo Ward

|

|

Commercial and

Industrial

|

Capital value

|

$0.0000441

|

$2,719

|

|

Residential

|

Capital value

|

$0.0000082

|

$3,204

|

|

Rural

|

Capital value

|

$0.0000063

|

$7,971

|

|

Dams and Utilities

|

Capital value

|

$0.0000056

|

$80

|

Planning and Environment Rate

The Council sets a

targeted rate under section 16 of the Local Government (Rating) Act 2002 for

Planning and Environment on all rating units. The rate is based on the

capital value of all rating units in the District according to the table

below:

|

CATEGORY

|

Factor(s) for calculation liability

|

Rate Factor per $ of Capital Value (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

Planning and

Environment

|

Capital value

|

$0.0001217

|

$2,226,045

|

Economic Development Rate

The Council sets a targeted rate under section 16 of the

Local Government (Rating) Act 2002 for economic development on all rating

units. The rate is based on the capital value of all rating units in the

District according to the table below:

|

CATEGORY

|

Factor(s) for calculation liability

|

Rate Factor per $ of Capital Value

(GST Inclusive)

|

Total revenue sought from this

category (GST inclusive)

|

|

Economic Development

|

Capital value

|

$0.0000114

|

$208,265

|

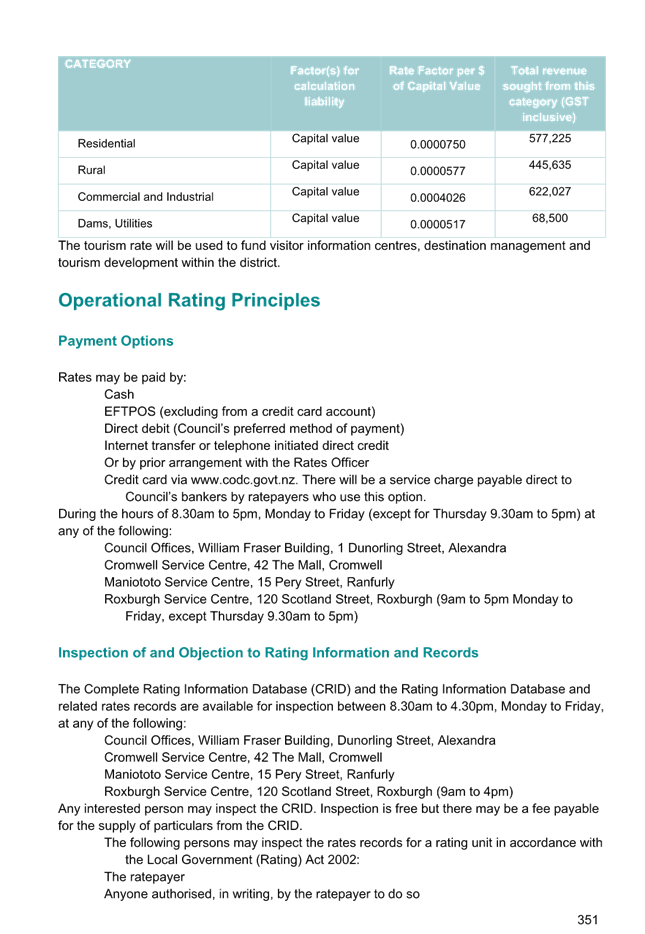

Tourism Rate

The Council sets a targeted rate under section 16 of the

Local Government (Rating) Act 2002 on a differential basis based on use of

all rating units, except those rating units used as sport and recreation, for

Tourism. The rate is based on the capital value of all rating units in the

district.

|

CATEGORY

|

Factor(s) for calculation liability

|

Rate Factor per $ of Capital Value (GST Inclusive)

|

Total revenue sought from this category (GST inclusive)

|

|

Residential

|

Capital value

|

$0.0000750

|

$577,225

|

|

Rural

|

Capital value

|

$0.0000577

|

$445,635

|

|

Commercial and Industrial

|

Capital value

|

$0.0004026

|

$622,027

|

|

Dams, Utilities

|

Capital value

|

$0.0000517

|

$68,500

|

C. To

set due dates and penalties for the financial year.

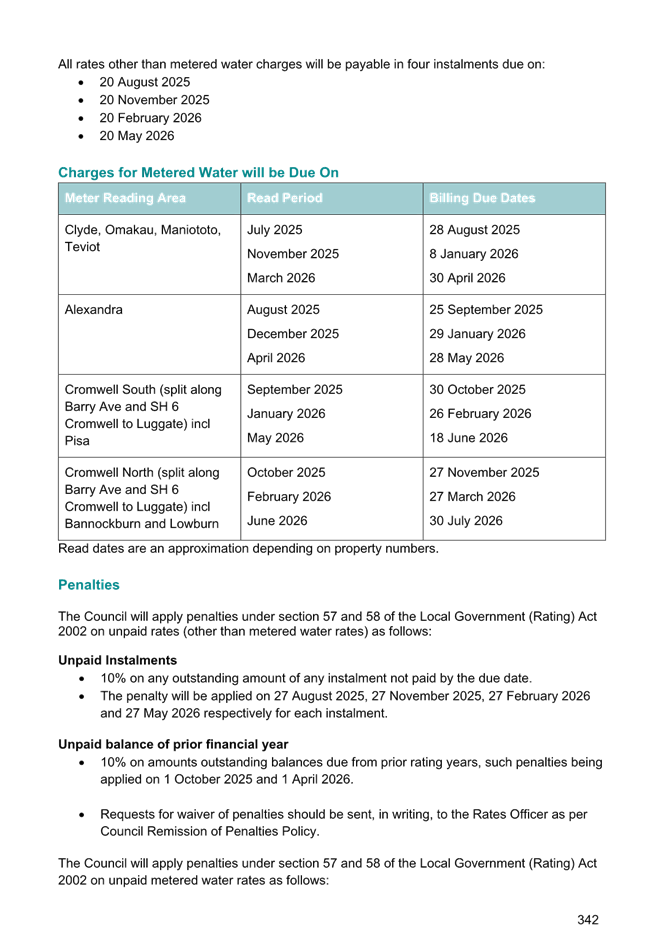

Due Dates

Rates for 2025-26

(other than for metered water) be due for payment in four equal instalments

on the dates as detailed below:

• 20 August 2025

• 20 November 2025

• 20 February 2026

• 20 May 2026

Penalties

Penalties

will be added under sections 57 and 58 of the Local Government

(Rating) Act 2002 to unpaid rates (other than for metered water):

• 10% on any outstanding amount

of any instalment not paid by the due date.

• The penalty will be applied on

27 August 2025, 27 November 2025, 27 February 2026 and 27 May 2026

respectively for each instalment.

• 10% on amounts outstanding from

earlier years, such penalty being applied on 1 October 2025 and

1 April 2026.

Sets the due dates for metered water billing as

follows:

|

Meter

Reading Area

|

Read Period

|

Billing Due Dates

|

|

Clyde, Omakau, Maniototo, Teviot

|

July 2025

November 2025

March 2026

|

28 August 2025

8 January 2026

30 April 2026

|

|

Alexandra

|

August 2025

December 2025

April 2026

|

25 September 2025

29 January 2026

28 May 2026

|

|

Cromwell South (split

along Barry Ave and SH 6 Cromwell to Luggate) including Pisa

|

September 2025

January 2026

May 2026

|

30 October 2025

26 February 2026

18 June 2026

|

|

Cromwell North (split

along Barry Ave and SH 6 Cromwell to Luggate) including Bannockburn and

Lowburn

|

October 2025

February 2026

June 2026

|

27 November 2025

27 March 2026

30 July 2026

|

Penalties will be added for 2025-26 under sections 57 and 58 of the Local Government (Rating)

Act 2002 on unpaid metered water rates as follows:

10% on any metered water rates outstanding after the

due date.

|

Meter

Reading Area

|

Penalty Date

|

|

Clyde, Omakau, Maniototo, Teviot

|

4 September 2025

15 January 2026

7 May 2026

|

|

Alexandra

|

2 October 2025

5 February 2026

4 June 2026

|

|

Cromwell South (split along Barry Ave and SH 6 Cromwell

to Luggate) including Pisa

|

6 November 2025

5 March 2026

25 June 2026

|

|

Cromwell North (split along Barry Ave and SH 6 Cromwell

to Luggate) including Bannockburn and Lowburn

|

4 December 2025

2 April 2026

6 August 2026

|

|

|

|

2. Background

The Local

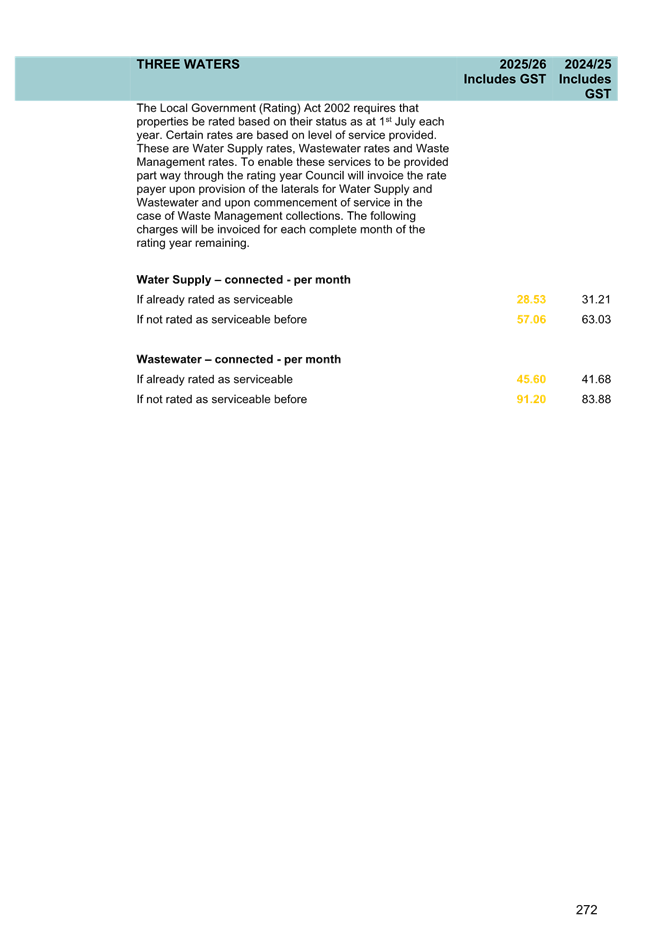

Government (Rating) Act 2002 requires that rates be set

by resolution of Council (Section 23), that due dates be set by resolution of

Council (Section 24) and that penalties be set by resolution of Council

(Sections 57 and 58).

3. Discussion

There is a requirement for

the Council to set the rates for the district every year. The rates being

collected determine the operational and capital expenditure for the Council

during the financial year as detailed in the 2025-34 Long-term plan.

The resolution has had an independent

legal review, and the minor changes that were recommended have been included in

this report.

4. Financial

Considerations

This decision is in-line with

the overall plans and budgets of the 2025-26 financial year. It also ensures

compliance of the Local Government Act 2002 and Local Government (Rating) Act

2002.

The financial impact of

adopting this plan and any amendments (if applicable) are significant as it

determines the operational and capital expenditure for the 2025-26 financial

year and how these are funded from rates, activity revenue, reserves and loans.

5. Options

Option 1 –

(Recommended)

Council sets the rates for

2025-26 financial year, including setting the instalment dates, application of

penalties and the amount of the penalties.

Advantages:

· Meets

legislative requirements.

· Allows

Council to assess and collect rates for 2025-26.

· Continues

with the programme of work contained within the 2025-34 Long-term Plan.

Disadvantages:

· None.

Option 2

That Council does not set

the rates for 2025-26 financial year, including setting the instalment dates,

application of penalties and the amount of the penalties.

Advantages:

· None.

Disadvantages:

· Breach

of Local Government Act 2002, section 95(3) “An annual plan must be

adopted before the commencement of the year to which it relates”.

· Does

not allow Council to assess and collect rates for 2025-26 which would result in

significant financial implications for council.

6. Compliance

|

Local Government Act 2002 Purpose Provisions

|

The

resolution to set rates, due dates and penalties is a direct result of

Council’s adherence to the Local Government (Rating) Act 2002 and the

Local Government Act 2002.

This

has been supported by a consultation process which enables democratic local

decision making and action by, and on behalf of the community.

AND

This decision promotes the

(social/cultural/economic/environmental) wellbeing of the community, in the

present and for the future by giving consideration to the communities

preference for their district included in the 2025-34 Long-term Plan.

|

|

Decision consistent with other Council plans and policies? Such as

the District Plan, Economic Development Strategy etc.

|

Yes

|

|

Considerations as to sustainability, the environment and climate

change impacts

|

These have all been considered as part of the 2025-34 Long-term

Plan.

|

|

Risks Analysis

|

A

failure to set the rates by resolution would result in Council not being able

to set and collect rates or penalties for 2025-26.

|

|

Significance, Consultation and Engagement (internal and external)

|

The decision to adopt this report is significant as

adoption will approve setting of the 2024-25

rates.

|

7. Next

Steps

Rates assessments and

invoices will be provided to ratepayers from July 2025 onwards, as required in

the Local Government (Rating) Act 2002.

The Rating Policy will be

made available on the Council website, along with Council’s resolution

from this report.

8. Attachments

Nil