|

|

|

AGENDA

Ordinary Council

Meeting

Wednesday, 27 April 2022

|

|

Date:

|

Wednesday, 27 April 2022

|

|

Time:

|

10.30 am

|

|

Location:

|

Ngā Hau e Whā, William Fraser Building,

1 Dunorling Street, Alexandra

(Due to

COVID-19 restrictions and limitations of the physical space, public access

will be available through a live stream of the meeting.

The link to the live stream will be available on the

Central Otago District Council's website.)

|

|

Sanchia Jacobs

Chief Executive Officer

|

Members His

Worship the Mayor T Cadogan (Chairperson), Cr N Gillespie, Cr T Alley, Cr S Calvert,

Cr L Claridge, Cr I Cooney, Cr S Duncan, Cr S Jeffery, Cr C Laws, Cr N

McKinlay, Cr M McPherson, Cr T Paterson

In Attendence S Jacobs (Chief Executive

Officer), L Macdonald (Executive Manager - Corporate Services), J Muir

(Executive Manager - Infrastructure Services), L van der Voort (Executive

Manager - Planning and Environment), S Righarts (Chief Advisor), M De Cort

(Communications Coordinator), W McEnteer (Governance Manager)

1 Apologies

2 Public

Forum

3 Confirmation

of Minutes

Ordinary Council Meeting - 9 March

2022

|

Council Meeting Agenda

|

27 April 2022

|

MINUTES

OF A Council Meeting

OF THE Central Otago District

Council

HELD ON Microsoft Teams

and Live Streamed

ON Wednesday, 9 March

2022 COMMENCING AT 10.30 am

PRESENT: His

Worship the Mayor T Cadogan (Chairperson), Cr N Gillespie, Cr T Alley, Cr S

Calvert, Cr I Cooney, Cr S Duncan, Cr S Jeffery, Cr C Laws,

Cr N McKinlay, Cr M McPherson, Cr T Paterson

IN ATTENDANCE: S Jacobs (Chief Executive

Officer), L Macdonald (Executive Manager - Corporate Services), L van der

Voort (Executive Manager - Planning and Environment), S Righarts (Chief

Advisor), A Crosbie (Senior Strategy Advisor), J McCallum (Roading

Manager), L Webster (Regulatory Services Manager), L Stronach (Team Leader

Statutory Property), C Martin (Property and Facilities Officer - Vincent and

Teviot Valley), N Lanham (Economic Development Manager), I Evans (Water Services

Manager), Quinton Penniall (Environmental Services Manager),

M De Cort (Communications Coordinator), R Williams (Governance

Manager) and W McEnteer (Governance Support Officer)

1 Apologies

|

Apology

|

|

Resolution

Moved: Paterson

Seconded: Cadogan

That the apology received from Cr Claridge be accepted.

Carried

|

2 Public

Forum

Glen

Christiansen – Chair, Central Otago Community Housing Trust

Mr Christiansen spoke

about Council’s role in affordable housing, and specifically the paper

being considered on the agenda. He discussed the formation of the trust,

and the current housing and rental market situation in Central Otago. He

advocated for the secure homes model to be initiated in Central Otago. Mr

Christiansen then responded to questions.

3 Confirmation

of Minutes

|

Resolution

Moved: Duncan

Seconded: McPherson

That the public minutes of the Ordinary Council Meeting

held on 26 January 2022 be confirmed as a true and correct record.

Carried

|

4 Declaration

of Interest

Members were reminded of their obligations in respect of

declaring any interests. There were no further declarations of interest.

5 Reports

Note: Cr Duncan assumed the Chair as the Roading

portfolio lead.

|

22.2.2 Safer

Speeds Bylaw

|

|

To

consider approving the Statement of Proposal for the proposed Speed Limits

Bylaw 2022 for public consultation.

|

|

Resolution

Moved: Alley

Seconded: Jeffery

That the Council

A. Receives

the report and accepts the level of significance.

B. Agrees that a bylaw is

the most appropriate way of addressing the perceived problem, and the

proposed bylaw is the most appropriate form and does not give rise to any

implications under the Bill of Rights Act 1990.

C. Approves the Statement

of Proposal for the proposed Speed Limit Bylaw 2022 for public consultation.

D. Appoints

Crs Alley, Duncan and Paterson to hear submissions, if necessary.

Carried

|

Note: Cr

Jeffery assumed the Chair as the Economic Development and Community Facilities

portfolio lead.

|

22.2.3 Economic

Development Work Programme Progress Report

|

|

To provide an update on the

implementation of the Economic Development Work programme for 2021/22.

|

|

Resolution

Moved: Duncan

Seconded: Alley

That the report be received.

Carried

|

Note: Cr Gillespie assumed the Chair as the Planning

and Regulatory portfolio lead.

|

22.2.4 Dangerous

and Insanitary Buildings Policy

|

|

To

consider the adoption of the proposed Dangerous and Insanitary Buildings

Policy.

|

|

Resolution

Moved: Calvert

Seconded: Cadogan

That the Council

A. Receives

the report and accepts the level of significance.

B. Adopts the proposed

Dangerous and Insanitary Buildings Policy.

Carried

|

Note: Cr McKinlay assumed the Chair as the Three

Waters and Waste portfolio lead.

|

22.2.5 Taumata

Arowai Consultation January 2022

|

|

To

inform elected members of consultation documents recently circulated by

Taumata Arowai.

|

|

Resolution

Moved: Jeffery

Seconded: Laws

That the report be received.

Carried

|

|

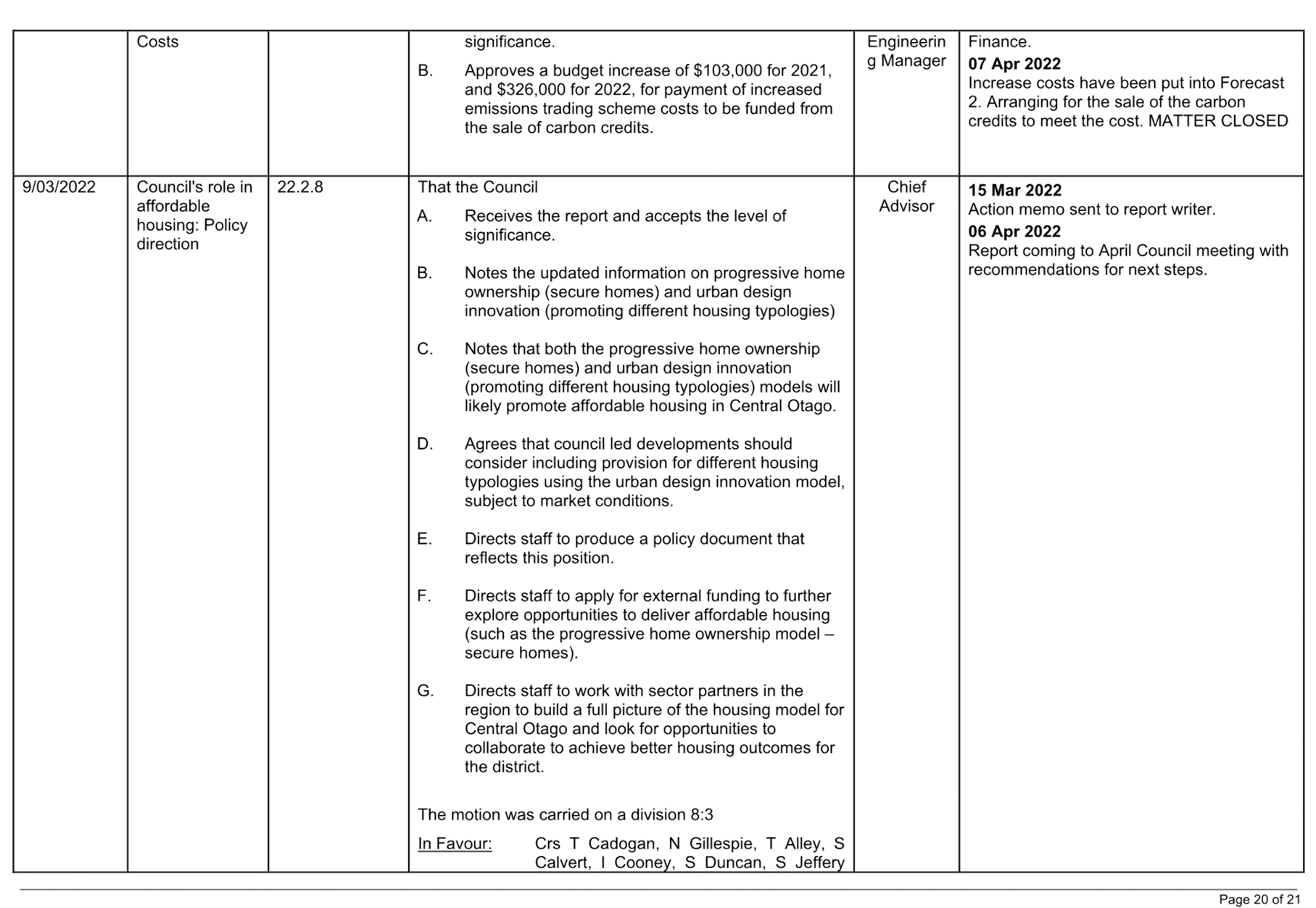

22.2.6 Emissions

Trading Scheme Costs

|

|

To

consider the cost increases associated with the Emissions Trading Scheme for

2021 and 2022. A question was raised if the carbon credits were a district or

ward asset.

|

|

Resolution

Moved: McPherson

Seconded: Cadogan

That the Council

A. Receives

the report and accepts the level of significance.

B. Approves a budget

increase of $103,000 for 2021, and $326,000 for 2022, for payment of

increased emissions trading scheme costs to be funded from the sale of carbon

credits.

Carried

|

Note: The Mayor assumed the Chair.

Note: Cr Duncan left the meeting at 12:07 pm.

|

22.2.7 Review

into the future for local government

|

|

To

consider the key questions in the interim report on the Review into the

Future for Local Government and the key shifts the Panel believe are required

in advance of a discussion with the Panel on 24 March 2022.

|

|

Resolution

Moved: Cadogan

Seconded: McPherson

That the report be received.

Carried

|

Note: Cr Duncan returned to

the meeting at 12:38 pm.

|

22.2.8 Council's

role in affordable housing: Policy direction

|

|

To agree on the policy direction

for Council’s role in affordable housing.

After discussion it was agreed

that staff would develop options for consultation to gauge the support for an

affordable housing model in Central Otago. Staff would present those options

to Council at a future meeting. The resolution was amended accordingly.

|

|

Resolution

Moved: Gillespie

Seconded: Cadogan

That the Council

A. Receives the report and accepts the level of

significance.

B. Notes the updated information on progressive home

ownership (secure homes) and urban design innovation (promoting different

housing typologies)

C. Notes that both the progressive home ownership (secure

homes) and urban design innovation (promoting different housing typologies)

models will likely promote affordable housing in Central Otago.

D. Agrees that council led developments should consider

including provision for different housing typologies using the urban design

innovation model, subject to market conditions.

E. Directs staff to produce a policy document that reflects

this position.

F. Directs staff to apply for external funding to further

explore opportunities to deliver affordable housing (such as the progressive

home ownership model – secure homes).

G. Directs staff to work with sector partners in the region

to build a full picture of the housing model for Central Otago and look for

opportunities to collaborate to achieve better housing outcomes for the

district.

The motion

was carried on a division 8:3

In

Favour: Crs T Cadogan, N Gillespie, T

Alley, S Calvert, I Cooney, S Duncan, S Jeffery and C Laws

Against: Crs

N McKinlay, M McPherson and T Paterson

Carried 8/3

|

Note: The meeting adjourned at 1:03 pm and resumed at

1:31 pm.

Note: Crs Cooney and McKinlay returned to the meeting

at 1:33 pm.

Note: Cr Laws returned to the meeting at 1:34 pm.

Note: Cr Duncan returned to the meeting at 1:36 pm.

|

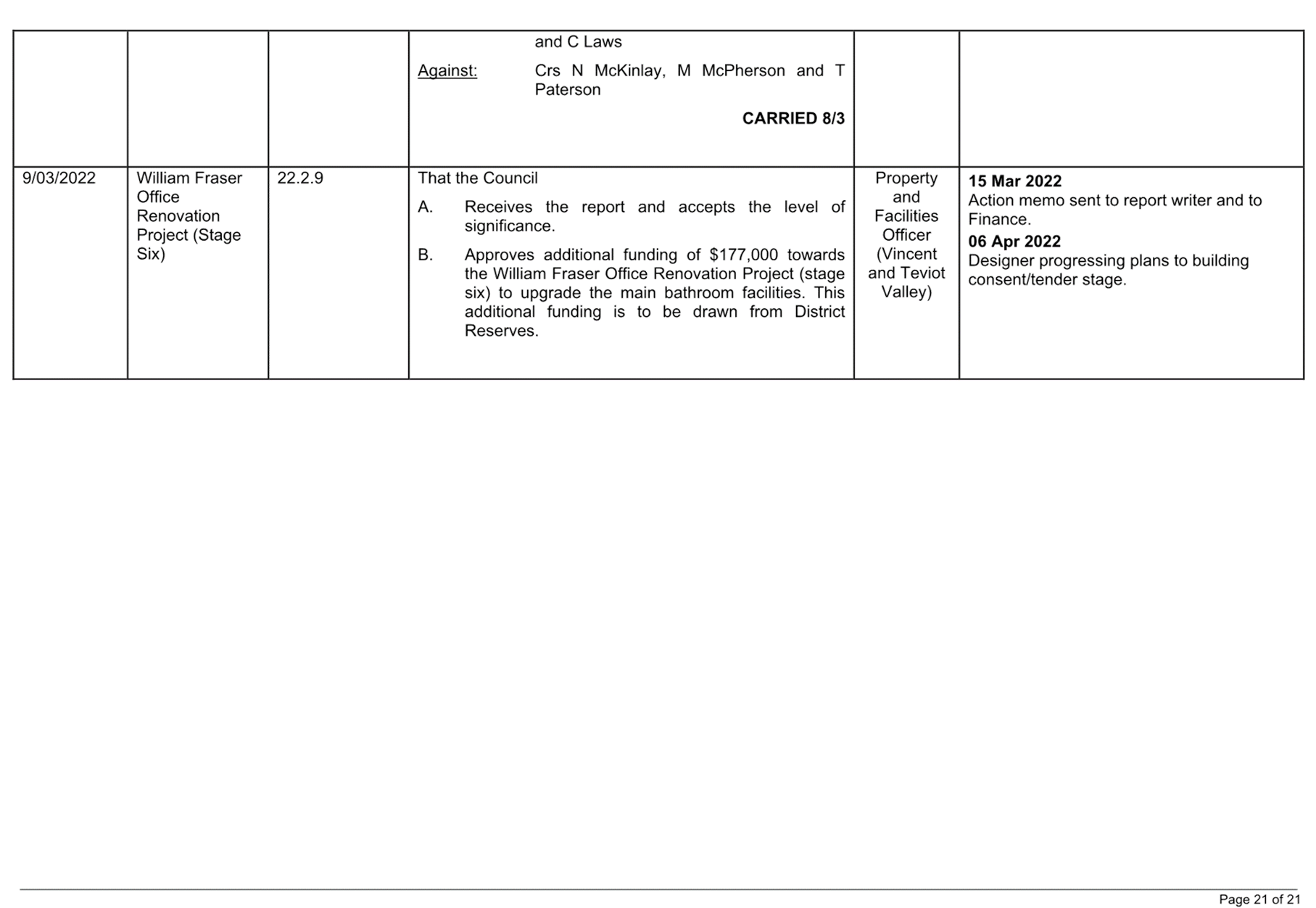

22.2.9 William

Fraser Office Renovation Project (Stage Six)

|

|

To

consider additional funding of the William Fraser Office Renovation Project

(stage six) to upgrade the main bathroom facilities of the building.

|

|

Resolution

Moved: Paterson

Seconded: Calvert

That the Council

A. Receives

the report and accepts the level of significance.

B. Approves

additional funding of $177,000 towards the William Fraser Office Renovation

Project (stage six) to upgrade the main bathroom facilities. This additional

funding is to be drawn from District Reserves.

Carried

|

|

22.2.10 Application

to Lease site at the Cromwell Wastewater Treatment Plant

|

|

To

consider granting a lease to Climate Solutions

Aotearoa Limited over part of Section 1 Survey Office Plan 20776 being

part of the Cromwell Wastewater Treatment Plant land.

After

discussion it was clarified that environmental waste was the type of waste to

be collected for the purpose of a worm farm and associated activities.

|

|

Resolution

Moved: Calvert

Seconded: Cadogan

That the Council

A. Receives

the report and accepts the level of significance.

B. Agrees

to grant Climate Solutions Aotearoa Limited a lease over approximately one

hectare of the Cromwell Wastewater Treatment Plant land, being part of

Section 1 Survey Office Plan 20776 (as shown in figure 1), for the purpose of

establishing and operating an environmental waste collection (worm farm and

associated activities) and material recovery business, on the following terms

and conditions:

- Initial term: Five

(5) Years

- Renewals: Three

(3) Rights of Renewal of Five (5) Years each

- Rental: Market

Rental (at valuation by independent valuer)

- Rent Reviews: On

first renewal and two yearly thereafter

- Rent Review

Methodology: Market Rental (at valuation

by independent valuer)

- Area: Approximately

1 hectare

Subject to the Climate

Solutions Aotearoa:

- Obtaining all

consents and permits associated with the operation of the business.

- Erecting security

(deer) fencing along the northern and eastern (internal) boundaries.

- Installing

security (deer) gates to provide for access from Richards Beach Road and for

exit via the unnamed road to the south of the lease area.

- Paying all costs

associated with preparing the lease area for their purposes.

- Paying all costs

associated with connecting the services and to utility networks.

- Not

impacting on the day to day operation of the wastewater treatment plant.

C. Authorises

the Chief Executive to do all that is necessary to give effect to the

resolution.

Carried

|

|

22.2.11 Financial

Report For The Period Ending 31 December 2021

|

|

To consider the financial

performance for the period ending 31 December 2021.

|

|

Resolution

Moved: Cadogan

Seconded: McKinlay

That the report be received.

Carried

|

|

22.2.12 Appointments

to External Bodies

|

|

To

consider the Council’s appointments to external organisations.

|

|

Resolution

Moved: Cadogan

Seconded: McPherson

That the Council

A. Receives

the report and accepts the level of significance.

B. Agrees that the

delegations register is updated to remove the Alexandra District Museum Inc.

from the list of external appointments.

C. Work with the committees

of Central Otago Wilding Conifer Control Group and the Maniototo Curling

International to change its representative roles to liaison positions.

Carried

|

|

22.2.13 Updated

2022 Meeting Schedule

|

|

To

approve an updated schedule of meetings for 2022.

|

|

Resolution

Moved: Cadogan

Seconded: Calvert

That the Council

A. Receives

the report and accepts the level of significance.

B. Adopts

the updated 2022 meeting schedule.

Carried

|

Note: His Worship the Mayor

recognised the contribution of the Governance Manager during her tenure and

wished her well for her new role.

6 Mayor’s

Report

|

22.2.14 March

2022 Mayor's Report

His Worship the Mayor spoke to his report. In

addition he outlined the recommendations of the

Three Waters Working Group he had been sitting on, whose recommendations had

recently become public. He then responded to questions.

|

|

Resolution

Moved: Cadogan

Seconded: Gillespie

That the Council receives the report.

Carried

|

7 Status

Reports

|

22.2.15 March

2022 Governance Report

|

|

To report on items of general

interest, receive minutes and updates from key organisations, consider

Council’s forward work programme, business plan and the legacy and

current status report updates.

|

|

Resolution

Moved: Cadogan

Seconded: Laws

That the Council receives the report.

Carried

|

8 Community

Board Minutes

|

22.2.16 Minutes

of the Vincent Community Board Meeting held on 1 February 2022

|

|

Resolution

Moved: Cadogan

Seconded: McPherson

That the unconfirmed Minutes of the Vincent Community

Board Meeting held on 1 February 2022 be noted.

Carried

|

|

22.2.17 Minutes

of the Teviot Valley Community Board Meeting held on 3 February 2022

|

|

Resolution

Moved: Cadogan

Seconded: McPherson

That the unconfirmed Minutes of the Teviot Valley

Community Board Meeting held on 3 February 2022 be noted.

Carried

|

|

22.2.18 Minutes

of the Cromwell Community Board Meeting held on 15 February 2022

|

|

Resolution

Moved: Cadogan

Seconded: McPherson

That the unconfirmed Minutes of the Cromwell Community

Board Meeting held on 15 February 2022 be noted.

Carried

|

|

22.2.19 Minutes

of the Maniototo Community Board Meeting held on 17 February 2022

|

|

Resolution

Moved: Cadogan

Seconded: McPherson

That the unconfirmed Minutes of the Maniototo Community

Board Meeting held on 17 February 2022 be noted.

Carried

|

9 Committee

Minutes

|

22.2.20 Minutes

of the Audit and Risk Committee Meeting held on 25 February 2022

|

|

Resolution

Moved: Cadogan

Seconded: McPherson

That the unconfirmed Minutes of the Audit and Risk

Committee Meeting held on 25 February 2022 be noted.

Carried

|

10 Date

of Next Meeting

Following item 22.2.13,

the date of the next scheduled meeting was changed to 27 April

2022.

11 Resolution

to Exclude the Public

|

Resolution

Moved: Cadogan

Seconded: Gillespie

That the public be excluded from the following parts of

the proceedings of this meeting.

The general subject matter of each matter to be considered

while the public is excluded, the reason for passing this resolution in

relation to each matter, and the specific grounds under section 48 of the

Local Government Official Information and Meetings Act 1987 for the passing

of this resolution are as follows:

|

General subject of each matter to be

considered

|

Reason for passing this resolution in

relation to each matter

|

Ground(s) under section 48 for the

passing of this resolution

|

|

Confidential Minutes of Ordinary

Council Meeting

|

s7(2)(b)(ii) - the withholding of the information

is necessary to protect information where the making available of the

information would be likely unreasonably to prejudice the commercial

position of the person who supplied or who is the subject of the

information

s7(2)(h) - the withholding of the information is

necessary to enable Council to carry out, without prejudice or

disadvantage, commercial activities

s7(2)(i) - the withholding of the information is

necessary to enable Council to carry on, without prejudice or disadvantage,

negotiations (including commercial and industrial negotiations)

|

s48(1)(a)(i) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

22.2.21 - March 2022 Confidential

Governance Report

|

s7(2)(i) - the withholding of the information is

necessary to enable Council to carry on, without prejudice or disadvantage,

negotiations (including commercial and industrial negotiations)

|

s48(1)(a)(i) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

22.2.22 - Confidential Minutes of the

Vincent Community Board Meeting held on 1 February 2022

|

s7(2)(i) - the withholding of the information is

necessary to enable Council to carry on, without prejudice or disadvantage,

negotiations (including commercial and industrial negotiations)

|

s48(1)(a)(i) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

22.2.23 - Confidential Minutes of the

Cromwell Community Board Meeting held on 15 February 2022

|

s7(2)(a) - the withholding of the information is

necessary to protect the privacy of natural persons, including that of

deceased natural persons

s7(2)(b)(ii) - the withholding of the information

is necessary to protect information where the making available of the

information would be likely unreasonably to prejudice the commercial

position of the person who supplied or who is the subject of the

information

s7(2)(h) - the withholding of the information is

necessary to enable Council to carry out, without prejudice or

disadvantage, commercial activities

s7(2)(i) - the withholding of the information is

necessary to enable Council to carry on, without prejudice or disadvantage,

negotiations (including commercial and industrial negotiations)

|

s48(1)(a)(i) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

22.2.24 - Confidential Minutes of the

Maniototo Community Board Meeting held on 17 February 2022

|

s7(2)(i) - the withholding of the information is

necessary to enable Council to carry on, without prejudice or disadvantage,

negotiations (including commercial and industrial negotiations)

|

s48(1)(a)(i) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

22.2.25 - Confidential Minutes of the

Audit and Risk Committee Meeting held on 25 February 2022

|

s7(2)(a) - the withholding of the information is

necessary to protect the privacy of natural persons, including that of

deceased natural persons

s7(2)(b)(ii) - the withholding of the information

is necessary to protect information where the making available of the

information would be likely unreasonably to prejudice the commercial

position of the person who supplied or who is the subject of the

information

s7(2)(c)(ii) - the withholding of the information

is necessary to protect information which is subject to an obligation of

confidence or which any person has been or could be compelled to provide

under the authority of any enactment, where the making available of the

information would be likely otherwise to damage the public interest

s7(2)(d) - the withholding of the information is

necessary to avoid prejudice to measures protecting the health or safety of

members of the public

s7(2)(g) - the withholding of the information is

necessary to maintain legal professional privilege

s7(2)(i) - the withholding of the information is

necessary to enable Council to carry on, without prejudice or disadvantage,

negotiations (including commercial and industrial negotiations)

|

s48(1)(a)(i) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

22.2.26 - Chief Executive Officer's

Contract

|

s7(2)(a) - the withholding of the information is

necessary to protect the privacy of natural persons, including that of

deceased natural persons

|

s48(1)(a)(i) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

Carried

|

The public were excluded at 2.32 pm and the meeting closed

at 2.53 pm.

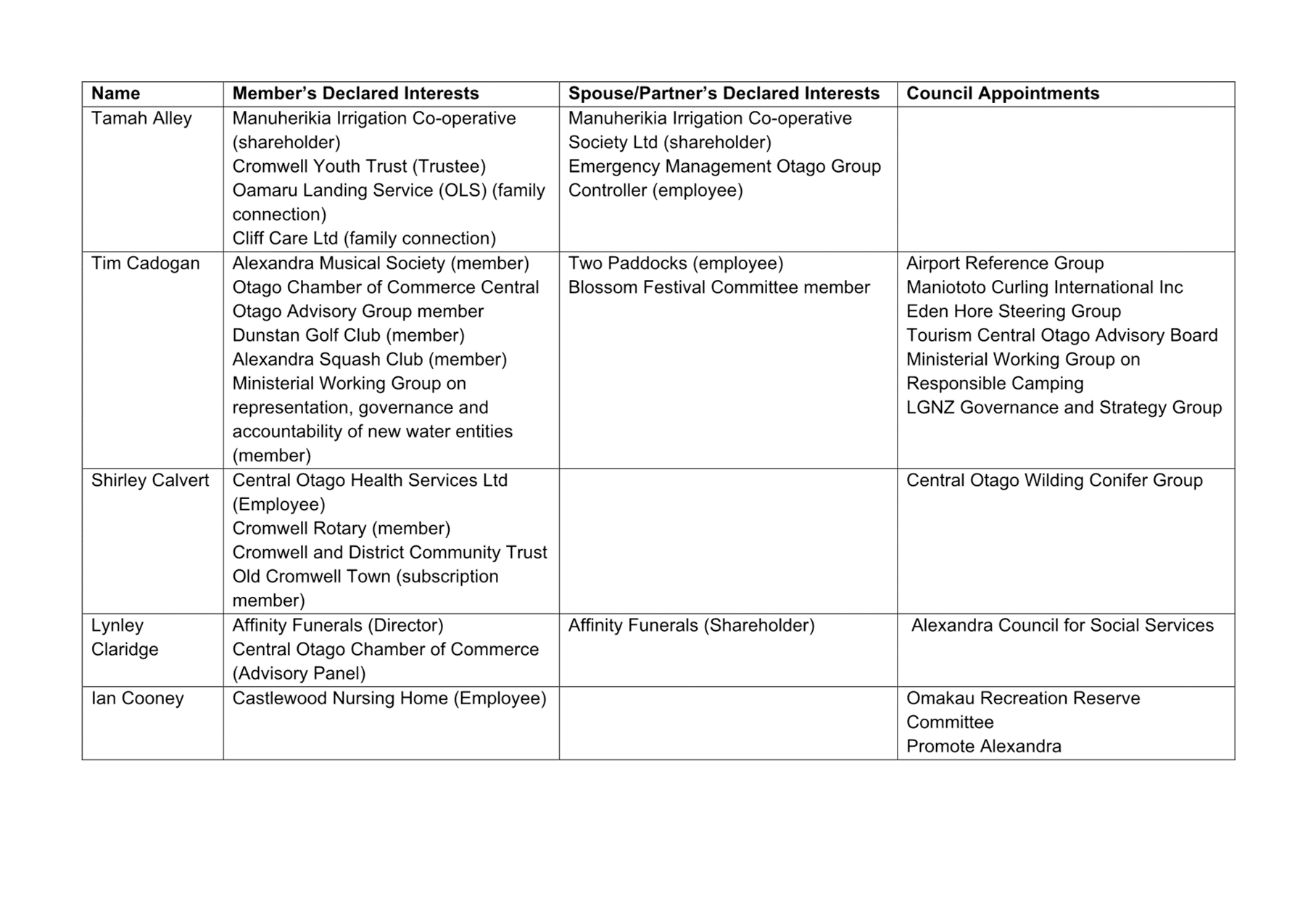

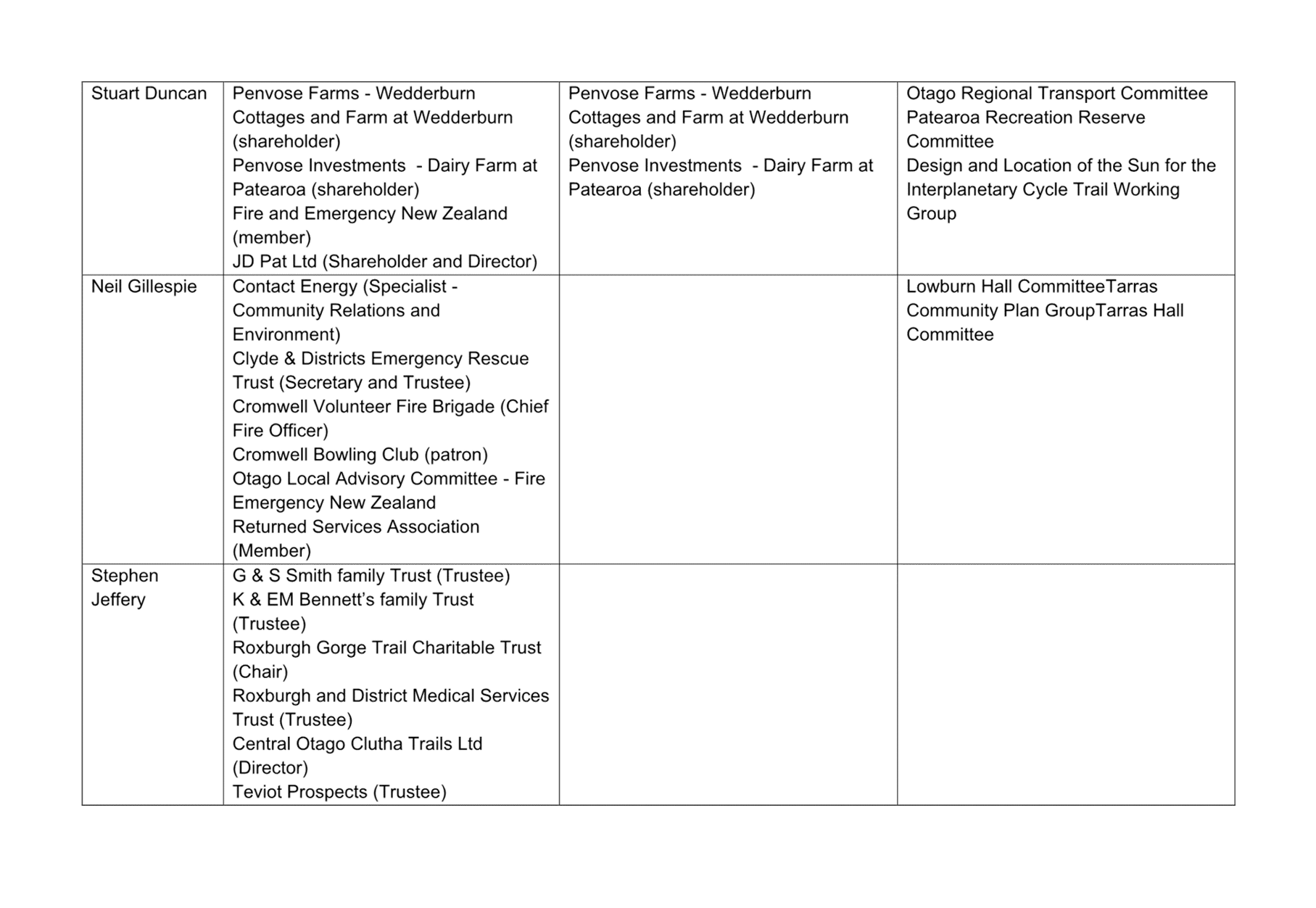

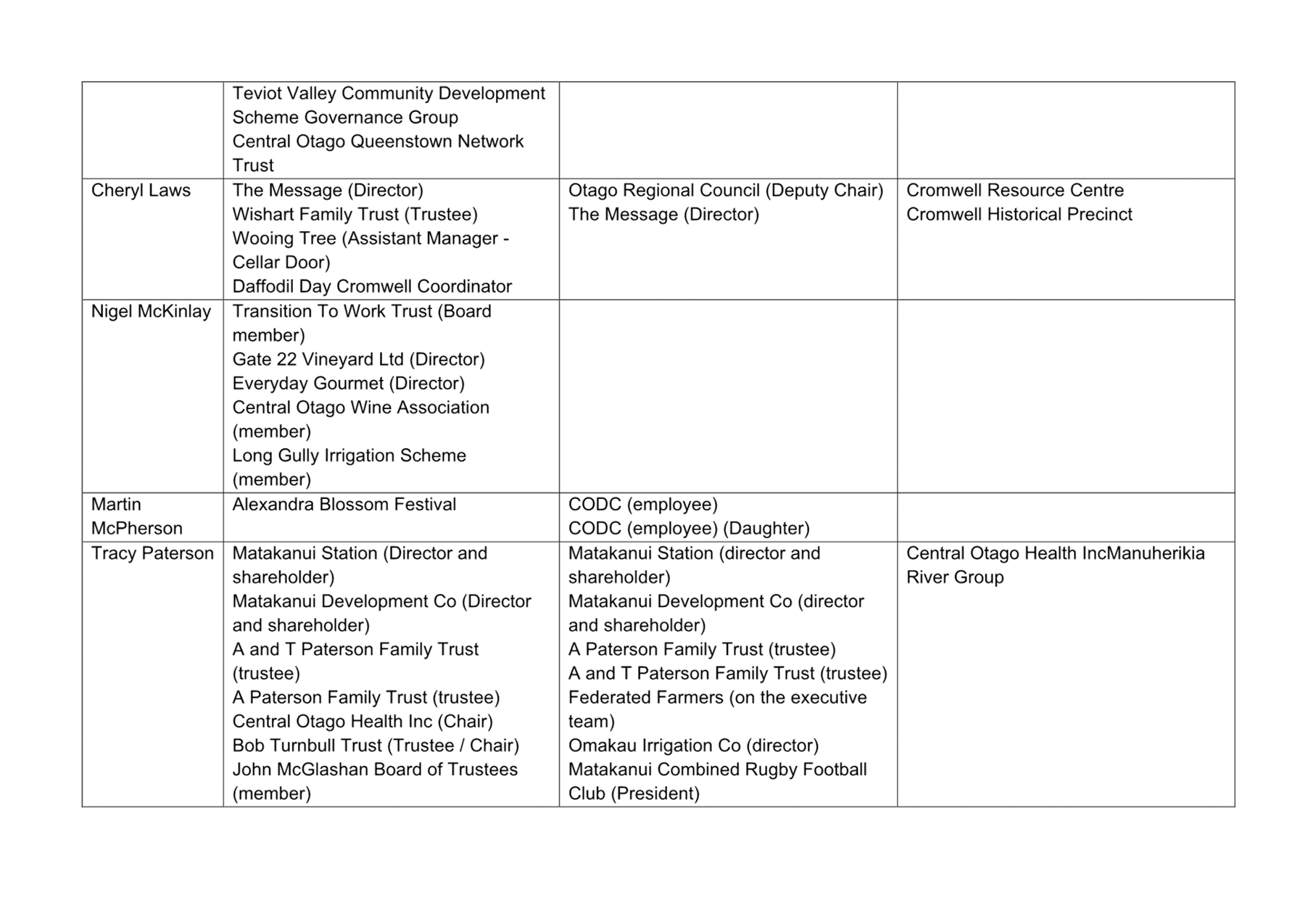

4 Declaration

of Interest

22.3.1 Declarations

of Interest Register

Doc ID: 577675

1. Purpose

Members are reminded of the need to be vigilant to stand

aside from decision making when a conflict arises between their role as a

member and any private or other external interest they might have.

2. Attachments

Appendix 1 - Council Declarations

of Interest ⇩

|

Council

meeting

|

27 April

2022

|

5 Reports

22.3.2 Request

for Information from Director General of Health regarding Fluoridation of

Community Water Supplies

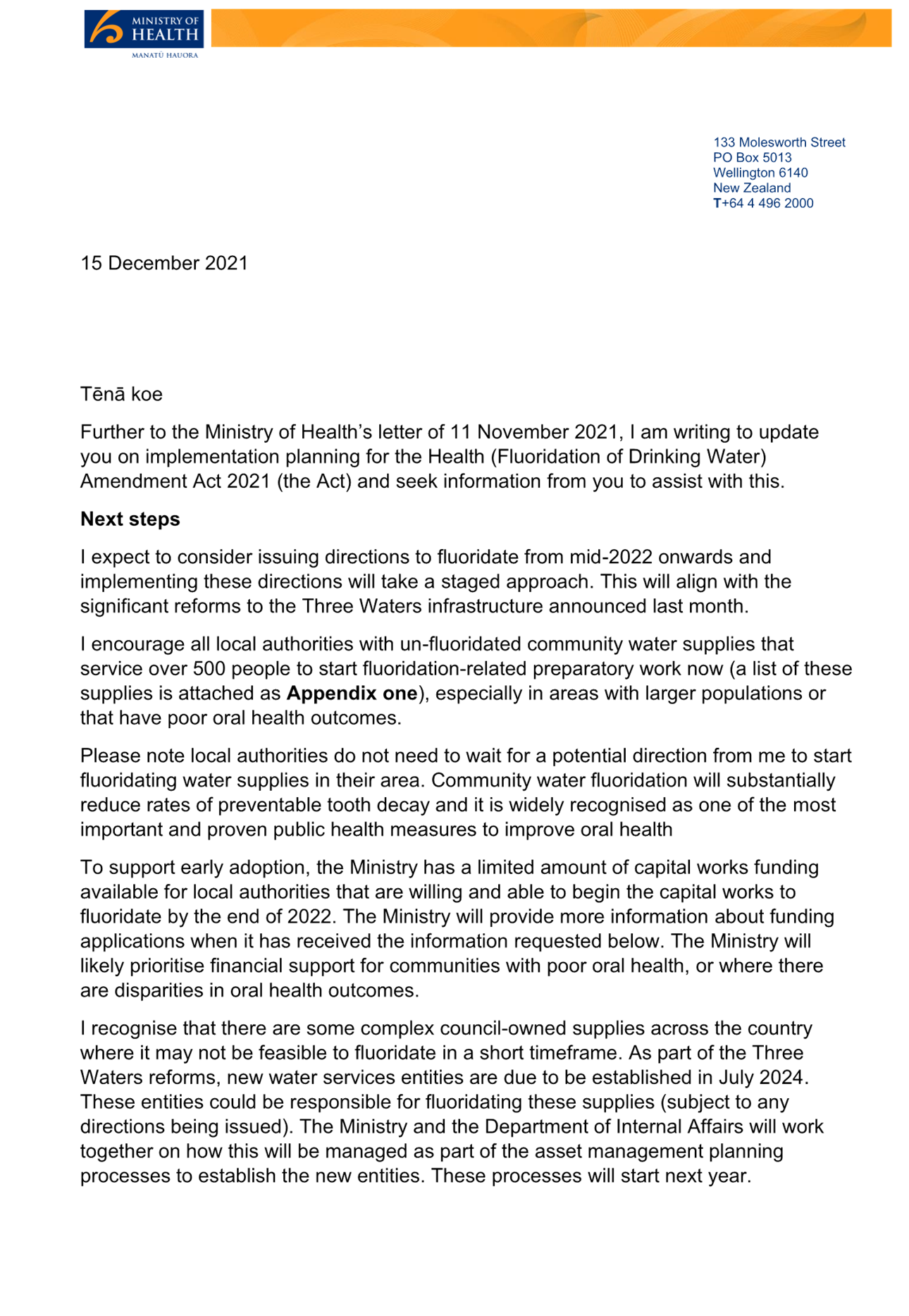

Doc ID: 574093

1. Purpose

To provide an update on

the Ministry of Health’s implementation for the Health (Fluoridation of

Drinking Water) Amendment Act 2021.

|

Recommendations

That the report be received.

|

2. Discussion

Following the Health

(Fluoridation of Drinking Water) Amendment Act 2021 passing into law last year,

the decision to fluoridate a drinking supply has moved from local government to

the Director General of Health.

Through correspondence

with all councils the Ministry of Health (the Ministry) is signalling that

drinking water supplies serving more than 500 people will eventually be

required to include fluoridation. It has been previously indicated that the

mandating process is likely to get under way by mid-2022 though there is no

indication of which areas will be targeted.

In December 2021

correspondence from the Ministry (attached) also included a request for

information on individual sites that serve over 500 people that are not

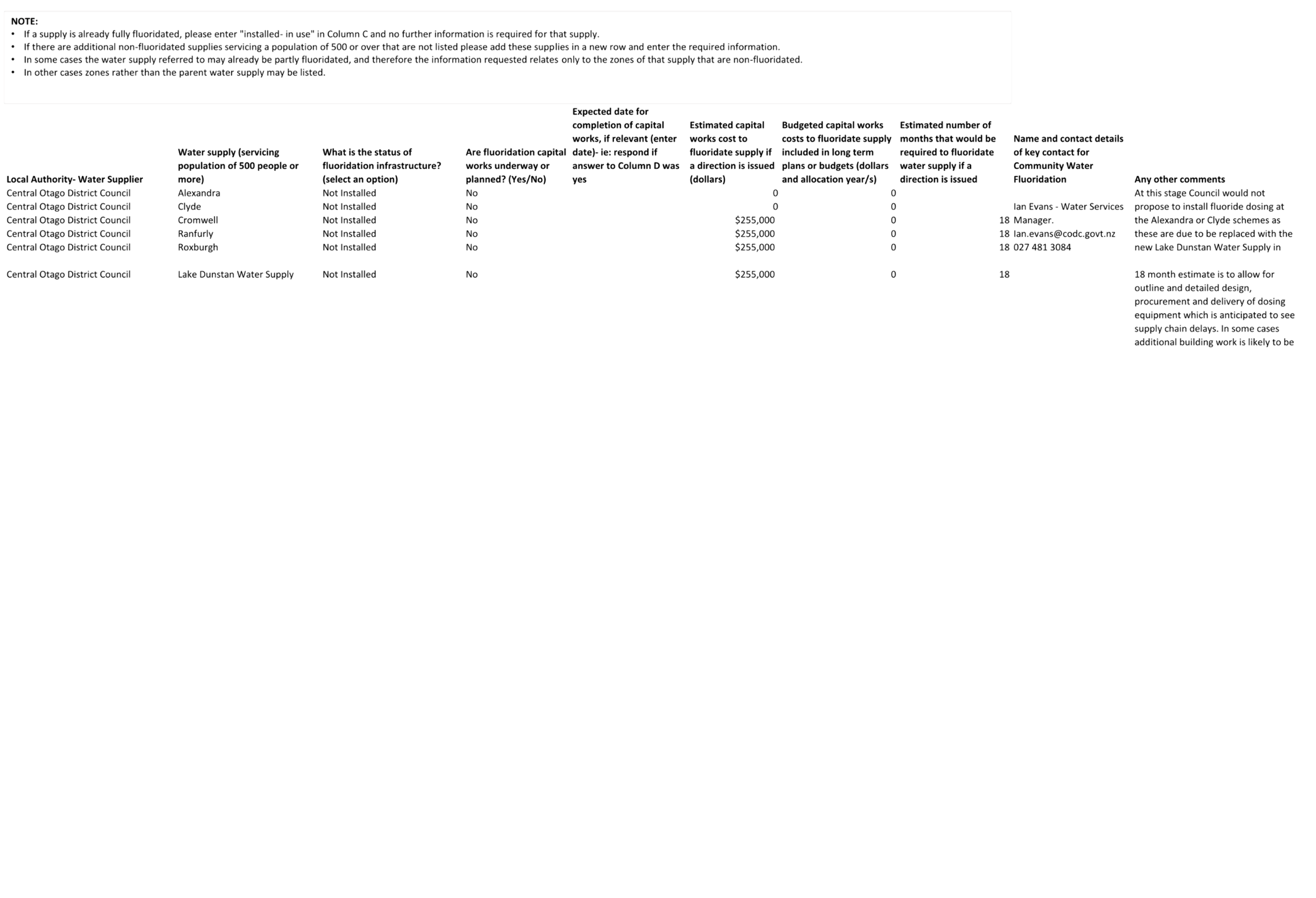

currently fluoridated. For Council this includes the following:

· Alexandra

· Clyde

· Cromwell

· Ranfurly

· Roxburgh

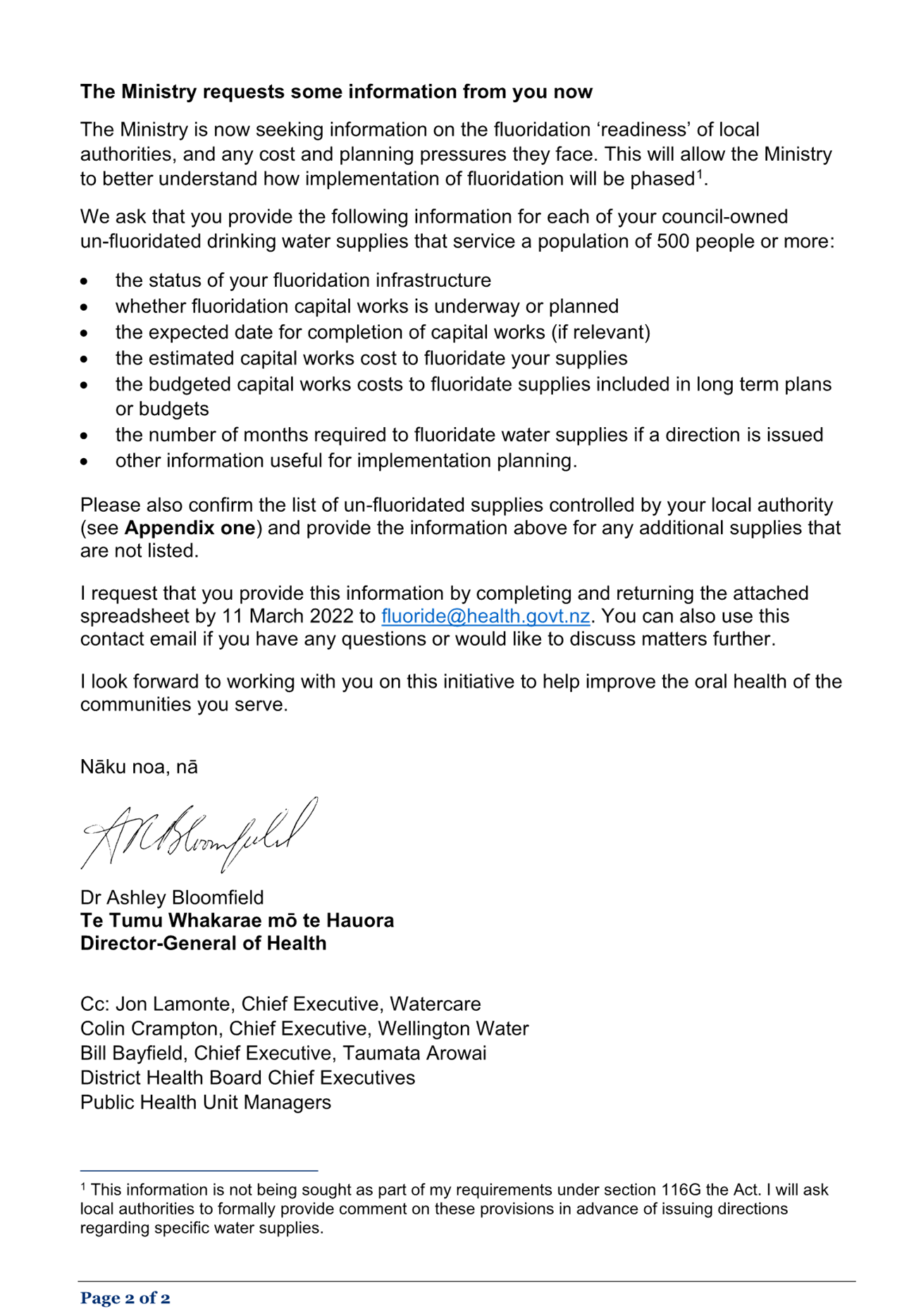

No allowance has been

budgeted in the 2021 Long Term Plan to include dosing fluoride at any of

council’s water supplies. If a directive is issued by the Director

General of Health, water suppliers will be required to comply under the Act,

although at this stage there is no set date for compliance.

Estimates of the potential

costs to upgrade have been prepared to enable Council to complete the

information request and respond to the Ministry (attached). The Ministry have

been advised that if mandated, the logical sequencing would be to include

fluoridation as existing treatment plants are upgraded, with the new Lake

Dunstan Water treatment plant occurring first. A review has been undertaken to

confirm that there is sufficient space to include fluoridation within the site

layout at the new Lake Dunstan treatment site. Current estimates indicate a

cost of approximately $255,000 per site.

A small contestable fund

is available for suppliers who can commit to completing a fluoridation upgrade

by the end of 2022. This is likely to only benefit suppliers with planned

upgrades already under way. It is unlikely that Council can benefit from this

round of funding due to lead times for design and material supply. The

Lake Dunstan Water Supply will not qualify for this funding as commissioning

will not occur until 2023.

The decision to fluoridate

supplies with a population under 500 population continues to be the

responsibility of the water suppliers, and this has not been transferred to the

Ministry of Health.

3. Attachments

Appendix 1 - Letter to local

authority CEs ⇩

Appendix 2 - Community Water

Fluoridation questionaire CODC response ⇩

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Ian Evans

|

Julie

Muir

|

|

Water

Services Manager

|

Executive

Manager - Infrastructure Services

|

|

24/03/2022

|

30/03/2022

|

|

Council

meeting

|

27 April

2022

|

|

Council meeting

|

27 April

2022

|

22.3.3 Proposed

Road Stopping - Unnamed Unformed Road off Poole Road (previously known as/part

of Boundary Road).

Doc ID: 572027

1. Purpose of Report

To consider a proposal to

stop an unnamed unformed road off Poole Road in accordance with the provisions

of the Local Government Act 1974.

|

Recommendations

That the Council

A. Receives the

report and accepts the level of significance.

B. Approves the proposal

to stop the unnamed unformed road off the northern end of Poole Road, subject

to:

- The provisions of the Local Government Act 1974.

- The public notification process outlined in the

same Act.

- No objections being received within the public

notification period.

- The Road being surveyed into three parcels as

shown in figure 11 (overview of proposed stopping).

- The area marked “A” in figure 11,

being stopped, classified as recreation reserve, then amalgamated with Lot 24

DP 3194 in accordance with the provisions of the Reserves Act 1977.

- The areas marked “B” and

“C” in figure 11, being stopped, classified as recreation

reserve, then vested in the Central Otago District Council in accordance with

the provisions of the Reserves Act 1977.

- An easement (in gross) in favour of (and as

approved by) Aurora Energy Limited being registered over the areas marked

“A”, “B”, and “C”, as shown in figure 11

to protect the infrastructure identified in figure 13.

- The costs outlined in table 1 being paid from the

Dunstan Park Development account.

C. Authorises

the Chief Executive to do all that is necessary to give effect to the

resolution.

|

2. Background

Boundary Road (Alexandra)

used to run northeast from Alexandra Wastebusters, across the Alexandra-Clyde

Road through Molyneux Park, to the Central Otago Netball pavilion. It then

veered northwest through Dunstan Park to the Alexandra Golf Club (AGC) clubhouse.

The southern end of

Boundary Road between Alexandra Wastebusters and the Clyde-Alexandra Road is

formed and sealed. It has length of approximately 880 metres.

The middle section of

Boundary Road, from the Clyde-Alexandra Road through Molyneux Park to the

entrance to the Alexandra Netball pavilion, is formed and sealed. It has a

length of approximately 550 metres.

In April 2021, this middle

section of Boundary Road was renamed Poole Road. The purpose of the renaming

was to resolve an historic street numbering issue.

The northern end of

Boundary Road, between Molyneux Park and the AGC clubhouse, is unformed. It has

a length approximately 1060 metres. It is now an unnamed section of legal road.

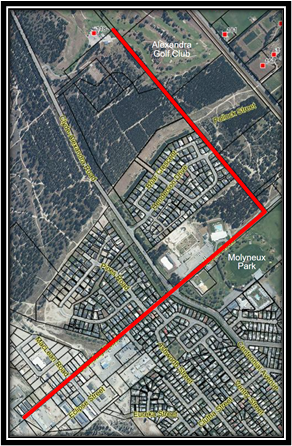

An overview of Boundary

Road, prior to the renaming exercise, is shown in red below in figure 1.

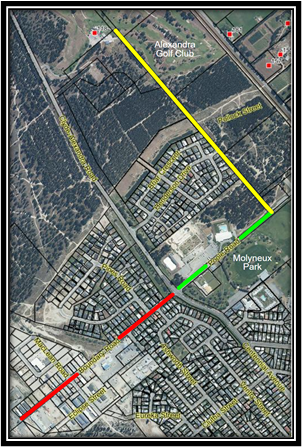

An overview of Boundary

Road, Poole Road, and the unnamed unformed section of the road, post the

renaming, is shown below in figure 2.

Figure 1 – Boundary

Road prior to the renaming.

Figure 2 – The three roads post renaming.

Poole Road and the unnamed

unformed the road are shown on District Plan Maps 1, 2, and 42. The underlying

zoning is residential. An extract from the District Plan showing Poole Road and

the unnamed unformed section of legal road is shown below in figure 3.

The first 200 metres (southern

end) of the unnamed unformed legal road is tagged ‘D10’ –

“Road to be Stopped & Recreation Purposes”. D10 is magnified in

figure 4.

Figure 3 – Extract of

District Plan.

Figure

4 – Designation 10.

Poole Road and part of the

unnamed unformed road (the Road) are also both shown in the Molyneux Park

Reserve Management Plan 2021 (the Management Plan).

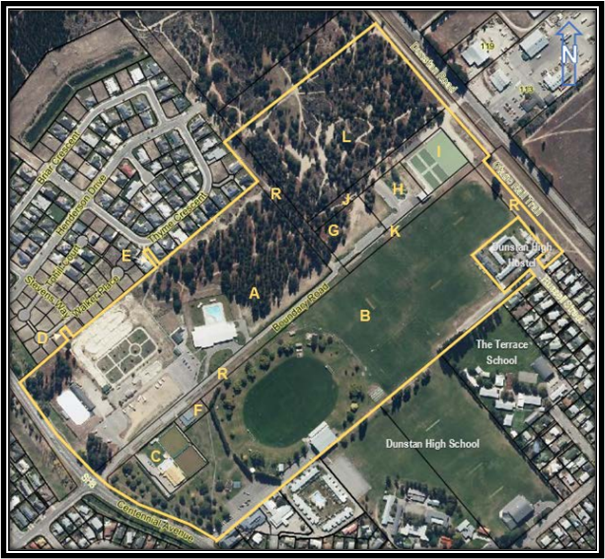

Noting that the Management

Plan was adopted prior to the renaming exercise, Boundary Road (labelled

‘R’ below in figure 5) is described as being:

The main entry to Molyneux Park is from the intersection of

Boundary Road with State Highway 8 (Centennial Avenue and Clyde-Alexandra

Road). A driveway within the road reserve of Boundary Road East is located

centrally within the park and provides access to most activities and car park

areas.

Figure 5 – Overview

of Molyneux Park (noting the Road labelled ‘R’ is now Poole Road).

The Management Plan also details

a proposal to develop new sports fields in an area to west of the Netball

courts. While the new sports fields will form part of Molyneux Park once they

are constructed. the land will remain relatively undeveloped until such time as

they are needed. A plan of the proposed sports fields as extracted from the

Management Plan is shown below in figure 6.

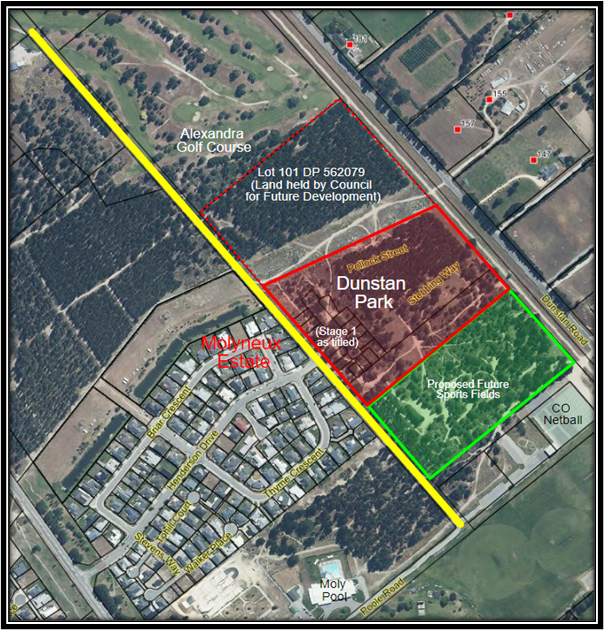

Figure 6 – Proposed

Sports Field Development Adjacent to the Existing Netball Pavilion & Courts.

Council is in the process

of subdividing the land to the north of the proposed sports fields. The

subdivision is a staged development which is known as Dunstan Park. Stage one

titles have since been released with stage two titles scheduled for release in

April. An overview of development which shows the released titles is shown in

figure 7.

Figure 7 – Overview

of Dunstan Park Subdivision (to the north of the Proposed Sports Fields).

In conjunction with the

Dunstan Park subdivision, it is proposed that the majority of the unnamed

unformed section of the road (the Road) be developed into a greenway.

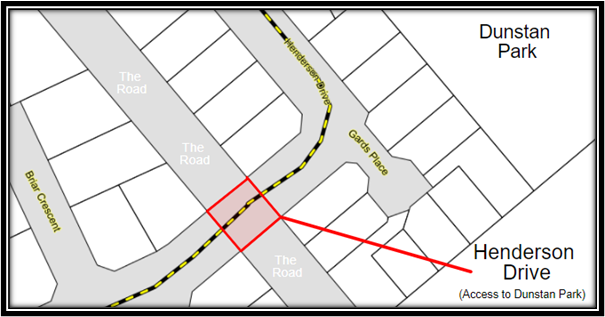

This does not include the

square of the Road which adjoins Henderson Drive. As shown in figure 8 below,

this square of the Road has been formed as part of Henderson Drive. It provides

access to Stage 1 of the Dunstan Park subdivision.

Figure 8 – Henderson

Drive Extension (Portion of the Road which will not be stopped shaded in red).

Also identified in figure

7 is Lot 101 Deposited Plan (DP) 562079 (Lot 101). Council holds Lot 101 for

future development. While plans for Lot 101 are still being finalised, the

development is expected to include a new road connecting Dunstan Road to the

Clyde – Alexandra Road, additional residential sections, and a greenway

styled buffer zone on the southern end of Lot 24 DP 3194.

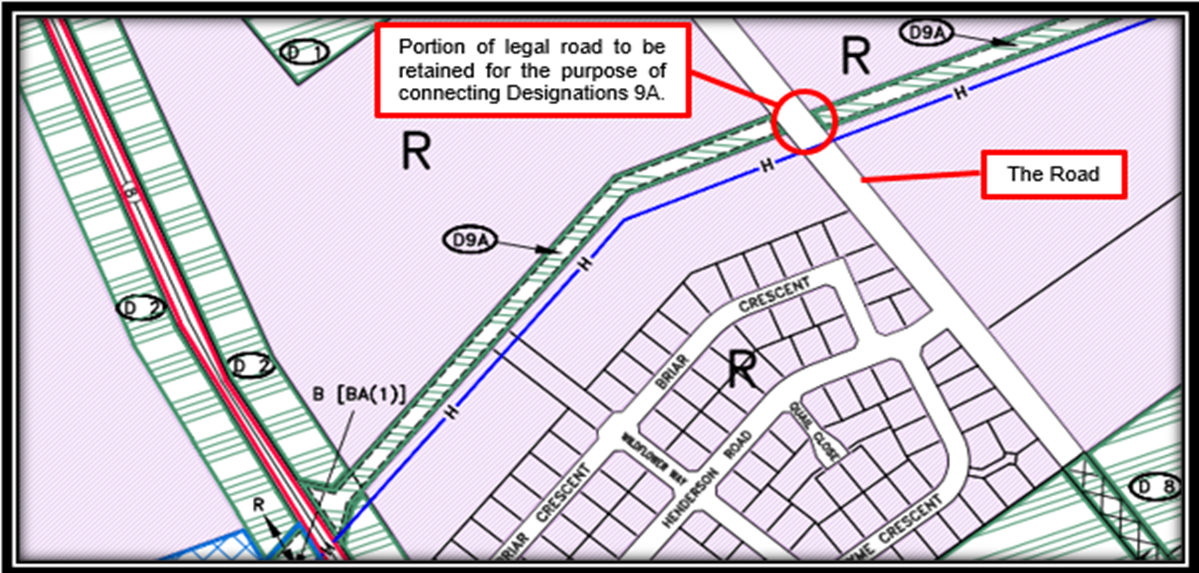

The new road is identified

on District Plan map 1 as designations 9A, and on District Plan map 42 as

designation 9B. Designations 9A are shown below in figure 9.

Should the new road be

formed at some point in the future, the area of land required to link the two

designation 9As will be taken at that time.

Figure

9 – Extract of District Plan Map 1 showing the two Designations 9A.

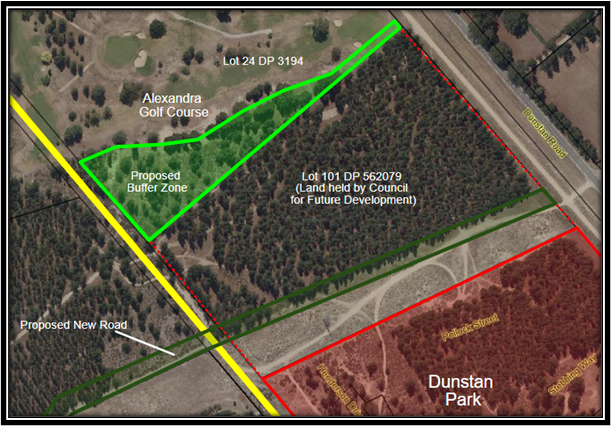

While Lot 101 is held for

future development, it is expected to be as residential sections. To provide

separation between those sections and the Alexandra Golf Course, a greenway

styled buffer zone is planned for the southern end of Lot 24. An example of the

proposed buffer zone is shown in green below in figure 10.

Figure 10 – Example

of proposed Greenway Styled Buffer Zone

The proposed greenway

styled buffer zone will provide recreational benefits and will increase

connectivity between the residential subdivisions and Molyneux Park, the Rail

Trail, and the Alexandra Golf Club.

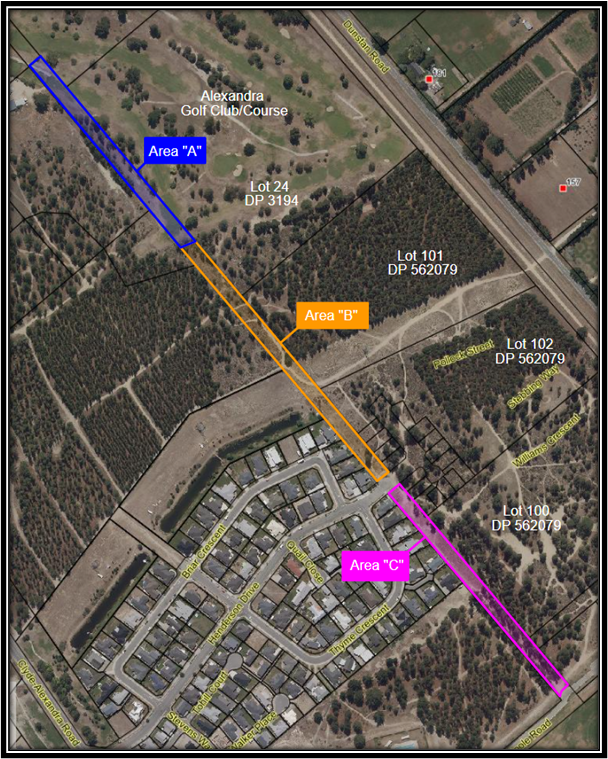

An overview of the

stopping, which is proposed to be affected in three sections, is shown below in

figure 11.

Figure 11 – Overview

of Proposed Stopping.

The area marked

“A” is occupied by the Alexandra Golf Club. It is proposed that

area “A” be stopped and amalgamated with Lot 24 DP 3194 (Lot 24) as

recreation reserve. This will allow the area marked “A” to be

included in the lease held by the Alexandra Golf Club.

It is proposed that the

areas marked “B” and “C” be stopped, freeholded, then

vested in Council as recreation reserve. This will allow areas “B”

and “C” to be developed into greenway which will secure and improve

ongoing public access.

3. Discussion

Evaluation of Application

An evaluation of the proposal to stop the Road is shown in

the table below.

|

Item

|

Criteria to be considered

|

Evaluation

|

|

District Plan

|

Has the road been identified in the

District Plan for any specific use or as a future road corridor?

|

The Road is shown on District Plan

Maps 1, 2, and 42.

The first 200 metres (southern end) of

the unnamed unformed legal road is tagged ‘D10’ –

“Road to be Stopped & Recreation Purposes”.

As shown in figure 8, the span of the

Road that intersects Henderson Drive has been formed and provides access to

the Dunstan Park residential subdivision. This span of the Road will not be

stopped.

The balance of the Road not

identified for any specific purpose or as a future road corridor.

|

|

Current Level

of Use

|

Is the road used by members of the

public for any reasons?

|

The Road is currently used by members

of the public for recreational purposes. This use will be supported by

changing the road to a reserve and greenway.

|

|

Does it provide the only or most

convenient means of access to any existing lots?

|

No. New roads have been formed or are

to be constructed for the purpose of accessing Dunstan Park.

The lots in Molyneux Estate are

accessed via existing roads.

The Central Otago Netball facility, the

existing sports field and the proposed sports fields are all access via Poole

Road.

Footpaths and cycleways can be

constructed within the greenway.

|

|

Will stopping the road adversely

affect the viability of any commercial activity or operation?

|

No commercial activity is located on

land adjacent to, or accessed from, the Road.

|

|

Will any land become landlocked if the

road is stopped?

|

No.

|

|

Future Use

|

Will the road be needed to service

future residential, commercial, industrial, or agricultural developments?

|

As above, Dunstan Park will be

accessed via newly constructed roads as a requirement of the resource

consent.

|

|

Will the road be needed in the future

to connect existing roads?

|

Yes. The part of Road which crosses

Henderson Drive will not be stopped.

This part of the Road will be formed

to provide access to Dunstan Park from Molyneux Estate.

|

|

Non-traffic

Uses

|

Does the road have current or

potential value for amenity functions, e.g., walkway, cycleway, recreational

access, access to conservation or heritage areas, park land?

|

The purpose of the proposed stopping

is to enable the road to be developed as a greenway.

Developing the Road as a greenway will

improve its amenity value by creating and securing recreational access.

|

|

Does the road have potential to be

utilised by the Council for any other public work either now or potentially

in the future?

|

As the surrounding area is developed,

additional services may need to be installed in the greenway/road corridor.

Should that be necessary, the services

could be protected by the granting and registration of easements on the

relevant record(s) of title.

|

|

Does the road have significant

landscape amenity value?

|

The Road does not have any significant

landscape amenity value.

|

|

Access to

Waterbody

|

Does the road provide access to a

river, stream, lake or other waterbody?

|

The Road does not provide access to

any waterbody.

|

|

If so, there is a need to consider

Section 345 of the Local Government Act, which requires that after stopping

the land be vested in Council as an esplanade reserve

|

N/A (refer above).

|

|

Infrastructure

|

Does the road currently contain any

services or other infrastructure, such as electricity, telecommunications,

irrigation, or other private infrastructure?

|

Yes. Both Transpower New Zealand

Limited and Aurora Energy Limited have an assortment of infrastructure

running through and over the Road.

|

|

Can the existing services or

infrastructure be protected by easements?

|

Yes. Easements will be created to

protect the infrastructure belonging to Aurora Energy. The Transpower network

is protected by virtue of the Electricity Act 1992.

|

|

Traffic Safety

|

Does the use of motor vehicles on the

road constitute a danger or hazard?

|

Yes. There are a myriad of informal

tracks through the area including on and over the Road.

Walkers and cyclists use the road for

recreational purposes which means using motor vehicles on the Road could

constitute danger or hazard to the public.

|

4. Financial

Considerations

As shown in the evaluation

table, the southern end of the Road is identified as “Road to be Stopped

& Recreation Purposes”. The balance of the Road, with the exception

of the intersections of Henderson Drive and the ‘new road’

identified in figure 9, is not required for any other roading purpose.

The Road does contain

infrastructure belonging to Transpower New Zealand Limited (Transpower) and to Aurora

Energy Limited (Aurora). Protection for this infrastructure is discussed next.

Easements

Transpower have a 220kV

overhead network which runs up the northern side of Molyneux Estate and Dunstan

Park. Their network does cross the Road, but no easement is required to protect

this infrastructure. The Transpower network is protected by virtue of the

Electricity Act 1992.

Aurora have a high voltage

underground cable and two fuse switches in the Road. The high voltage cable

runs almost the length of the Road. The cable is dashed red below in figure 13.

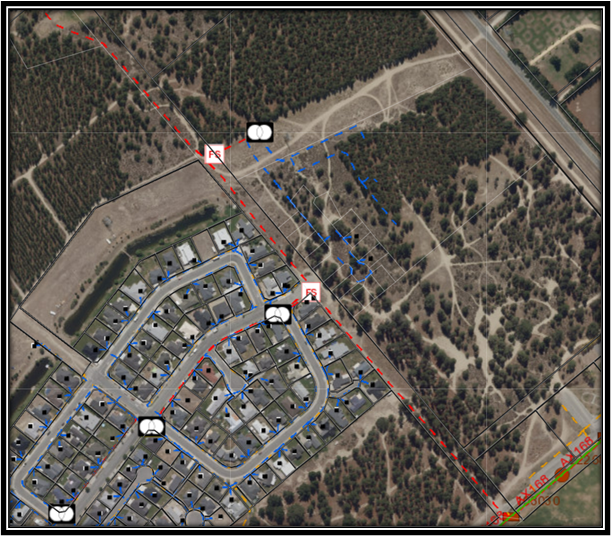

The two fuse switches are marked ‘FS’.

Figure 13 –

Aurora’s High Voltage Cable and Fuse Switches.

If the application to stop

the Road is successful Aurora will require an easement (in gross) to protect

their infrastructure. An easement will provide Aurora with right to access the

land for the purpose of managing and maintaining their network.

Legislation and Policy

Council’s Roading

Policy determines the appropriate statutory procedure for stopping a legal road

or any part thereof. The policy for selecting the correct statutory process is

as follows:

The Local Government Act

1974 road stopping procedure shall be adopted if one or more of the following

circumstances shall apply:

a) Where

the full width of road is proposed to be stopped and public access will be

removed as a result of the road being stopped; or

b) The

road stopping could injuriously affect or have a negative or adverse impact on

any other property; or

c) The

road stopping has, in the judgment of the Council, the potential to be

controversial; or

d) If

there is any doubt or uncertainty as to which procedure should be used to stop

the road.

The Local Government Act

process requires public notification of the proposal. This involves erecting signs at each end of the road to be stopped,

sending letters to adjoining owners/occupiers and at least two public notices a

week apart in the local newspaper. Members of the public have 40 days in

which to object.

The Public Works Act 1981 road stopping

procedure may be adopted when the following

circumstances apply:

e) Where

the proposal is that a part of the road width be stopped and a width of road

which provides public access will remain.

f) Where

no other person, including the public generally, are considered by the Council

in its judgment to be adversely affected by the proposed road stopping;

g) Where other reasonable

access will be provided to replace the access previously provided by the

stopped road (i.e. by the construction of a new road).

As the full width of the

road is to be stopped and public access removed, it is proposed that Local

Government Act 1974 procedure be adopted for this application.

An application to stop a

road under the Local Government Act 1974 requires public consultation with the

members of the public having a right to object to proposal.

Council’s Roading

Policy states that:

If an objection is received then the applicant will be

provided with the opportunity to consider the objection and decide if they wish

to continue to meet the costs for the objection to be considered by the Council

and the Environment Court.

If an objection is received and it is accepted by the Council

then the process will be halted and the Council may not stop the road.

If the objection is not accepted by the Council then the road

stopping proposal must be referred to the Environment Court for a decision. The

applicant is responsible for meeting all costs associated with defending the

Council’s decision in the Environment Court.

Community Board Recommendation

A report on this matter was presented to the Vincent Community

Board (the Board) for consideration at their meeting of 22 March 2022.

On consideration the Board

resolved (Resolution 22.2.6) to recommend to Council that they approve the

proposal to stop the unnamed unformed

road off the northern end of Poole Road.

5. Options

Option 1 –

(Recommended)

To approve the proposal to stop the unnamed

unformed road off the northern end of Poole Road, subject to:

- The provisions

of the Local Government Act 1974.

- The public

notification process outlined in the same Act.

- No objections

being received within the public notification period.

- The Road being

surveyed into three parcels as shown in figure 11 (overview of proposed

stopping).

- The area marked

“A” in figure 11, being stopped, classified as recreation reserve,

then amalgamated with Lot 24 DP 3194 in accordance with the provisions of the

Reserves Act 1977.

- The areas

marked “B” and “C” in figure 11, being stopped,

classified as recreation reserve, then vested in the Central Otago District

Council in accordance with the provisions of the Reserves Act 1977.

- An easement (in

gross) in favour of (and as approved by) Aurora Energy Limited being registered

over the areas marked “A”, “B”, and “C”, as

shown in figure 11 to protect the infrastructure identified in figure 13.

- The costs

outlined in table 1 being paid from the Dunstan Park Development

account.

Advantages:

· Public

thoroughfare is maintained via the newly formed Henderson Drive extension.

· Provision

has been made for the protection of the existing utility networks.

· The

land will be classified and developed as recreation reserve.

· Recreational

connectivity will be enhanced.

· The

area marked “A” will be able to be added to the lease held by the

Alexandra Golf Club.

· The

income received from previously completed stoppings will fund the stopping.

·

Recognises the provisions of the:

- Local

Government Act 1974,

- Reserves

Act 1977,

- Electricity

Act 1992,

- Council’s

Operative District Plan; and,

- Council’s

Roading Policy Bylaw.

Disadvantages:

· The

balance of the Dunstan Park Development account will be reduced.

Option 2

To not recommend to Council to approve the proposal to stop

the unnamed unformed road off the northern end of Poole Road.

Advantages:

· The

balance of the Dunstan Park Development account will not be reduced.

Disadvantages:

· The

land will not be classified as it is to be developed and used/occupied.

· The

area marked “A” will not be able to be added to the lease held by

the Alexandra Golf Club.

· Does

not recognise the purpose for which income received from previously completed

stoppings is held.

· Does

not recognise the provisions and /or intentions of the:

- Local

Government Act 1974,

- Reserves

Act 1977,

- Electricity

Act 1992,

- Council’s

Operative District Plan; and,

- Council’s

Roading Policy Bylaw.

6. Compliance

|

Local Government Act 2002 Purpose Provisions

|

This

decision promotes the economic wellbeing of the community by enabling land

that was held (but not required) for roading purposes to be repurposed as

greenway which will increase the land’s amenity values and enhance recreational

connectivity.

|

|

Decision consistent with other Council plans and policies? Such as

the District Plan, Economic Development Strategy etc.

|

Council’s

Road Stopping Policy applies to this application.

Consideration

of this policy has ensured that the appropriate statutory process, being to

stop the road in accordance with the provisions of the Local Government Act

1974, has been adopted.

The

recommendation also acknowledges the designations outlined in Council’s

Operational District Plan.

|

|

Considerations as to sustainability, the environment and climate

change impacts

|

Stopping

the road, vesting it as recreation reserve, then developing it as a greenway

enhances the environmental and amenity value of the land.

|

|

Risks Analysis

|

The

proposal to stop the road will be subject to public consultation prior to a

final decision being made.

Consulting

with the public manages the risk associated with public accessibility

perceptions.

|

|

Significance, Consultation and Engagement (internal and external)

|

The

Significance and Engagement Policy has been considered, with none of the

criteria being met or exceeded.

Public

notices and advertising in accordance with the provisions of the Local

Government Act 1974 will be posted.

Notice

of the completed road stopping will be published in the New Zealand Gazette.

|

7. Next Steps

The

following steps have been/will be taken to implement the stopping:

1. Community

Board approval March

2022

2. Council

approval April

2022

3. Survey June

2022

4. Survey

Plan approved June/July

2022

5. Public

Notification commences Mid

to late 2022

6. Public

Notification Period ends Mid

to late 2022

7. Gazette

notice published Late

2022

8. Attachments

Nil

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Linda

Stronach

|

Quinton

Penniall

|

|

Team

Leader - Statutory Property

|

Acting Executive

Manager – Infrastructure Services

|

|

24/03/2022

|

5/04/2022

|

22.3.4 Request

for Minister of Conservation's Consent to the Granting of an Easement over

Local Purpose Reserve [PRO: 65-7027-E1]

Doc ID: 571955

1. Purpose of Report

To consider granting the consent of the Minister of

Conservation (under delegated authority) to the granting of an easement (in

gross) to Aurora Energy over Part Section 142 Block I Teviot Survey District

being the Roxburgh Local Purpose (Public Utility) Reserve.

|

Recommendations

That the Council

A. Receives the

report and accepts the level of significance.

B. Agrees grant the consent of the Minister of

Conservation (under delegated authority) to the granting of an easement (in

gross) over Part Section 142 Block I Teviot Survey District to Aurora Energy

Limited.

|

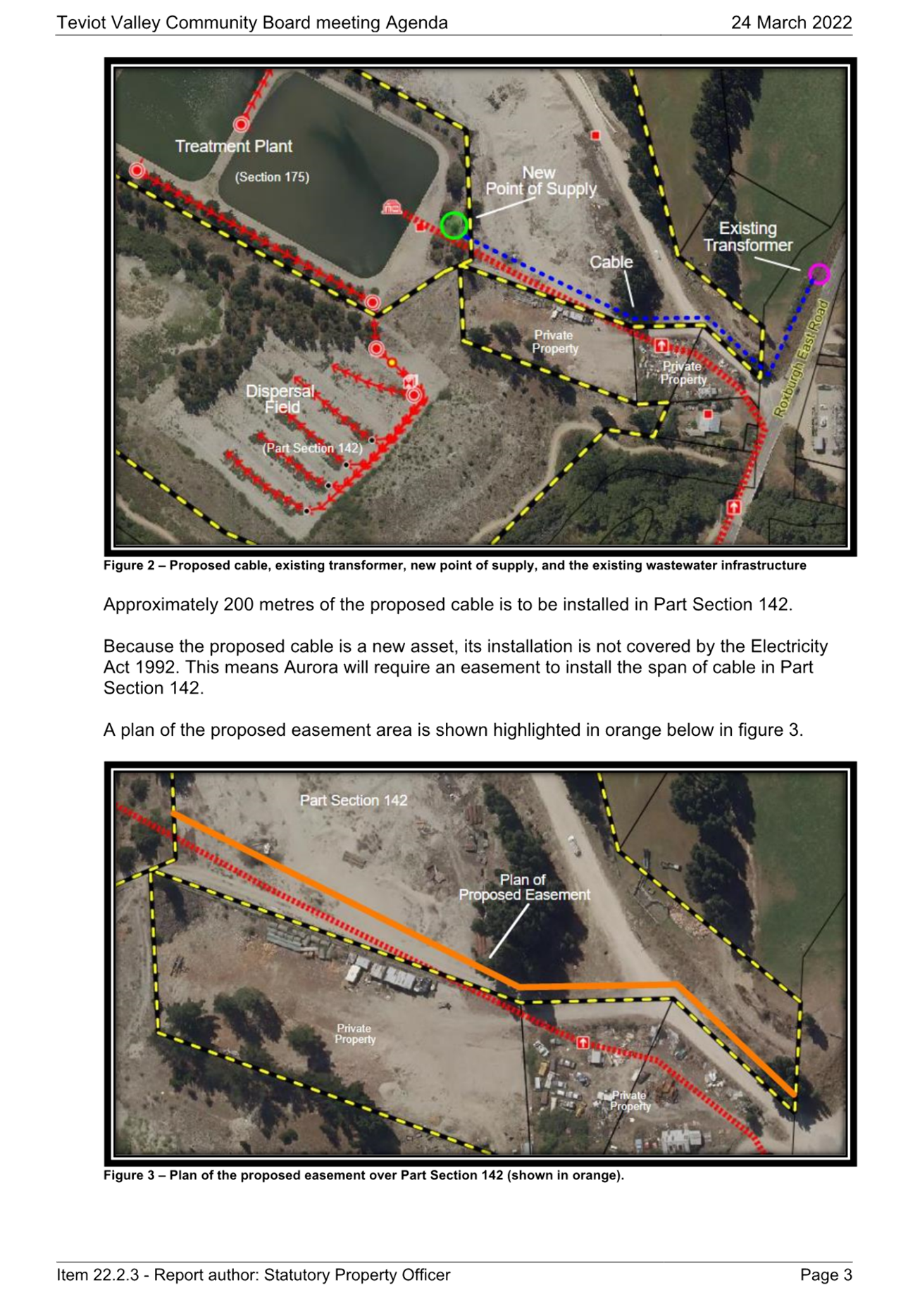

2. Background

Resolution 22.2.3

At its meeting of 24 March 2022, the Teviot Valley Community

Board (the Board) considered an application for an easement over Part Section

142 Block I Teviot Survey District being Local Purpose (Public Utility)

Reserve.

A copy of the report to the Board dated 24 March 2022 is

attached as Appendix 1.

On consideration, the Board resolved (Resolution 22.2.3) as

follows:

B. Agrees

to grant an easement (in gross) to Aurora Energy Limited containing the right to

convey electricity over Part Section 142 Block I Teviot Survey District for $1,

subject to:

- Aurora Energy Limited

(or their agents) obtaining all consents, permits, and other rights associated

with installing the cable between the existing transformer and the new Point of

Supply.

- The final easement plan

being approved by the Chief Executive Officer.

- The Minister of

Conservation’s consent.

C. Authorises

the Chief Executive to do all that is necessary to give effect to the

resolution

As noted in Resolution

22.2.3, the granting of the easement over Part Section 142 Block I Teviot Survey

District is subject to the consent of the Minister of Conservation.

The role of the Minister

of Conservation in this matter is to:

· be

satisfied that the granting of the easement conforms with the provisions of the

Reserves Act 1977.

· ensure

that due process under the Act has been followed.

· consider

submissions resulting from public notification (when required if applicable).

3. Discussion

Due Process –

Easements over Reserve Land

Section 48(1)(d) of the

Reserves Act 1977 (the Act) authorises the granting easements over a reserve or

any part thereof for an electrical installation or work as defined in section 2

of the Electricity Act 1992.

Section 2 of the

Electricity Act 1992 defines an electrical installation or work as “all

fittings beyond the point of supply that form part of a system that is used to

convey electricity to a point of consumption”. Accordingly, the granting

of an easement for the purpose of extending the existing network to service to

the oxidation ponds on Section 175 Block I Teviot Survey District, is

consistent with the Act.

Part Section 142 Block I

Teviot Survey District is a Local Purpose (Public Utility) Reserve. It is held

by Council (as the administering Body) subject to the Reserves Act 1977.

While public notice can be

required when easements or other rights are granted over reserves, section

48(3) of the Act states that public notification is not required where the

reserve is vested in an administering body and is not likely to be materially

altered or permanently damaged; and the rights of the public in respect of the

reserve are not likely to be permanently affected.

An underground cable will

not materially alter the reserve or affect the rights of the public. Therefore,

public consultation is not required in this instance.

Minister of

Conservation’s Consent

Under the Reserves Act

1977, the Minister of Conservation’s consent is required by the

administering body when granting an easement over recreation reserve. The

purpose of the Minister’s consent is to ensure due process under the Act

has been followed by the administering body.

Pursuant to section 10 of

the Act, and in accordance with the “Instrument of Delegation to

Territorial Authorities” dated 12 June 2013, the Minister of Conservation

has delegated the granting of that consent to the Council.

4. Financial

Considerations

There are no financial considerations

or implications related to the recommendation.

5. Options

Option 1 –

(Recommended)

To grant the consent of

the Minister of Conservation (under delegated authority) to the granting of an

easement (in gross) over Part Section 142 Block I Teviot Survey District to Aurora

Energy Limited.

Advantages:

· The

granting of the easement will not materially alter the reserve or compromise

the use of the land.

· Recognises

that the purpose of the easement is consistent with the Reserves Act 1977.

· Recognises

the provisions of the Instrument of Delegation dated 12 June 2013.

· Recognises

that due process has been followed.

Disadvantages:

· None.

Option 2

To not grant the consent

of the Minister of Conservation (under delegated authority) to the granting of

an easement (in gross) over Part Section 142 Block I Teviot Survey District to

Aurora Energy Limited.

Advantages:

· None.

Disadvantages:

· Does

not recognise that the purpose of the easement is consistent with the Reserves

Act 1977.

· Does

not recognise the provisions of the Instrument of Delegation dated 12 June

2013.

· Does

not recognise that due process has been followed.

6. Compliance

|

Local Government Act 2002 Purpose Provisions

|

The

Local Government Act 2002 does not apply to this decision.

The

Minister of Conservation’s consent is delegated to Council in

accordance with the Reserves Act 1977, and the “Instrument of

Delegation to Territorial Authorities” dated 12 June 2013.

|

|

Decision consistent with other Council plans and policies? Such as

the District Plan, Economic Development Strategy etc.

|

There

are no financial implications related to the recommendation.

|

|

Considerations as to sustainability, the environment and climate

change impacts

|

The

recommendation is consistent with the Reserves Act 1977 and with the

“Instrument of Delegation to Territorial Authorities” dated 12

June 2013.

|

|

Risks Analysis

|

There

are no risks to Council associated with the recommended option.

|

|

Significance, Consultation and Engagement (internal and external)

|

The

Significance and Engagement Policy has been considered, with none of the

criteria being met or exceeded.

Pursuant

to section 48(3) of the Reserves Act 1977, public advertising of the

intention to grant of an easement over a reserve or any part thereof is not

required where the reserve is not likely to be materially altered or

permanently damaged; and the rights of the public in respect of the reserve

are not likely to be permanently affected.

|

7. Next Steps

The following steps

have/will be undertaken in association with having the easement registered:

1. Community Board Approval 24

March 2022

2. Consent of the Minister of Conservation 20

April 2022

3. Applicant

advised of outcome Late

April 2022

8. Attachments

Appendix 1 - Copy of the report to

the Board dated 24 March 2022 ⇩

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Linda

Stronach

|

Louise

van der Voort

|

|

Team

Leader - Statutory Property

|

Executive

Manager - Planning and Environment

|

|

25/03/2022

|

12/04/2022

|

|

Council

meeting

|

27 April

2022

|

22.3.5 Request

for Minister of Conservation's Consent to the Granting of an Easement over

Scenic Reserve [PRO: 65-3000-E1]

Doc ID: 576529

1. Purpose of Report

To consider granting the consent of the Minister of

Conservation (under delegated authority) to the granting of the right to

resurvey and increase the footprint of an existing easement (in gross) to

Aurora Energy over Lot 7 DP 433991 being part of the Sugarloaf Scenic Reserve.

|

Recommendations

That the Council

A. Receives the

report and accepts the level of significance.

B. Agrees grant the

consent of the Minister of Conservation (under delegated authority) to the granting of the right to increase the footprint

of an existing easement (in gross), to legalise the existing infrastructure,

and to provide for the installation of an additional electrical cable, over

Lot 7 DP 433991, being part of the Sugarloaf Scenic Reserve, to Aurora Energy

Limited.

|

2. Background

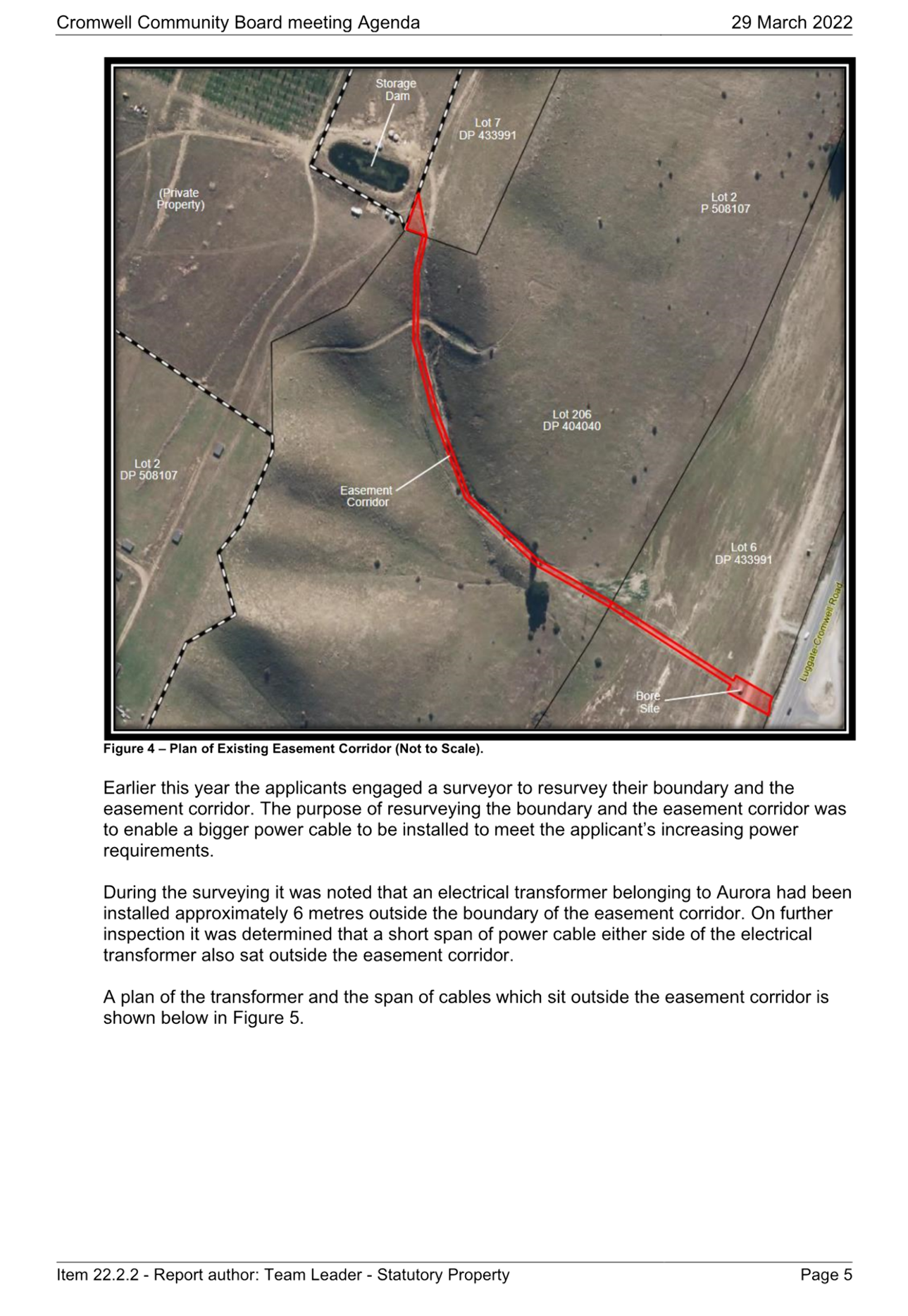

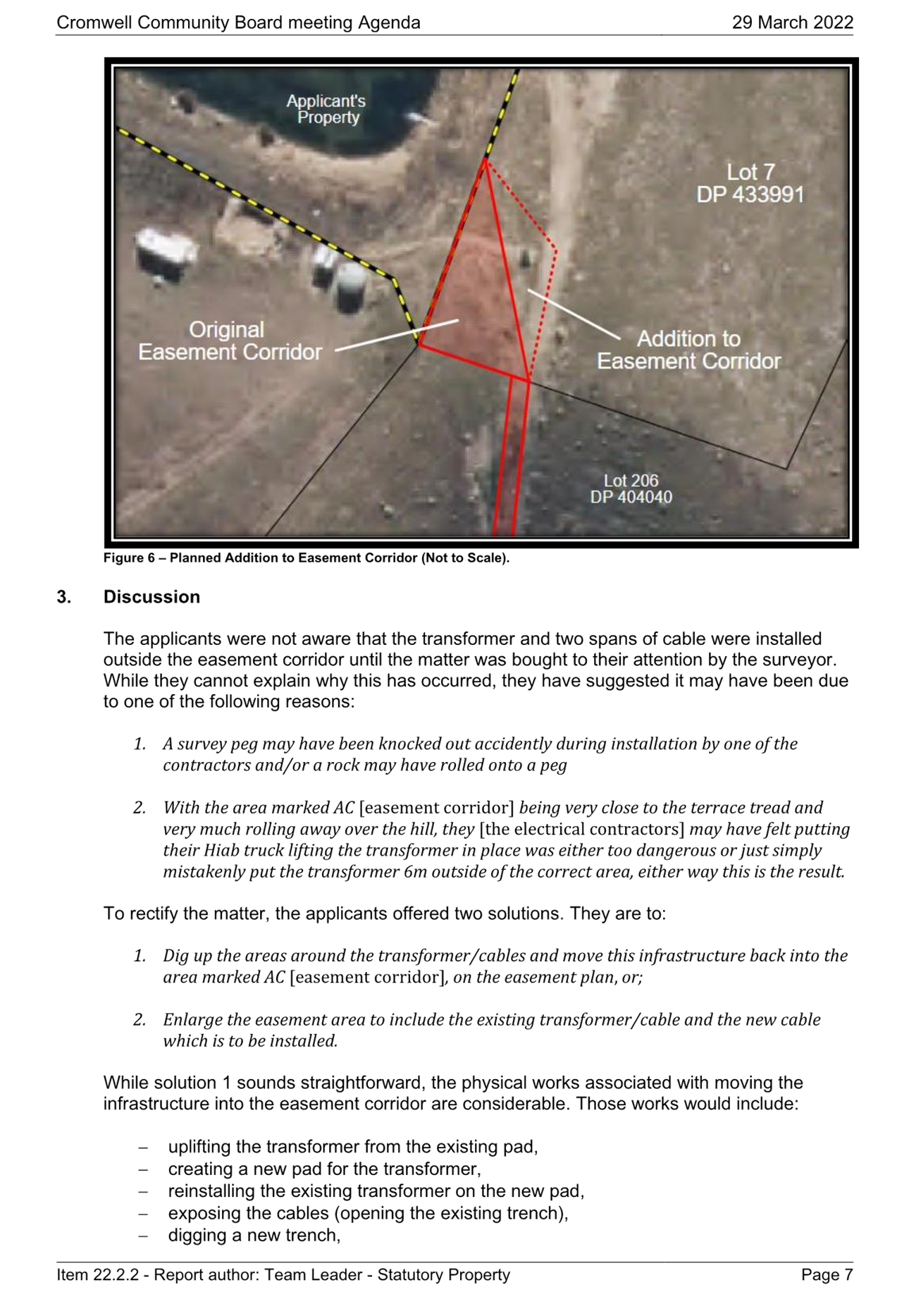

Resolution 22.2.2

At its meeting of 29 March 2022, the Cromwell Community

Board (the Board) considered an application to resurvey and increase the

footprint of an existing easement Lot 7 DP 433991 being part of the Sugarloaf

Scenic Reserve.

A copy of the report to the Board dated 29 March 2022 is

attached as Appendix 1.

On consideration, the Board resolved (Resolution 22.2.2) as

follows:

B. Agrees

the area of the easement corridor on Lot 7 DP 433991 being resurveyed and increased

in size (as shown in figure 6), to legalise the existing infrastructure and to allow

an additional power cable to be installed to meet the applicant’s

increased power requirements,

subject to:

- The applicants obtaining

all permits and consents associated with installing the additional cable.

- The applicants paying

all costs associated with surveying the infrastructure and with the preparation

and registration of the revised easement agreement.

- The Chief Executive

approving the new easement plan and agreement.

- The Chief Executive

being satisfied with any reinstatement/remediation works following any

earthworks on the Reserve.

- The consent of the

Minister of Conservation.

C. Authorises

the Chief Executive to do all that is necessary to give effect to the

resolution

As noted in Resolution

22.2.2, the granting of the extension to the footprint easement over Lot 7 DP

433991 is subject to the consent of the Minister of Conservation.

The role of the Minister

of Conservation in this matter is to:

· be

satisfied that the granting of the easement conforms with the provisions of the

Reserves Act 1977.

· ensure

that due process under the Act has been followed.

· consider

submissions resulting from public notification (when required if applicable).

3. Discussion

Due Process –

Easements over Reserve Land

Section 48(1)(d) of the

Reserves Act 1977 (the Act) authorises the granting of easements over a reserve

or any part thereof for an electrical installation or work as defined in section

2 of the Electricity Act 1992.

Section 2 of the

Electricity Act 1992 defines an electrical installation or work as “all

fittings beyond the point of supply that form part of a system that is used to

convey electricity to a point of consumption”. Accordingly, the granting

of an easement for the purpose of extending the existing network to service to

the oxidation ponds on Section 175 Block I Teviot Survey District, is

consistent with the Act.

Lot 7 DP 433991 is Scenic

Reserve. It is held by Council (as the administering Body) subject to the

Reserves Act 1977.

While public notice can be

required when easements or other rights are granted over reserves, section

48(3) of the Act states that public notification is not required where the

reserve is vested in an administering body and is not likely to be materially

altered or permanently damaged; and the rights of the public in respect of the

reserve are not likely to be permanently affected.

Increasing the footprint

of an existing easement, to legalise existing infrastructure, and to provide

for the installation of an additional electrical cable will not materially

alter the reserve or affect the rights of the public. Therefore, public

consultation is not required in this instance.

Minister of Conservation’s

Consent

Under the Reserves Act

1977, the Minister of Conservation’s consent is required by the

administering body when granting an easement over recreation reserve. The

purpose of the Minister’s consent is to ensure due process under the Act

has been followed by the administering body.

Pursuant to section 10 of

the Act, and in accordance with the “Instrument of Delegation to

Territorial Authorities” dated 12 June 2013, the Minister of Conservation

has delegated the granting of that consent to the Council.

4. Financial

Considerations

There

are no financial considerations or implications related to the recommendation.

5. Options

Option 1 –

(Recommended)

To grant the consent of

the Minister of Conservation (under delegated authority) to the granting of the

right to increase the footprint of an existing easement (in gross), to legalise

the existing infrastructure, and to provide for the installation of an

additional electrical cable, over Lot 7 DP 433991, being part of the Sugarloaf

Scenic Reserve, to Aurora Energy Limited.

Advantages:

· The

existing infrastructure will be legalised.

· The

additional cable will not materially alter the reserve or compromise the use of

the land.

· Recognises

that the purpose of the easement is consistent with the Reserves Act 1977.

· Recognises

the provisions of the Instrument of Delegation dated 12 June 2013.

· Recognises

that due process has been followed.

Disadvantages:

· None.

Option 2

To not grant the consent

of the Minister of Conservation (under delegated authority) to the granting of the

right to increase the footprint of an existing easement (in gross) over Lot 7

DP 433991, to Aurora Energy Limited.

Advantages:

· None.

Disadvantages:

· The

existing infrastructure will not be legalised.

· Does

not recognise that the purpose of the easement is consistent with the Reserves

Act 1977.

· Does

not recognise the provisions of the Instrument of Delegation dated 12 June

2013.

· Does

not recognise that due process has been followed.

6. Compliance

|

Local Government Act 2002 Purpose Provisions

|

The

Local Government Act 2002 does not apply to this decision.

The

Minister of Conservation’s consent is delegated to Council in

accordance with the Reserves Act 1977, and the “Instrument of Delegation

to Territorial Authorities” dated 12 June 2013.

|

|

Decision consistent with other Council plans and policies? Such as

the District Plan, Economic Development Strategy etc.

|

There

are no financial implications related to the recommendation.

|

|

Considerations as to sustainability, the environment and climate

change impacts

|

The

recommendation is consistent with the Reserves Act 1977 and with the

“Instrument of Delegation to Territorial Authorities” dated 12

June 2013.

|

|

Risks Analysis

|

There

are no risks to Council associated with the recommended option.

|

|

Significance, Consultation and Engagement (internal and external)

|

The

Significance and Engagement Policy has been considered, with none of the

criteria being met or exceeded.

Pursuant

to section 48(3) of the Reserves Act 1977, public advertising of the

intention to extend the footprint of an existing easement over a reserve or

any part thereof is not required where the reserve is not likely to be

materially altered or permanently damaged; and the rights of the public in

respect of the reserve are not likely to be permanently affected.

|

7. Next Steps

The following steps

have/will be undertaken in association with having the easement registered:

1. Community Board Approval 29

March 2022

2. Consent of the Minister of Conservation 27

April 2022

3. Applicant

advised of outcome May

2022

8. Attachments

Appendix 1 - Copy of Report to the

Board dated 29 March 2022 ⇩

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Linda

Stronach

|

Louise

van der Voort

|

|

Team

Leader - Statutory Property

|

Executive

Manager - Planning and Environment

|

|

1/04/2022

|

12/04/2022

|

|

Council

meeting

|

27 April

2022

|

22.3.6 Alexandra

Rugby Football Club Power Account

Doc ID: 576705

1. Purpose

of Report

To consider a request from

the Alexandra Rugby Football Club for reimbursement of a proportion of

historical electricity invoices.

|

Recommendations

That the Council

A. Receives the

report and accepts the level of significance.

B. Approves the

Alexandra Rugby Football Club’s request for compensation for historical

electricity invoices of $10,000.

C. Approves $10,000 from

the Molyneux Park charge account to action payment of recommendation B.

|

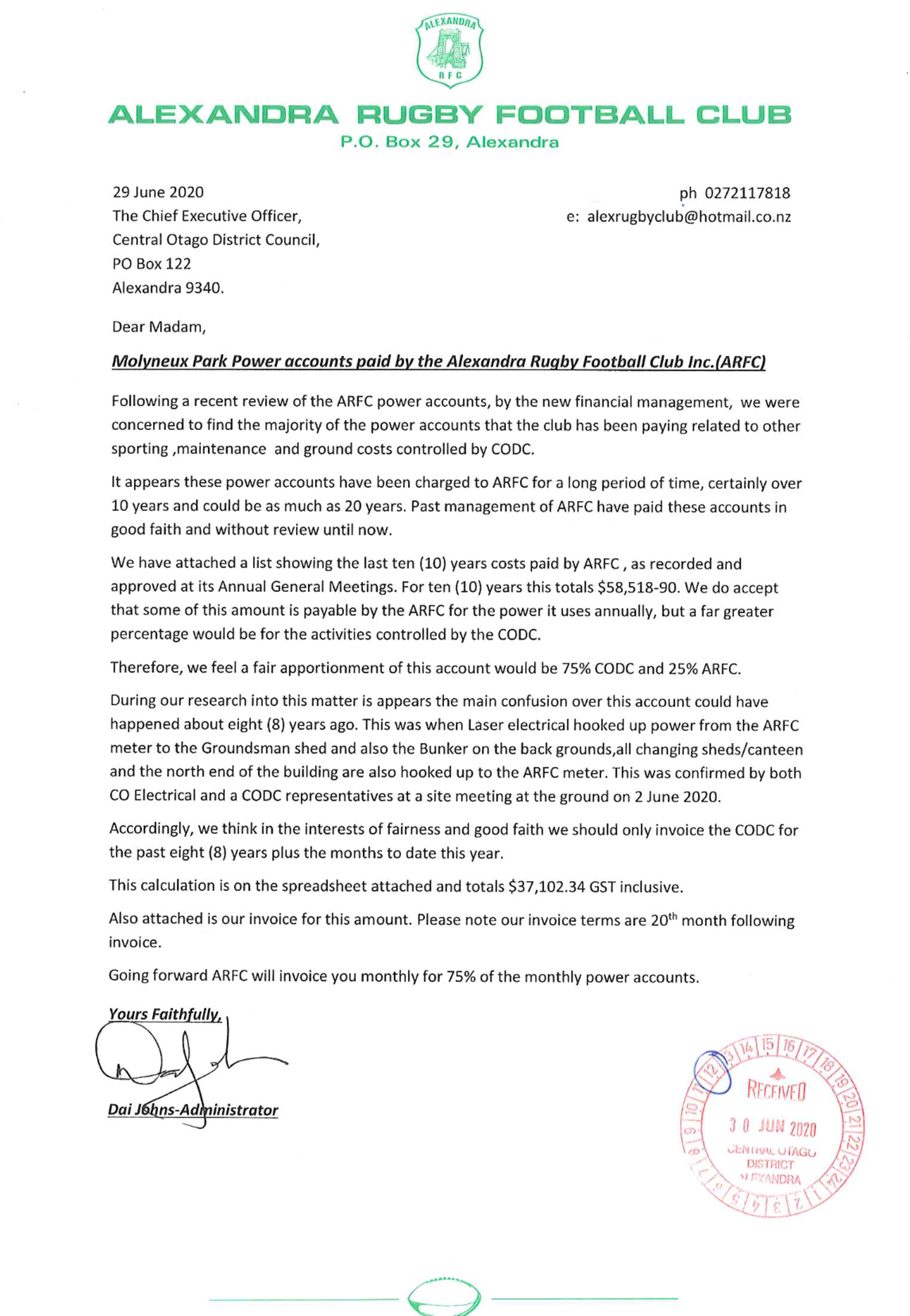

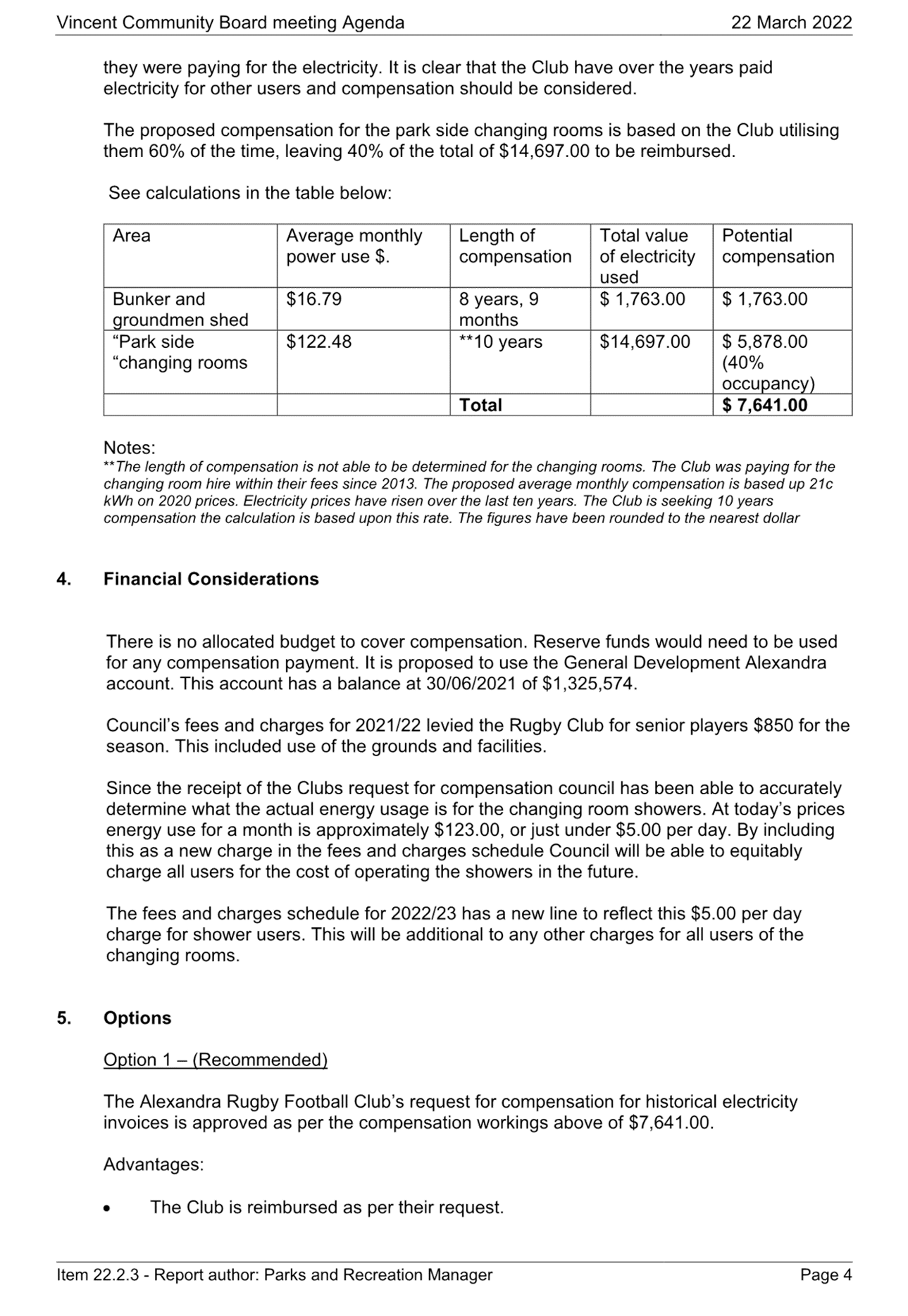

2. Background

In June 2020 Council

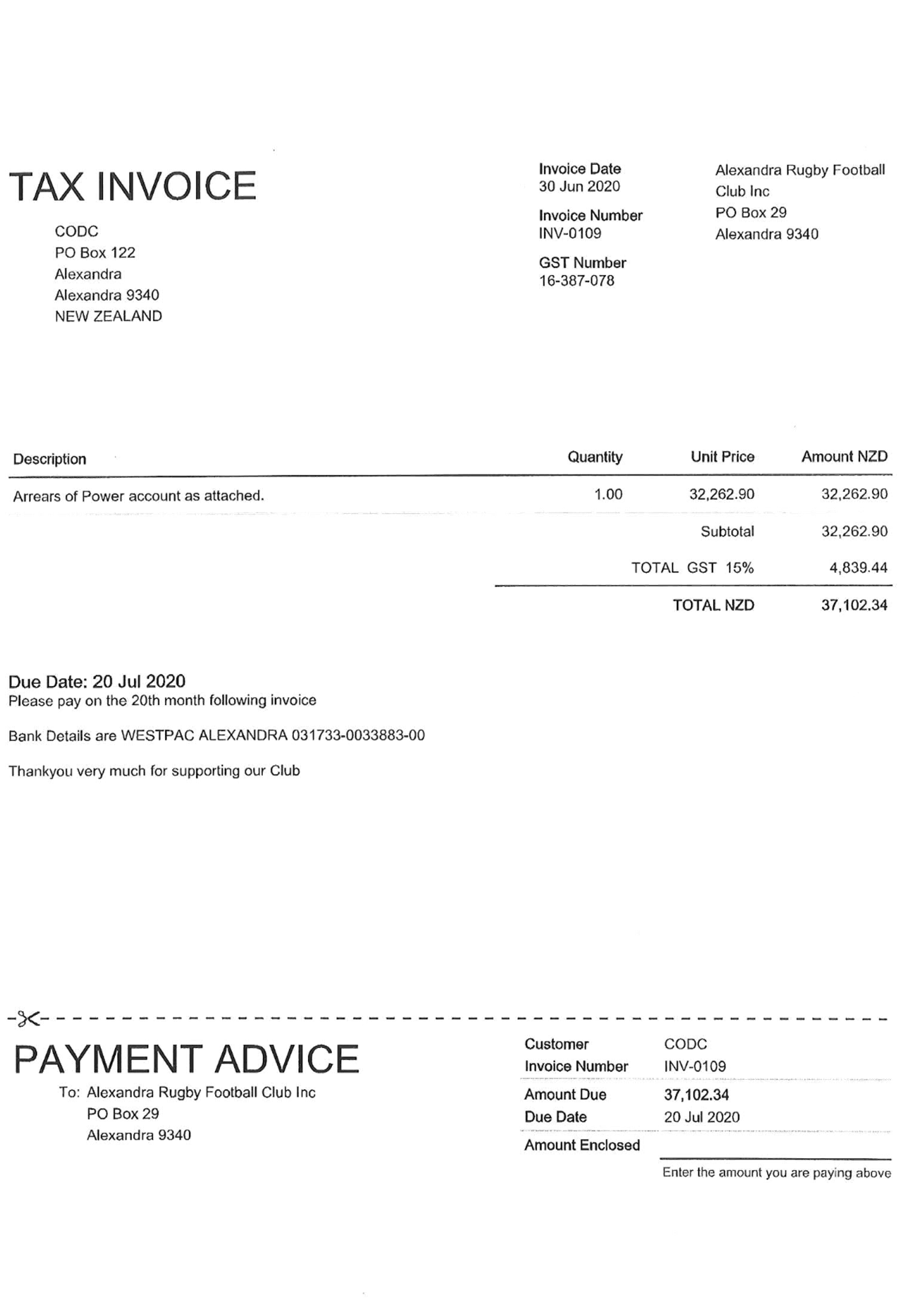

received a letter from the Alexandra Rugby Football Club (the Club) requesting

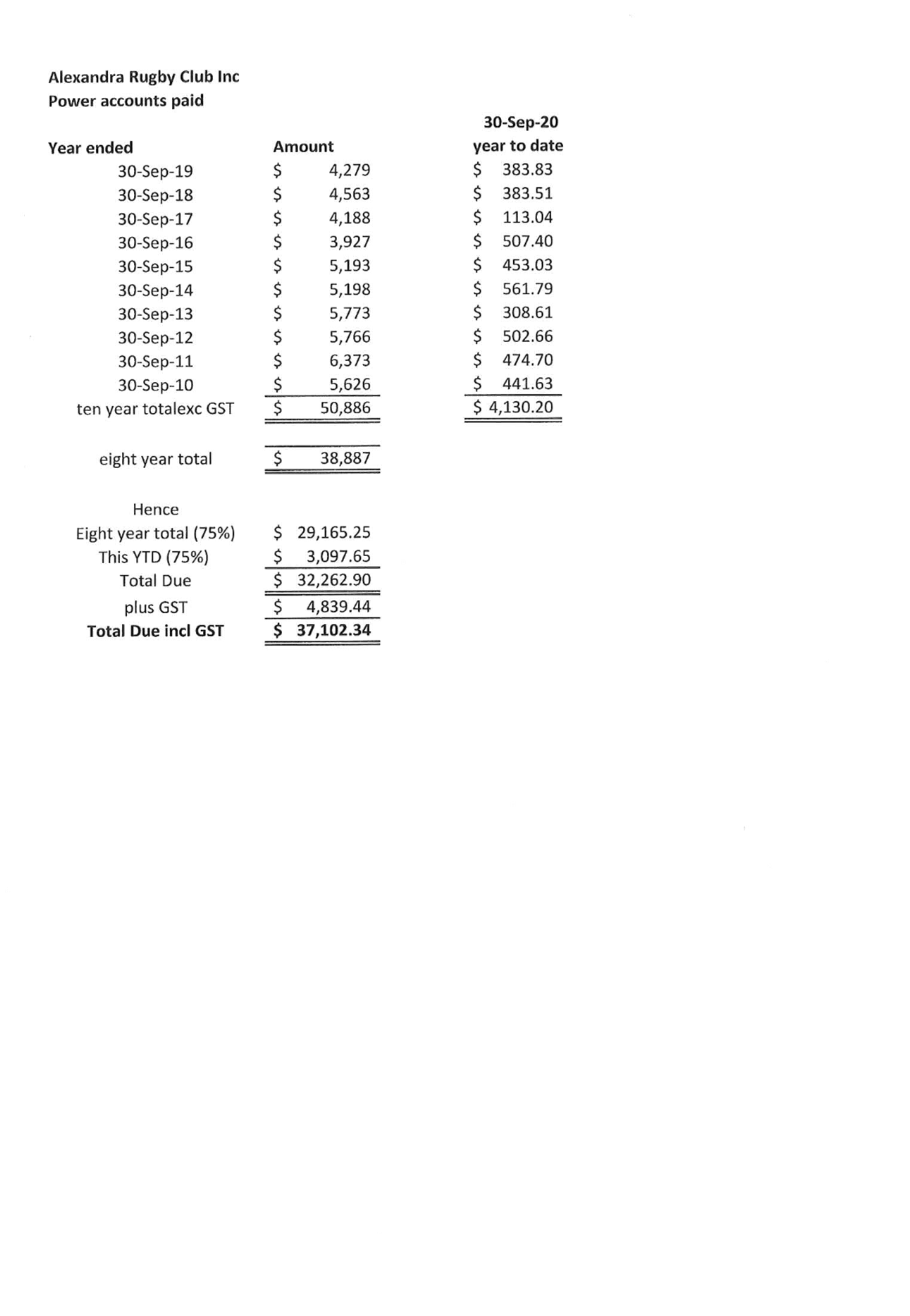

that Council reimburse the Club $37,102.34 GST inclusive. The Club states that

over the past ten years it has paid for electricity costs at Molyneux Park that

it considers should have been paid for by the Council. Appendix 1.

A report was referred to

the Vincent Community Board (the Board) at its meeting in November 2021. The

matter was left on the table and staff were requested to meet with the Club to

discuss the contents of the report and determine a way forward.

Staff and the Club held a

meeting in early January. The Club expressed a willingness to resolve this

matter and were of the view that for some years they have been paying for the

electricity use of other users of the changing room showers. The Club consider

they should receive some form of compensation for this.

The Board considered a

report, Appendix 2, at their meeting on 22 March and resolved the

following:

Moved: Garbutt

Seconded: Stirling-Lindsay

That the Vincent Community Board

A. Receives

the report and accepts the level of significance.

B. Recommends

to Council that they approve $10,000.00 from the General

Development Alexandra reserves account to action payment for

historical electricity invoices to the Alexandra Rugby Football Club as a final

settlement.

3. Discussion

There are two separate

electricity meters at Molyneux Park that the Club have paid the electricity

invoices for. The groundsman shed and bunker are on one meter and the Molyneux

Stadium’s Park side changing room showers on another.

Groundsman Shed and Bunker

The

groundsman’s shed was built by the Molyneux Park Charitable Trust in

2006. The construction of the bunker predates this by many years.

Upon investigation it was

found that the groundsmen shed, and the bunker were connected to the

Club’s account. This occurred when Council upgraded the Molyneux Park

irrigation system in late 2013. The original cable from the Stadium to the

bunker had to be reburied at that time as the previous cable had failed and was

non-compliant.

In discussions with a

former Council staff member and the electrical contractor involved in this

project, both recall a conversation with the Club seeking permission to connect

this new cable to the Club’s lighting control box. Their recollection was

that permission was granted, since very little power would be used. However,

this agreement seems not to have been documented in writing by either the

Council or the Club.

As it was not viable to

redirect the groundsmen shed and bunker onto a Council electricity meter, to

rectify the situation a “check” meter was installed in October

2020.

The “check”

meter is read every month and reimbursement for electricity used at the bunker and

groundsman shed is paid by Council to the Club. A reimbursement rate of 21

cents per kWh based on averages of previous electricity invoices was agreed to

with the Club. This now forms part of the Club’s lease agreement with

Council.

Council has on average

compensated the Club $16.79 per month for the electricity used by the bunker

and groundsman shed since October 2020 when the “check” meter was

installed.

Stadium’s

“park side” changing rooms

The changing rooms being

connected to the Club’s electricity meter is historical and likely dates

back to when the Molyneux Park Charitable Trust (the Trust) operated Molyneux

Park.

In

2006 Council entered into a management agreement with the Trust. As part of

this agreement the Trust were required to undertake a range of functions

including:

· Collecting facility hire and rental charges

· Changing room cleaning and services

· Monitor water heating and report any problems to Council

· Manage and clean four sports club changing rooms under the

rugby club

· Manage the changing rooms water heating system. (Council

acknowledges that this system is overdue for replacement, which is not expected

to be funded by the Trust)

The

Trust received an annual funding grant from Council to assist with operations.

The Trust also augmented its income from user charges.

The

final year of charging undertaken by the Trust was 2011. That year the Rugby

Club was charged the following:

- $2,100 for the season (including

changing rooms).

- Daily charge main oval (including

changing rooms) $185.00.

- Daily charge back fields

(including Changing rooms) $125.00.

Records indicate Council

took over the management of the park and changing rooms from the Trust on 1st

September 2011.

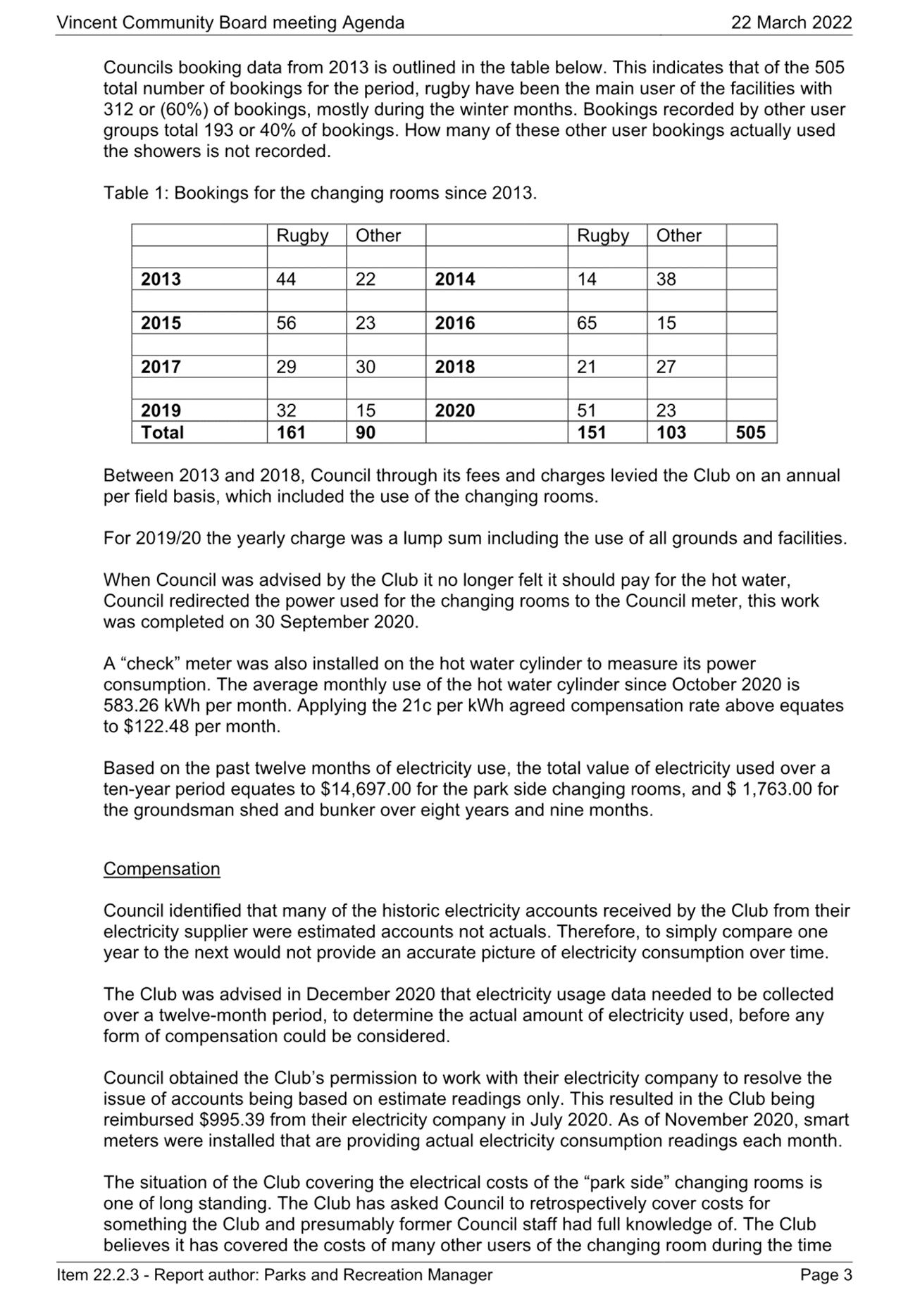

Currently the changing

rooms are used exclusively by the Club for rugby games and practice from April

to August/September each year. It is used intermittently by cricket when 20/20

and other representative matches are held during summer. There is also the

occasional casual booking that requires the use of the showers.

It should be noted that

booking data for some years has not been well recorded and that for many years

the Club would turn the power to the showers off when not required.

The Council’s

booking data from 2013 is outlined in the table below. This indicates that of

the 505 total number of bookings for the period, the rugby club has been the

main user of the facilities with 312 or (60%) of bookings, mostly during the

winter months. Bookings recorded by other user groups total 193 or 40% of

bookings. How many of these other user bookings actually used the showers is

not recorded.

Table 1: Bookings for the

changing rooms since 2013.

|

Rugby

|

Other

|

|

Rugby

|

Other

|

|

|

|

|

|

|

|

|

|

|

2013

|

44

|

22

|

2014

|

14

|

38

|

|

|

|

|

|

|

|

|

|

2015

|

56

|

23

|

2016

|

65

|

15

|

|

|

|

|

|

|

|

|

|

|

2017

|

29

|

30

|

2018

|

21

|

27

|

|

|

|

|

|

|

|

|

|

|

2019

|

32

|

15

|

2020

|

51

|

23

|

|

|

Total

|

161

|

90

|

|

151

|

103

|

505

|

Between 2013 and 2018,