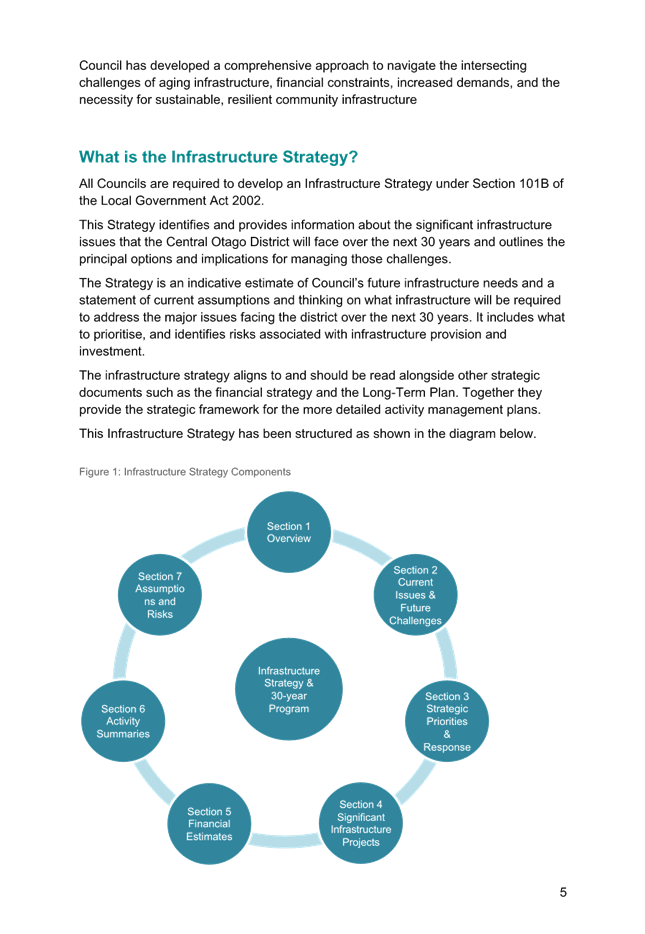

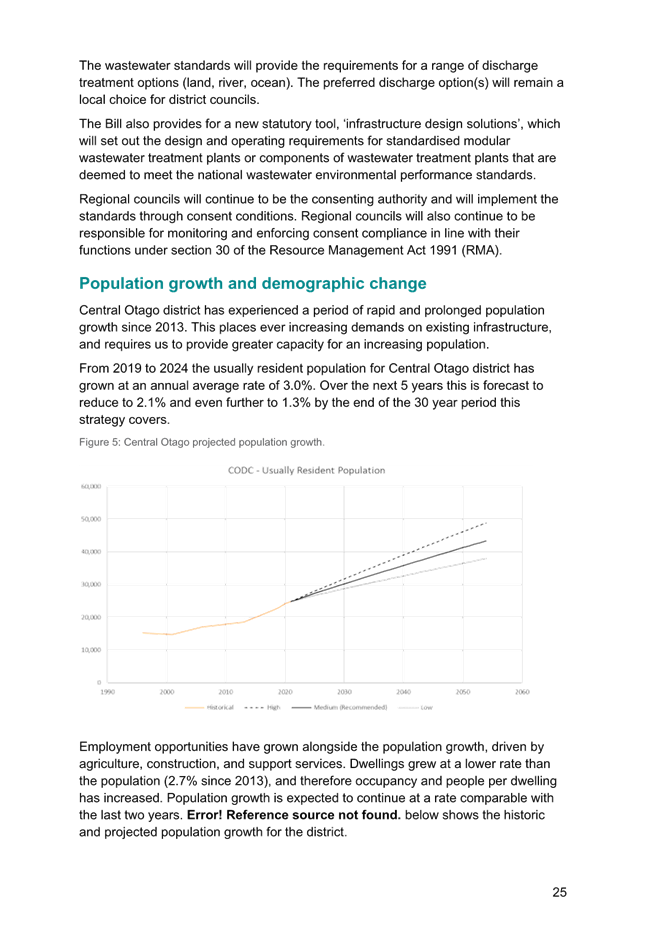

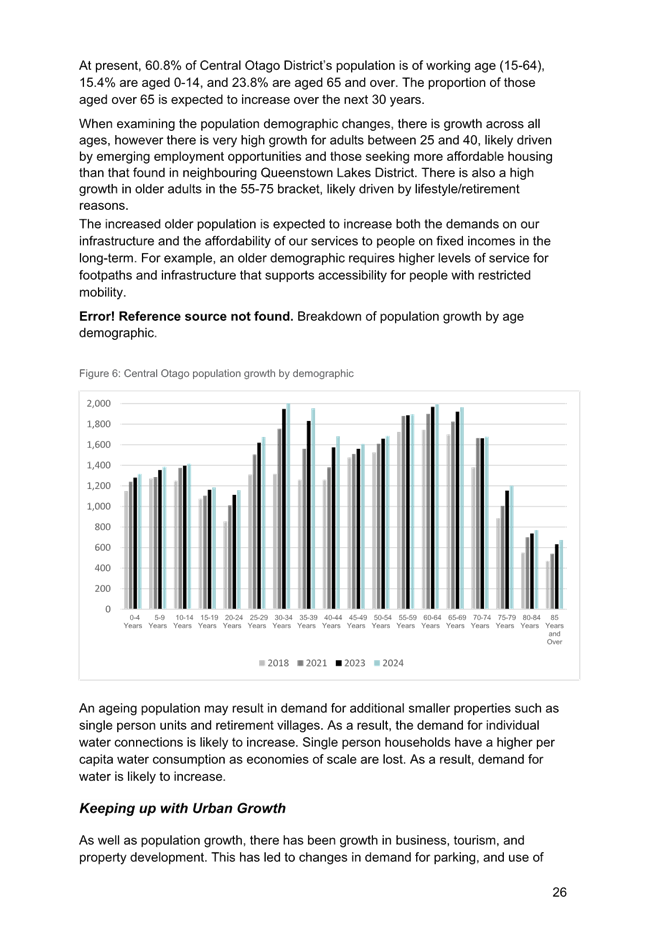

7 Reports

25.1.24 Draft

Consultation Document and Supporting Material for the 2025-34 Long-term Plan

for Audit New Zealand

Doc ID: 2015448

|

Report Author:

|

Saskia Righarts, Group Manager -

Business Support

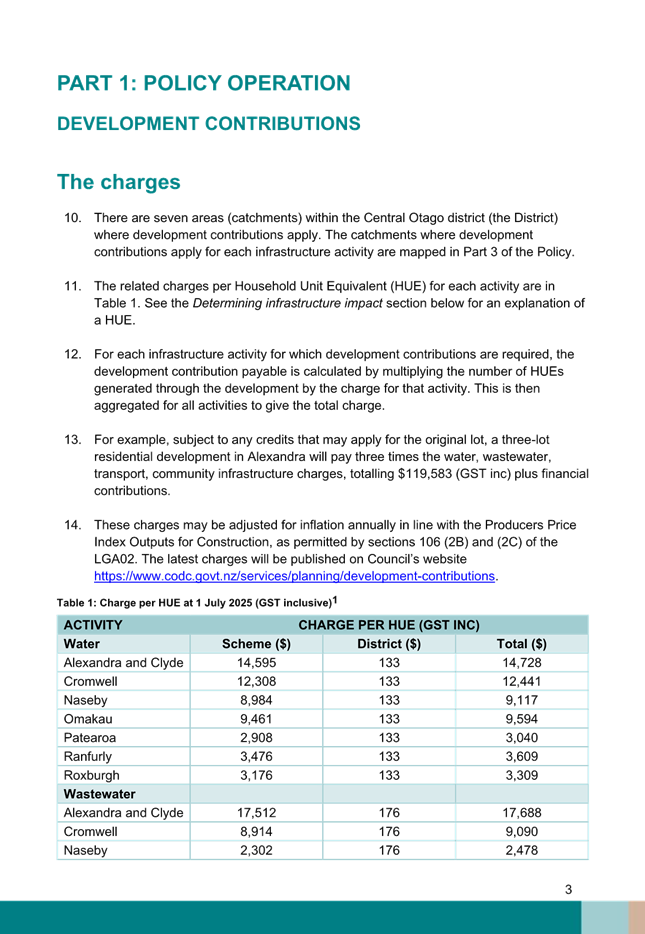

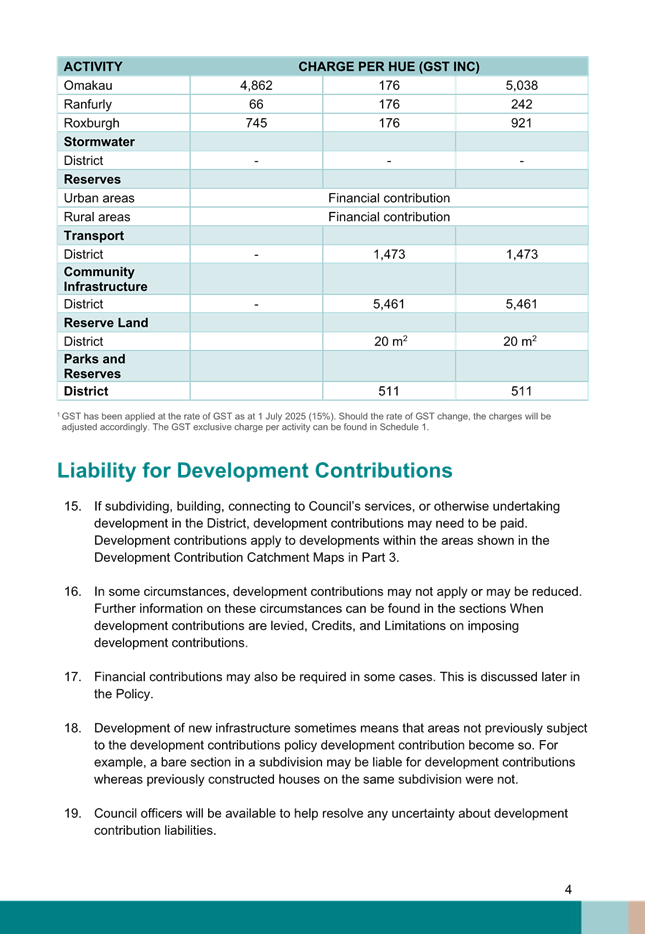

|

|

Reviewed

and authorised by:

|

Peter Kelly, Chief Executive

Officer

|

1. Purpose

of Report

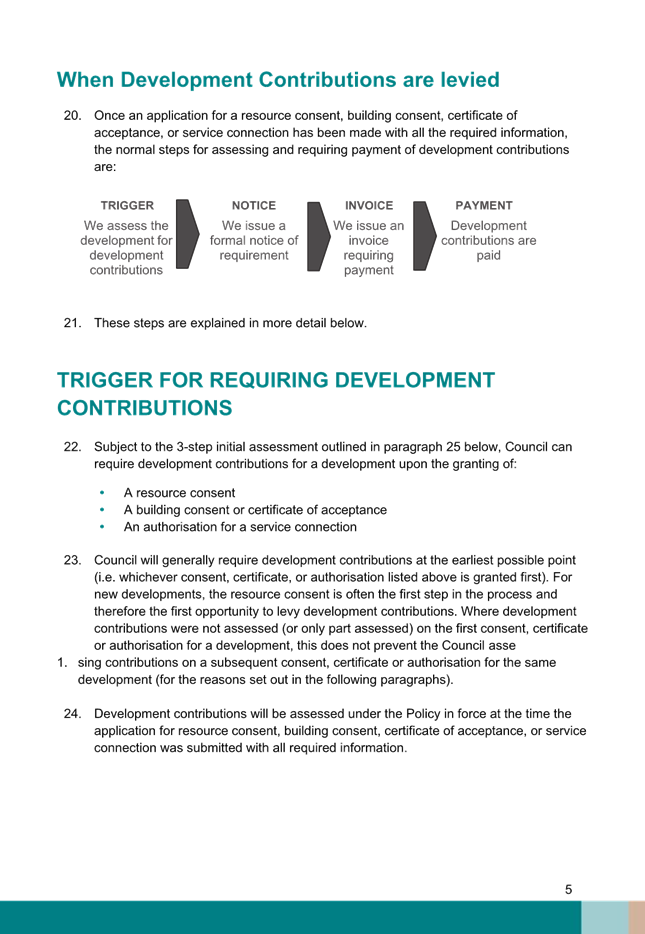

To consider approving the

2025-34 draft Consultation Document for the Long-term Plan and supporting

information to the Consultation Document be provided to Audit New Zealand.

|

Recommendations

That the Council

A. Receives

the report and accepts the level of significance.

B. Approves that the draft Consultation

Document be provided to Audit New Zealand for audit as required under the

Local Government Act 2002.

C. Approves the following supporting

information to the Consultation Document be provided to Audit New Zealand to

facilitate the audit:

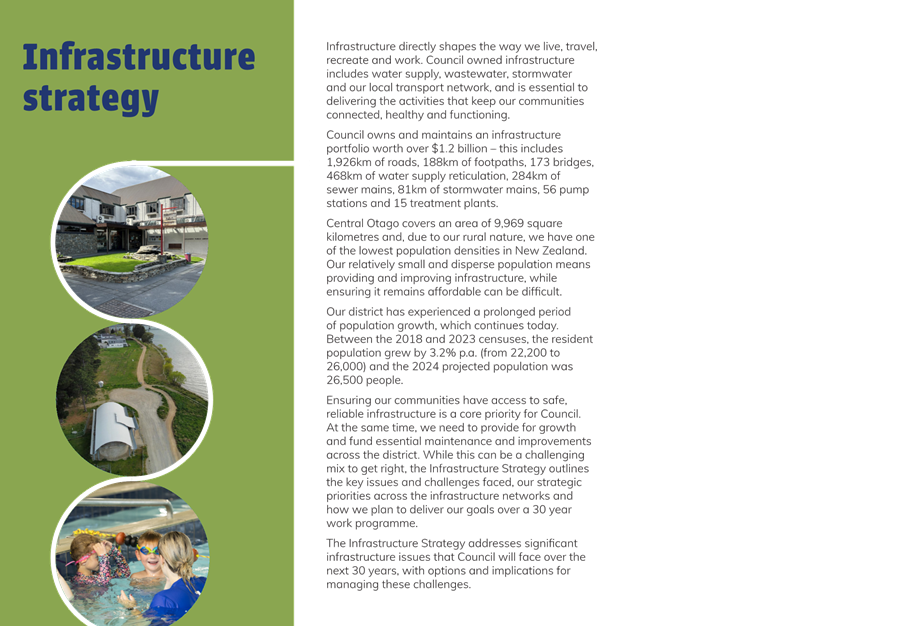

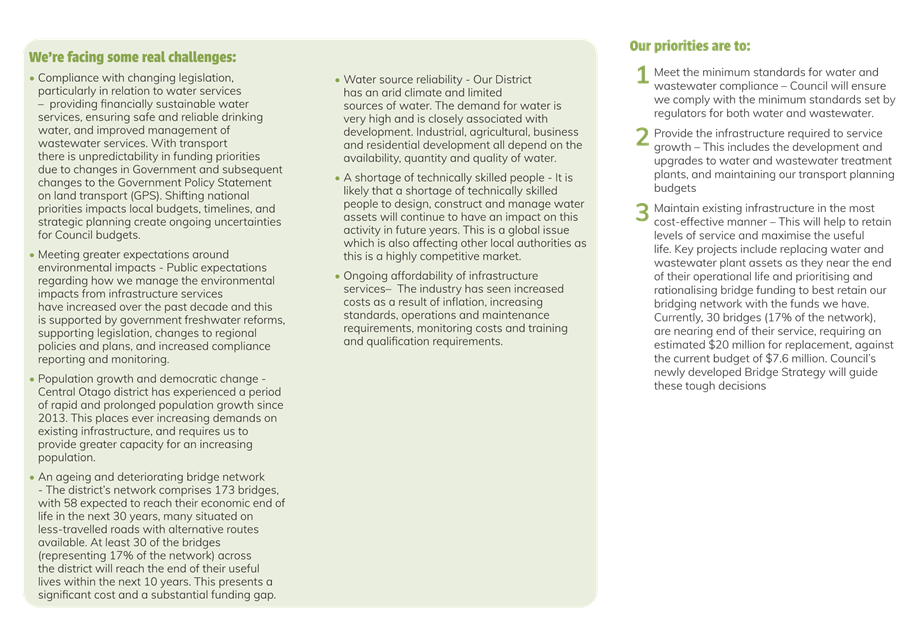

(a) Infrastructure

Strategy

(b) Financial

Strategy

(c) Development

and Financial Contributions Policy

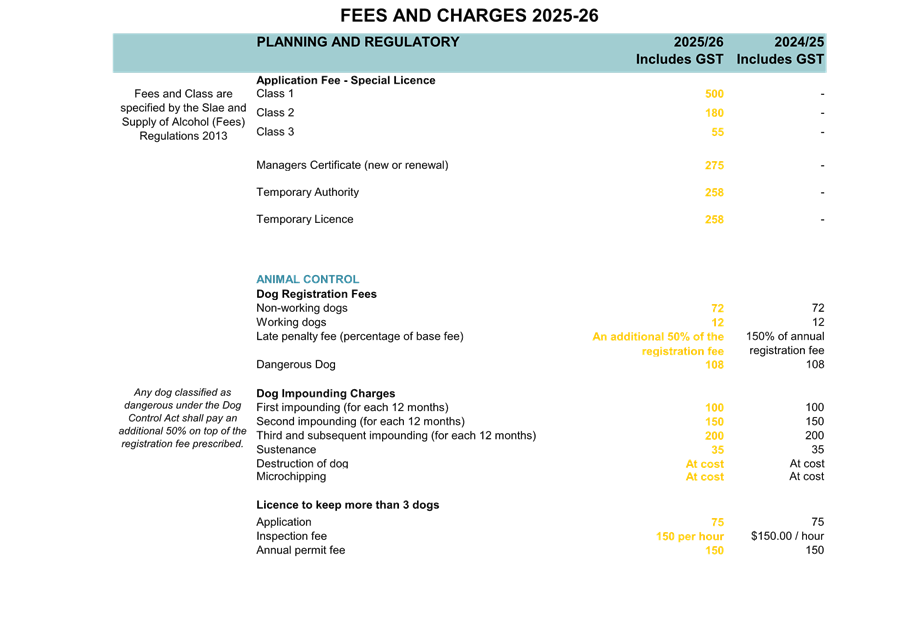

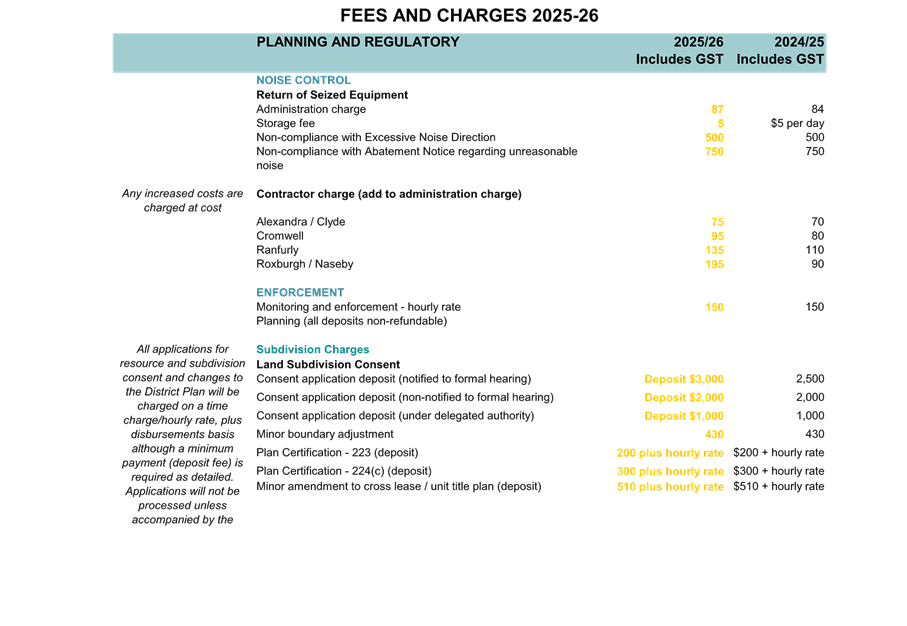

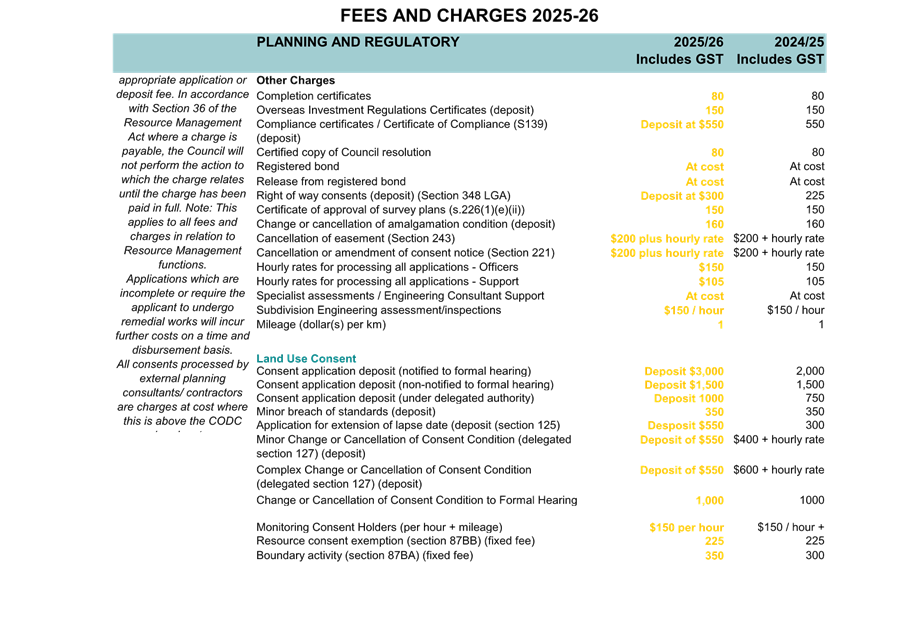

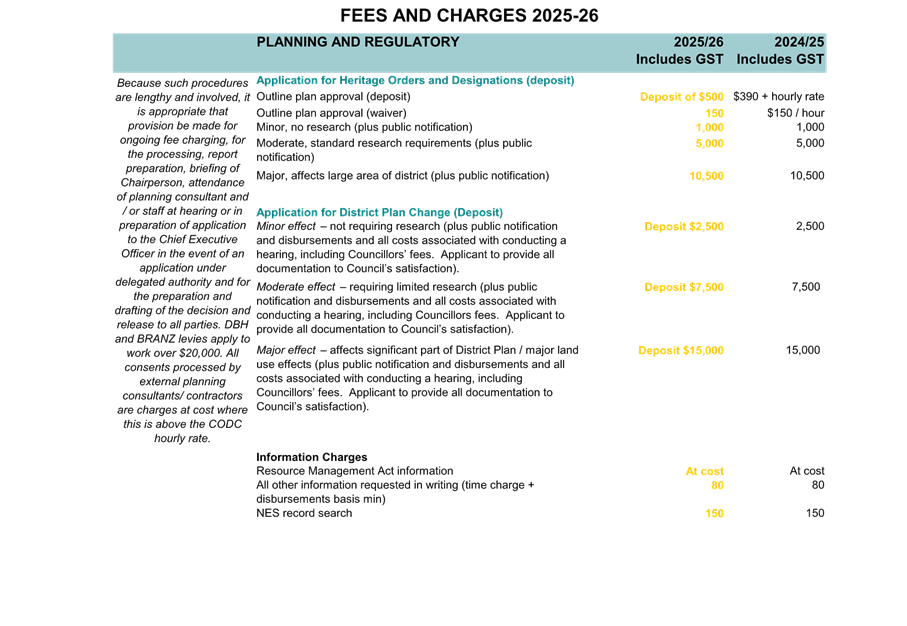

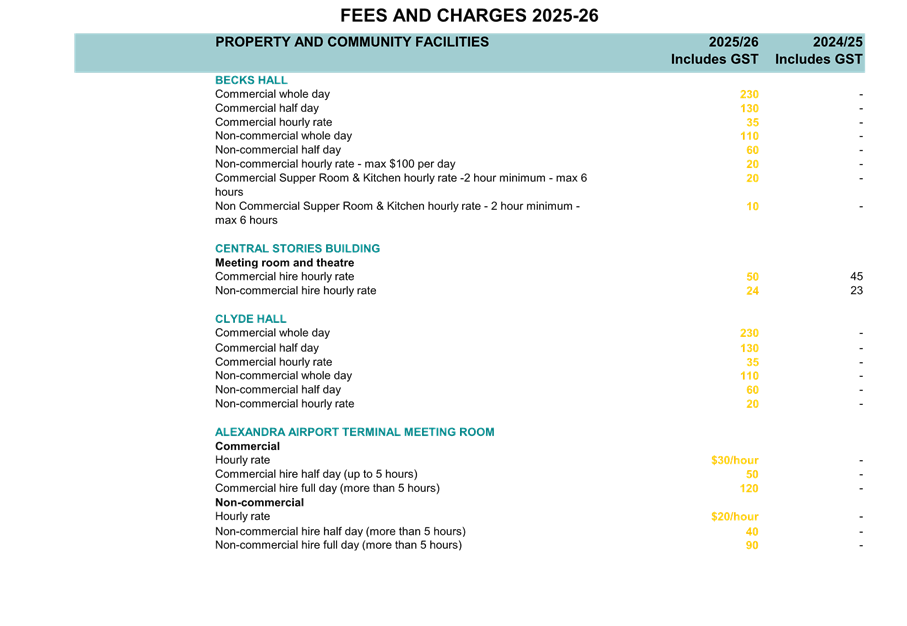

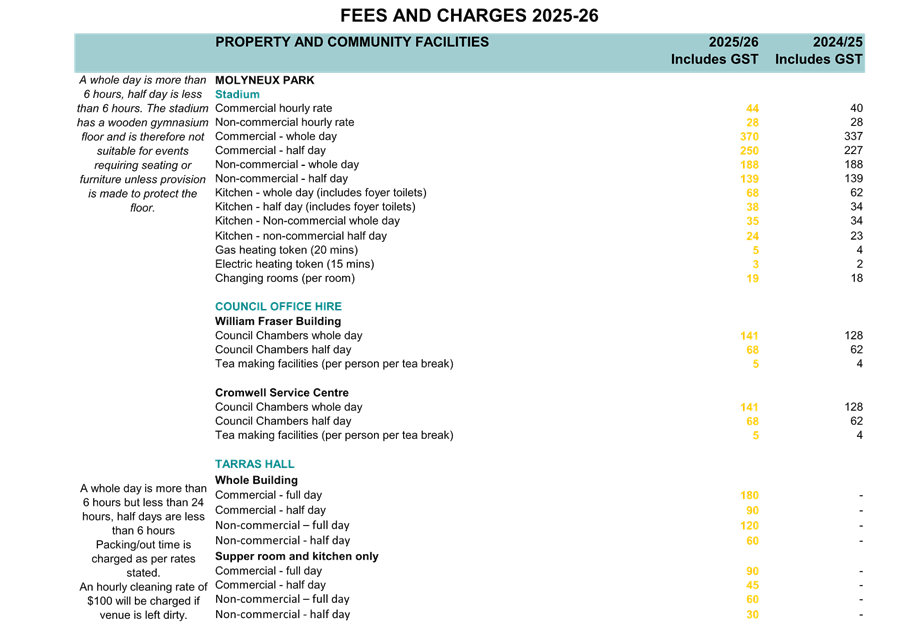

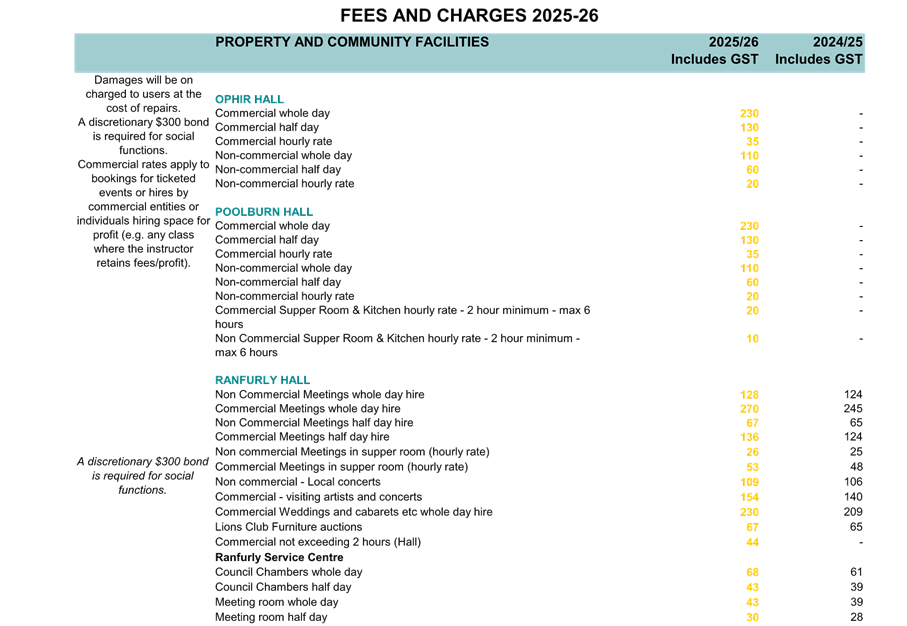

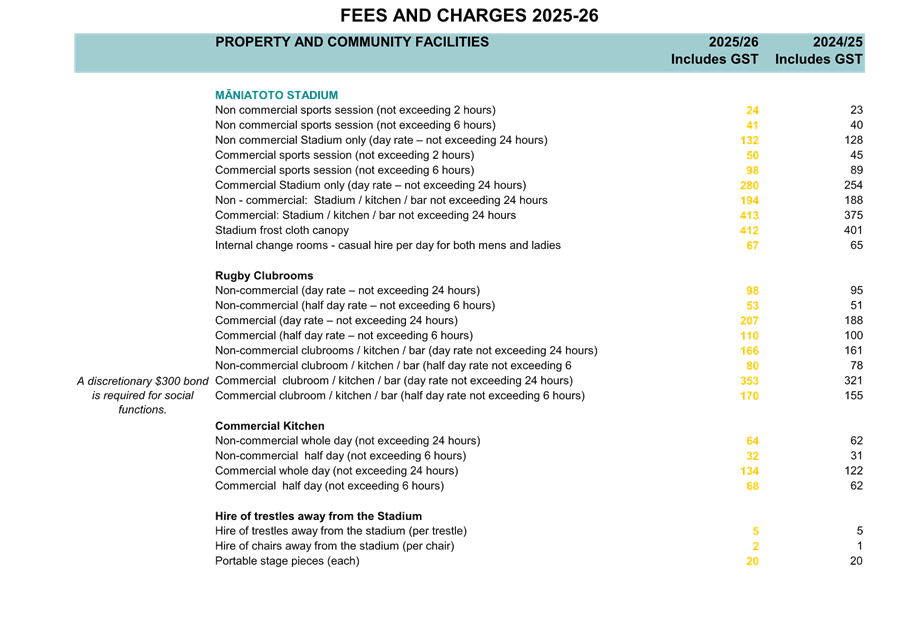

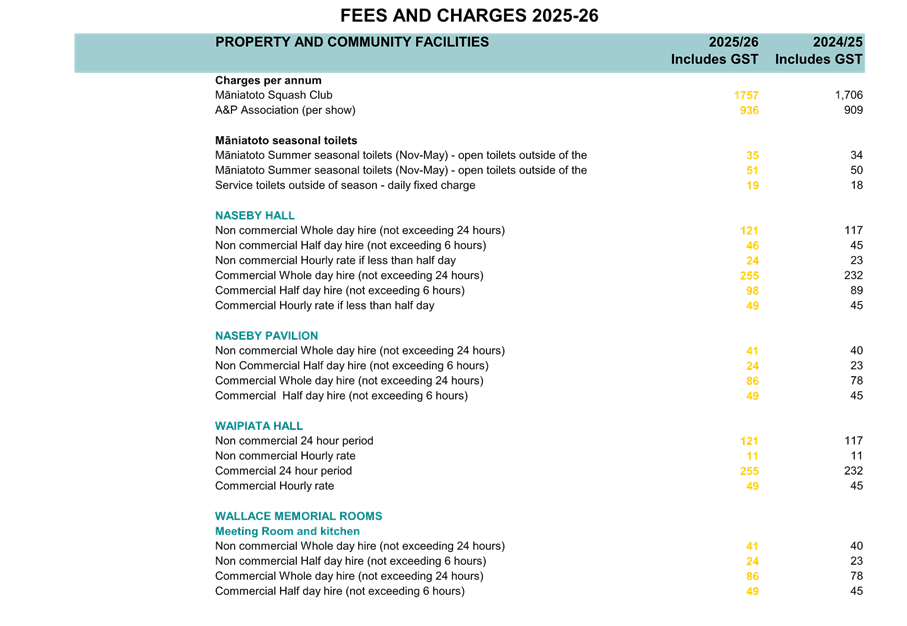

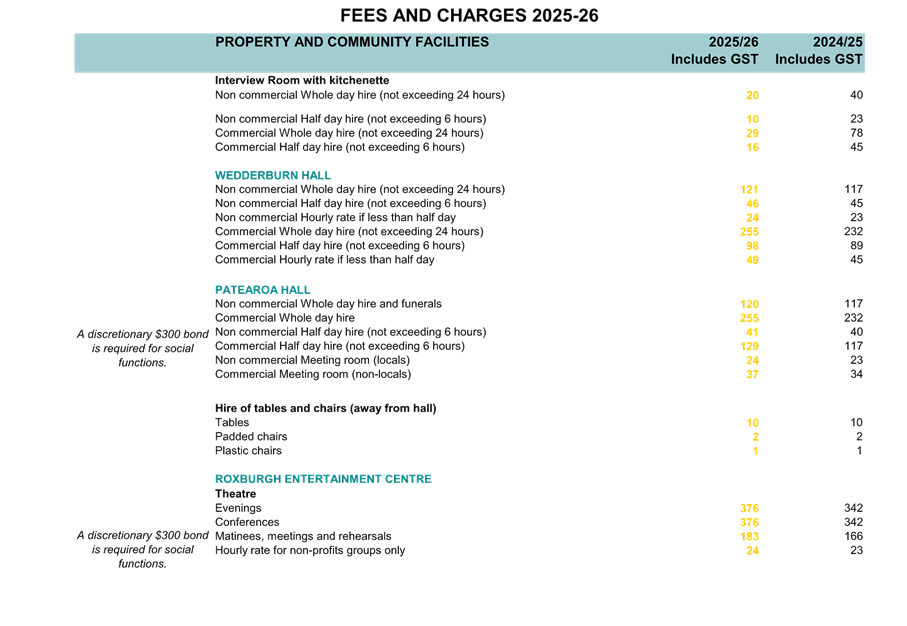

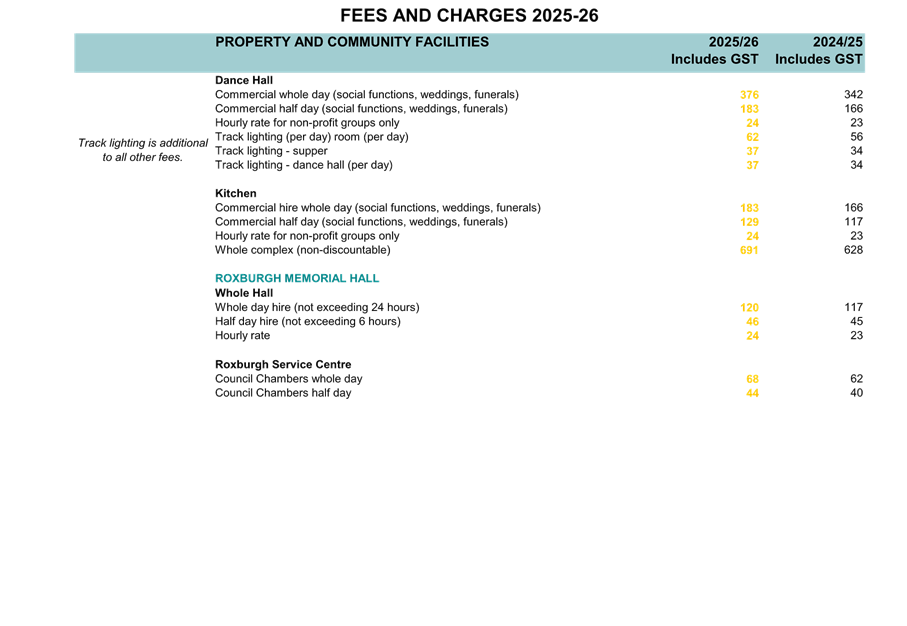

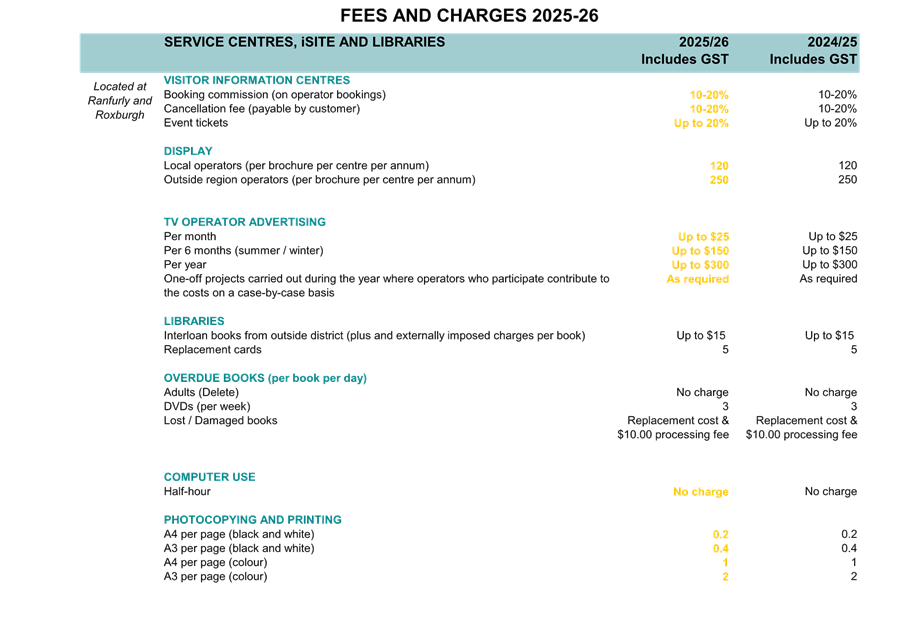

(d) Fees

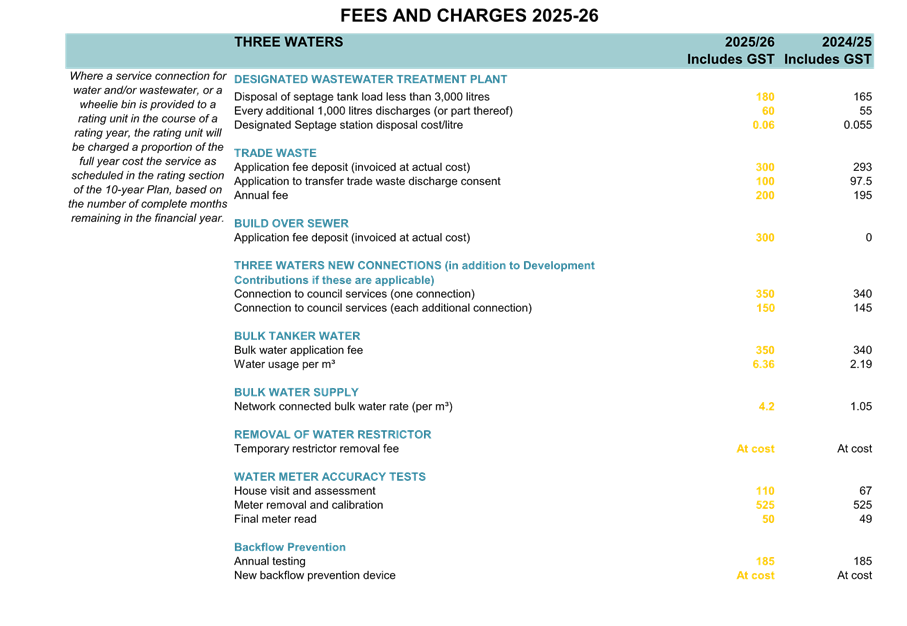

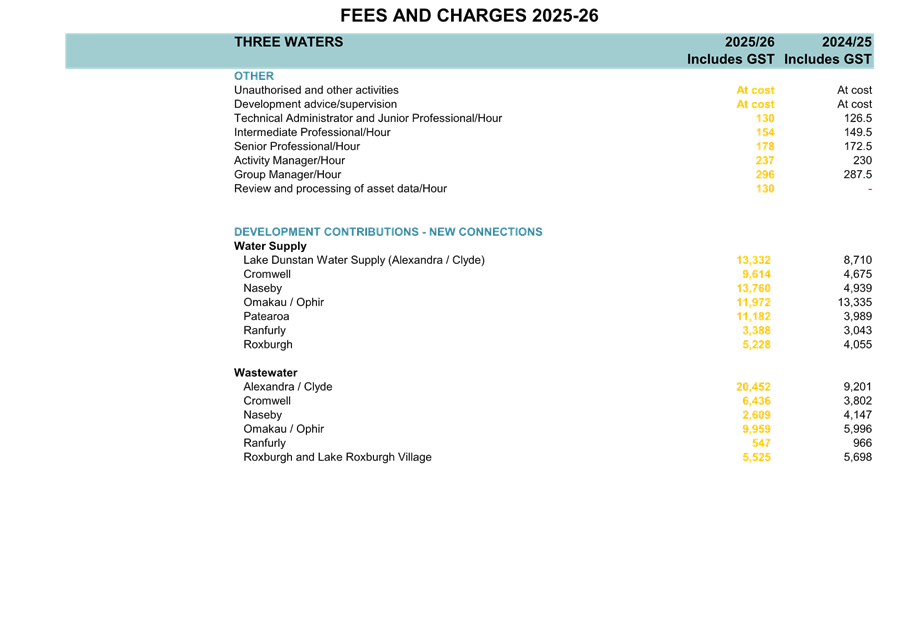

and Charges

(e) Significance

and Engagement Policy

(f) Revenue

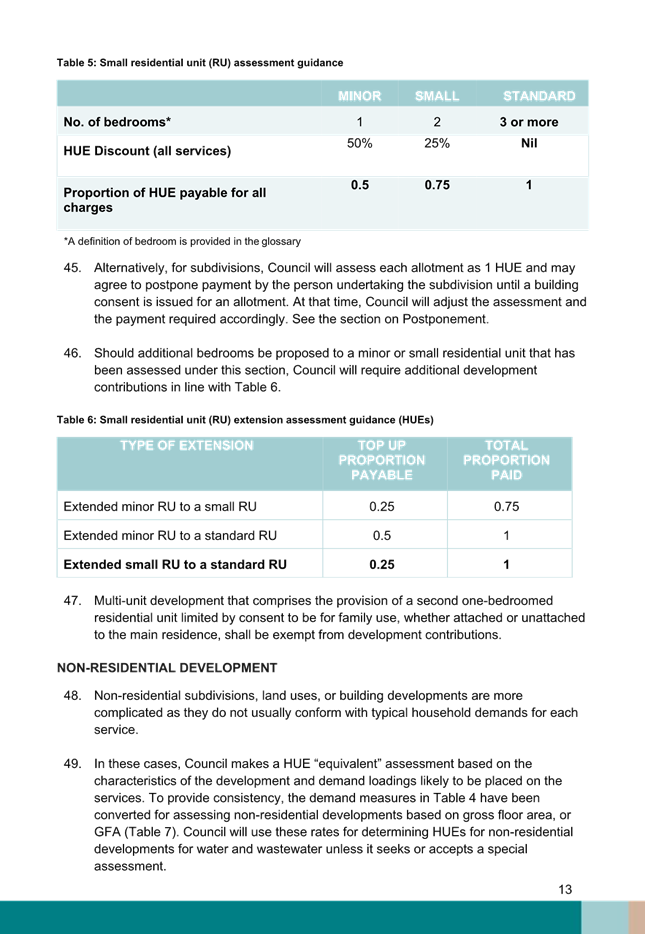

and Financing Policy

(g) Rates Remission and Postponement Policy

(h) Liability

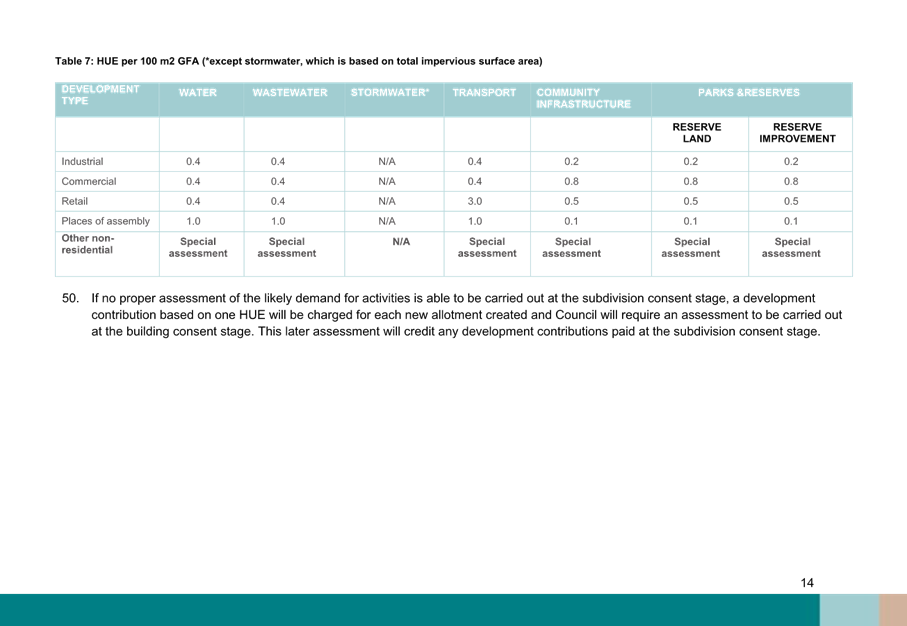

Management Policy

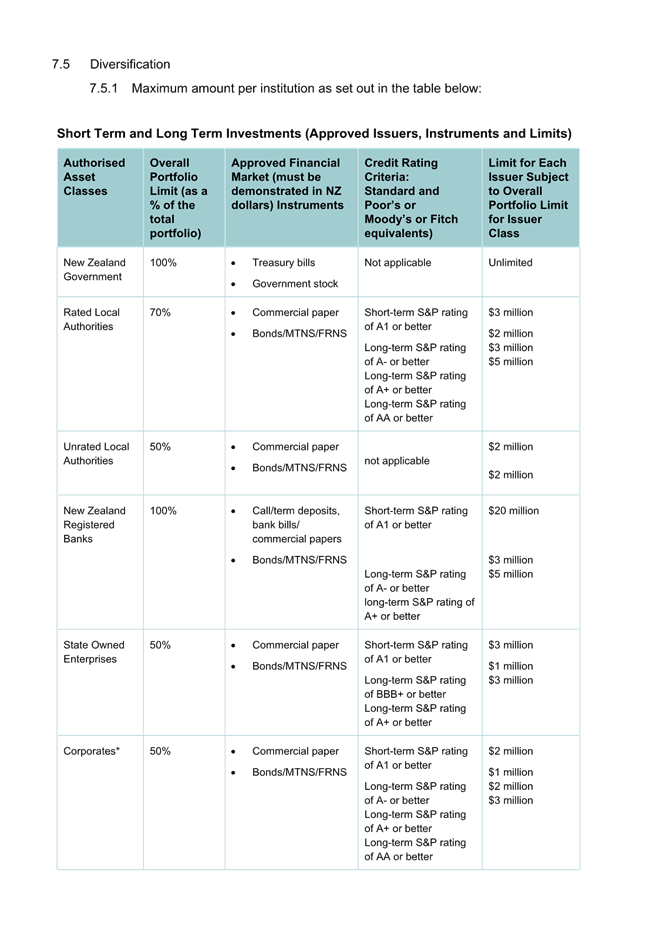

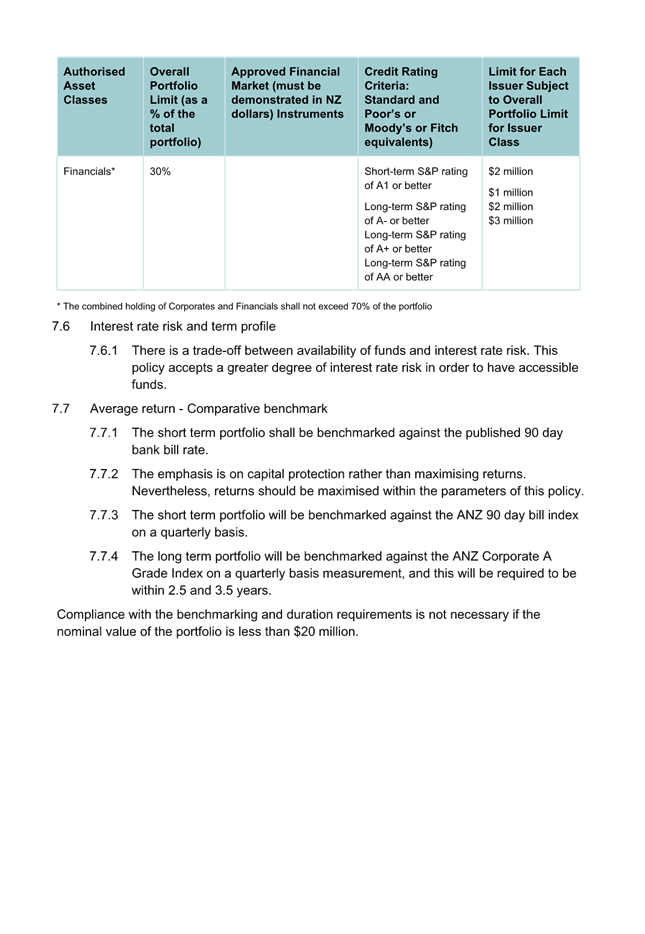

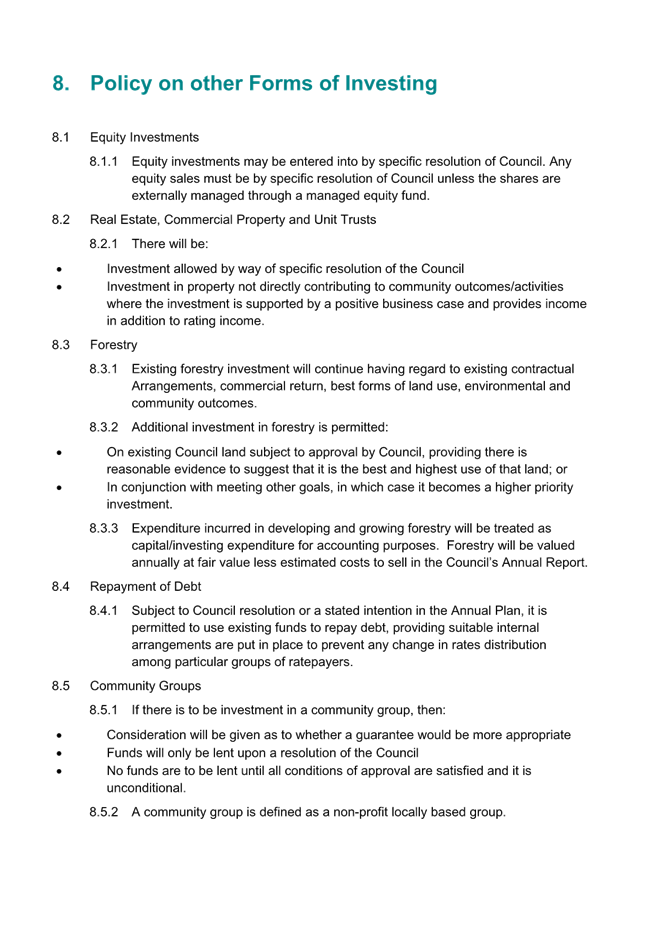

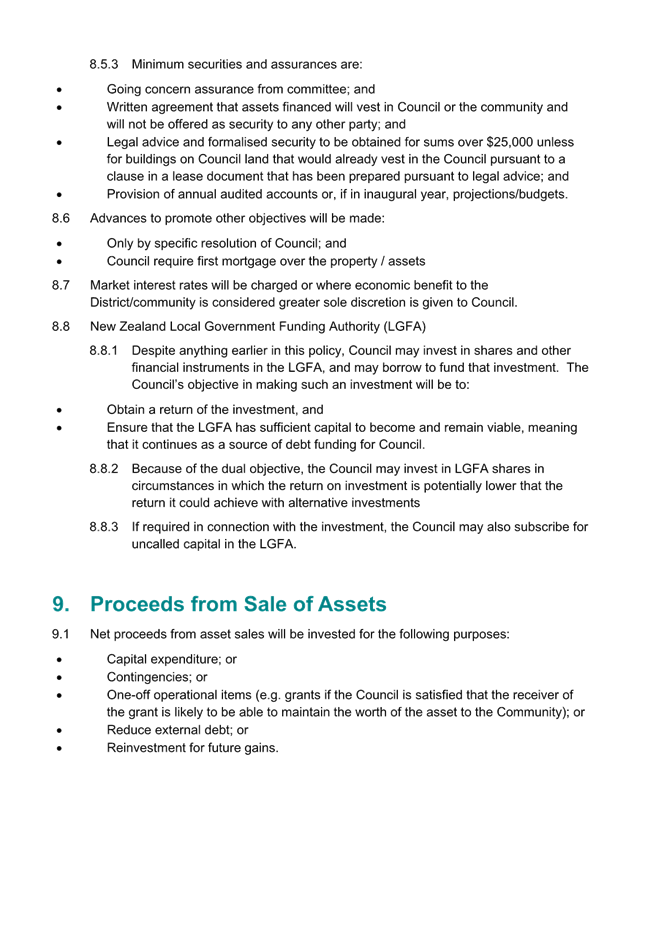

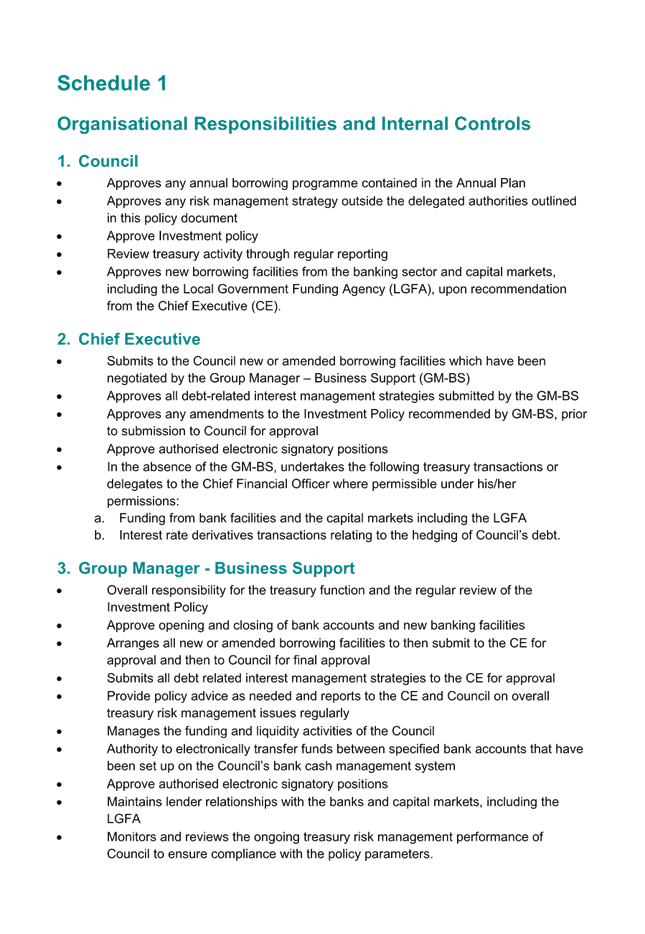

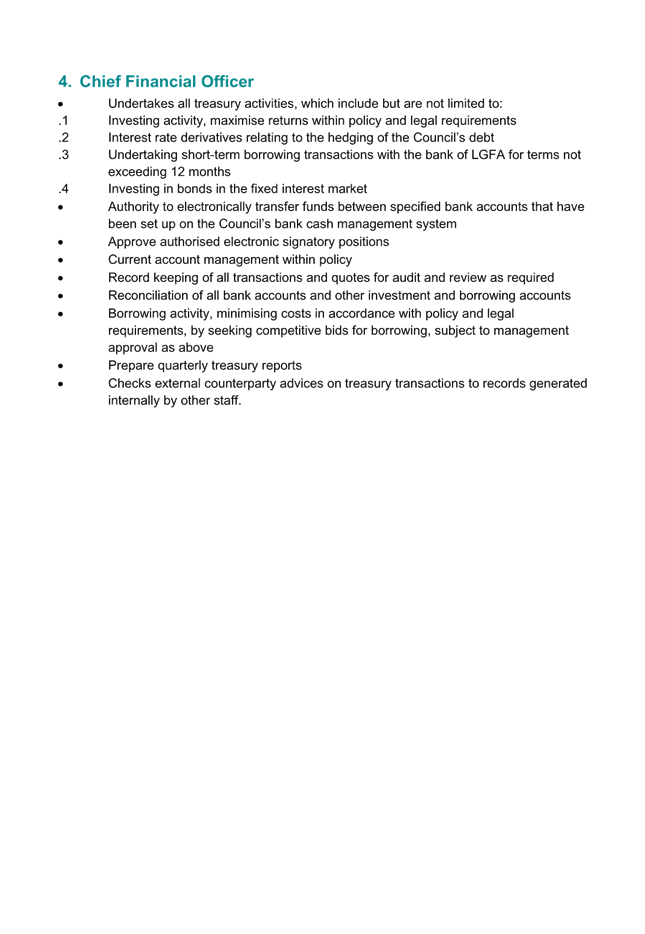

(i) Investment

Policy

(j) Prospective

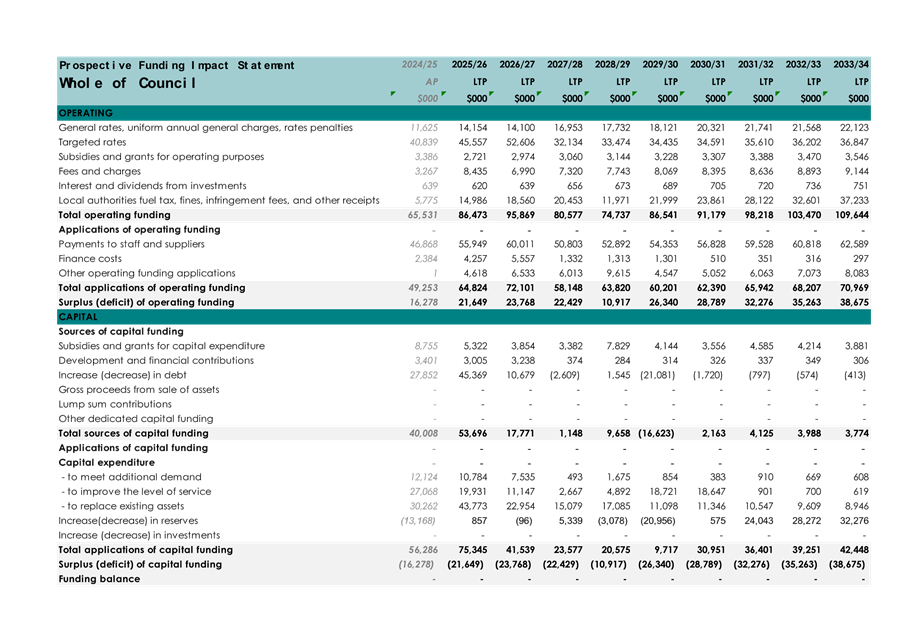

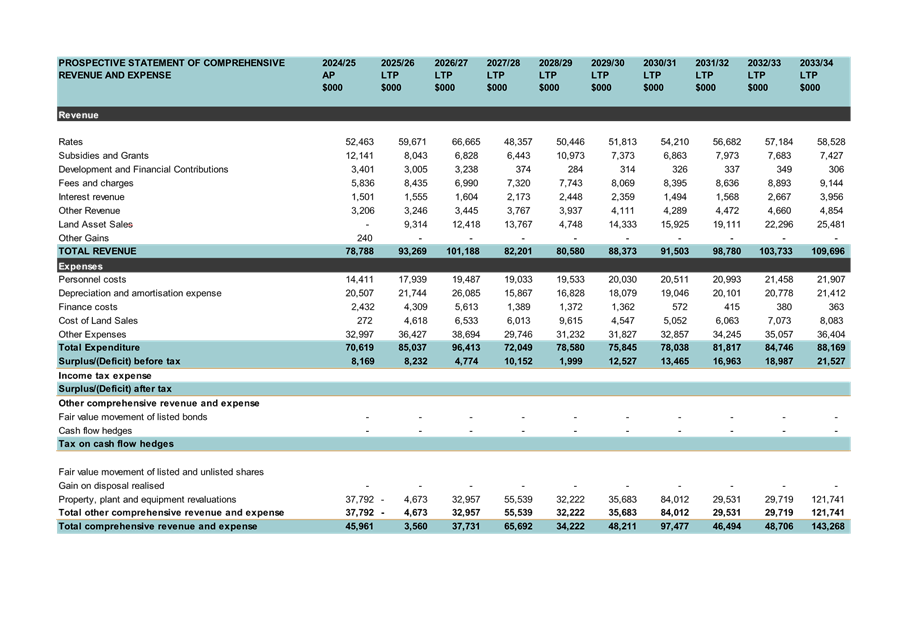

Financial Statements and Prospective Funding Impact Statements

(k) Community

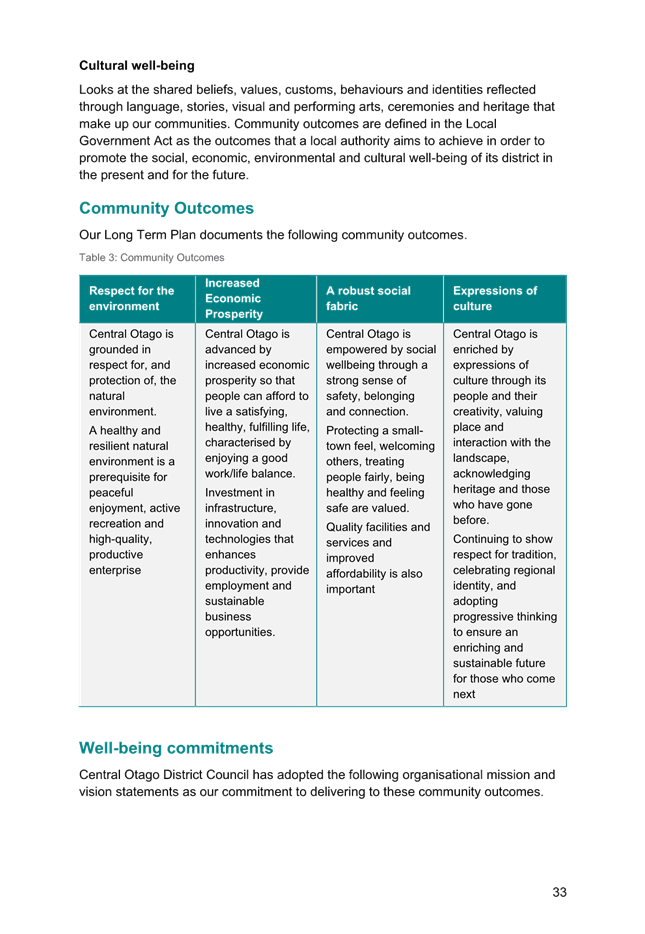

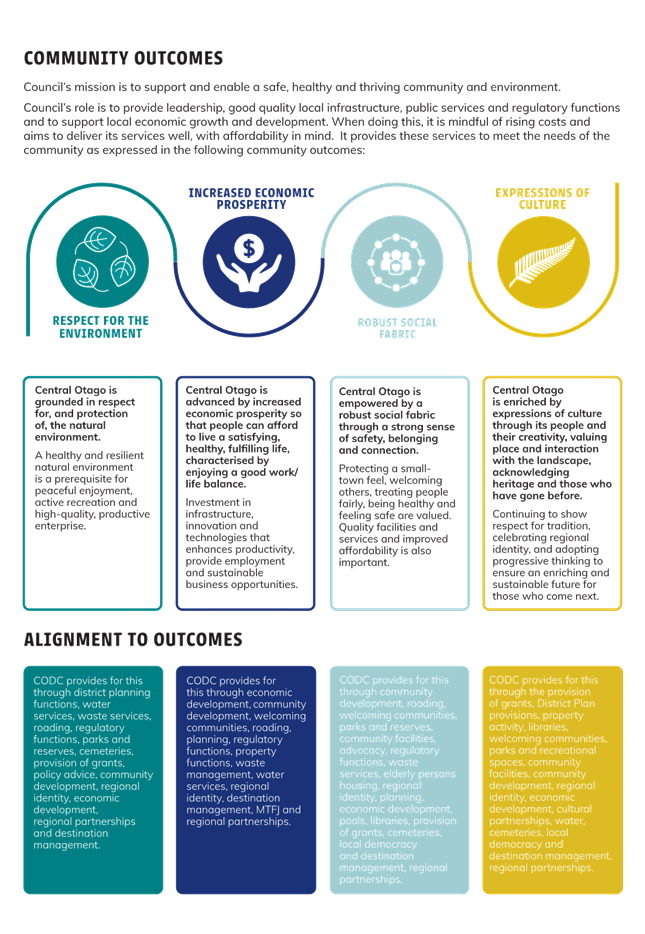

Outcomes Development

(l) Significant

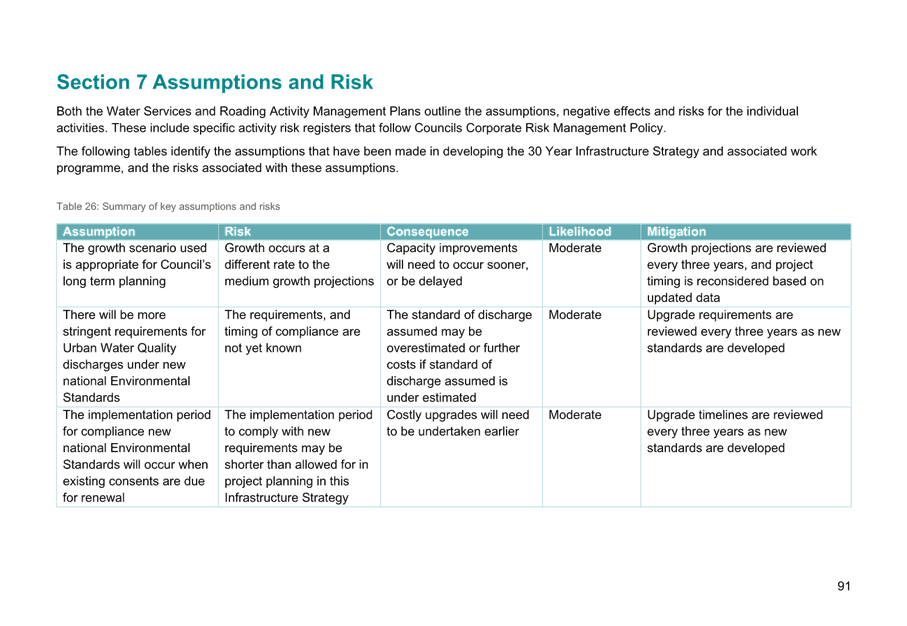

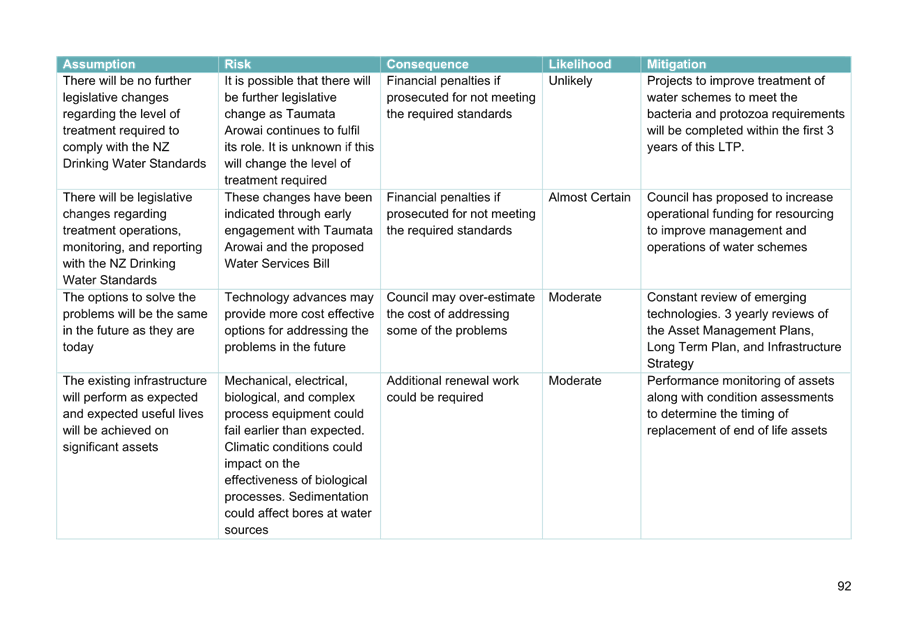

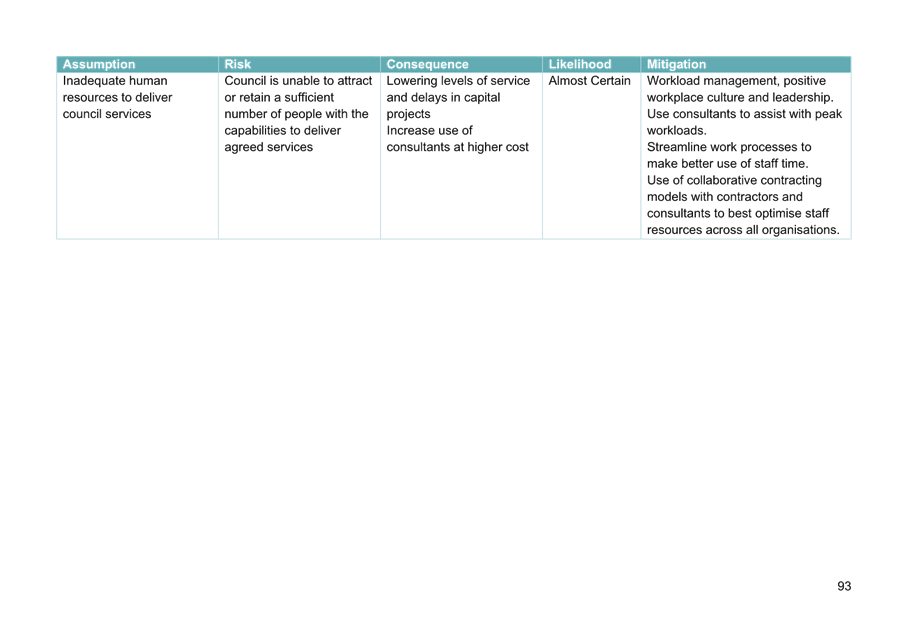

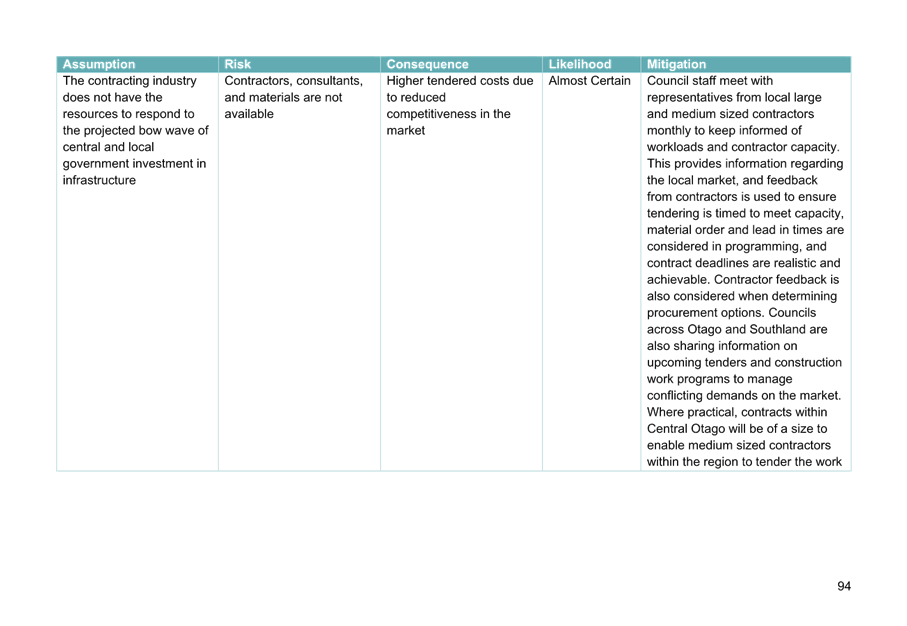

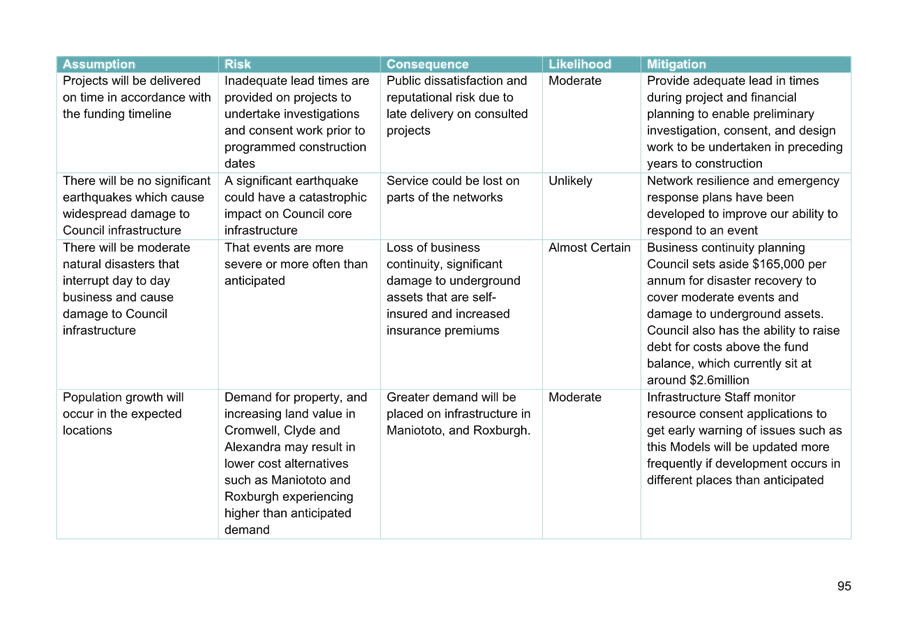

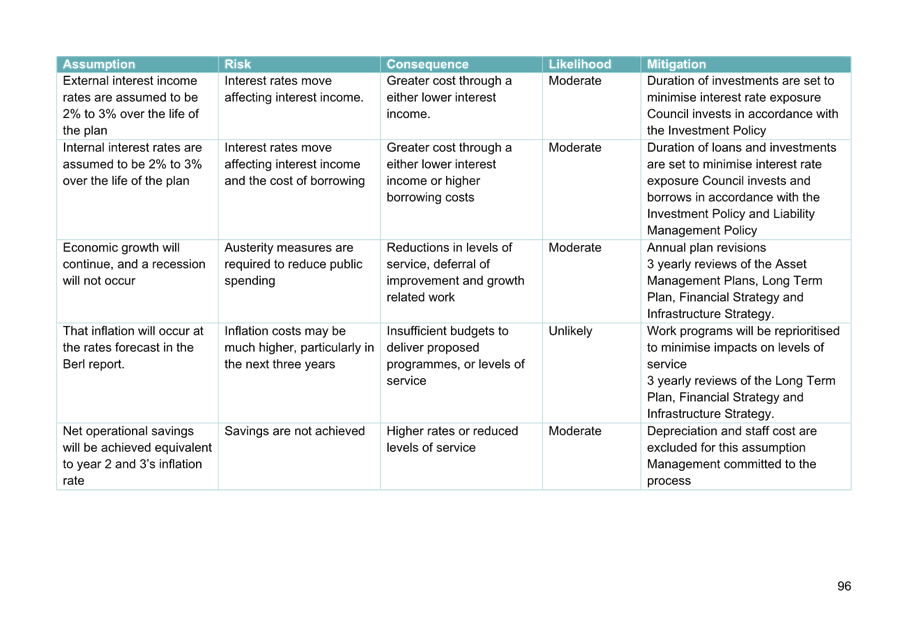

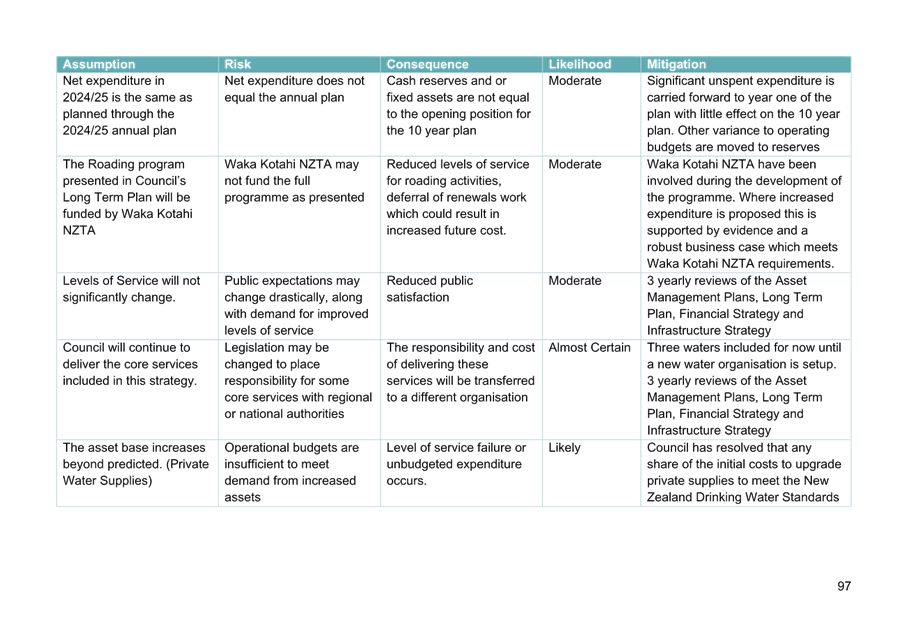

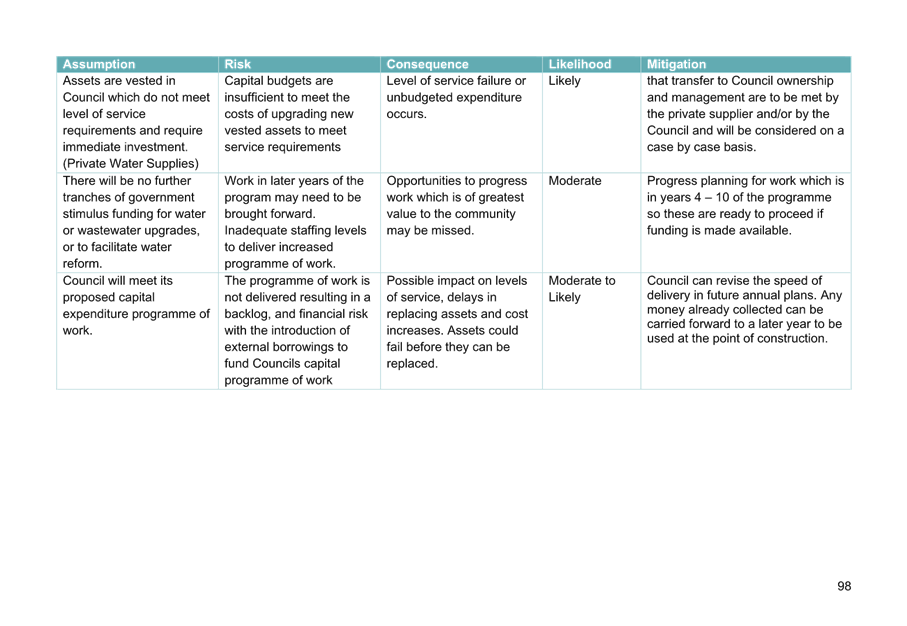

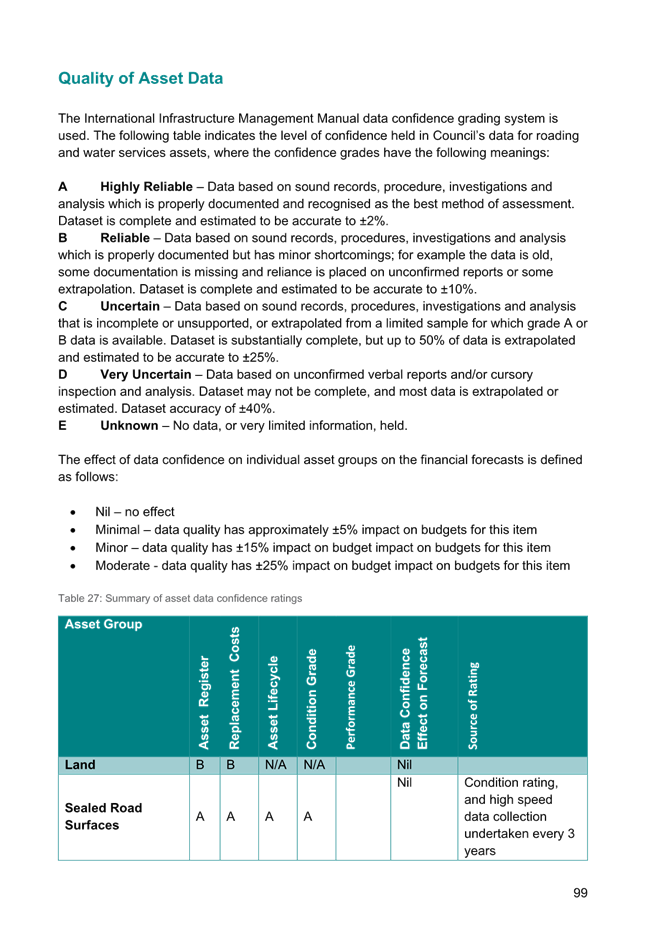

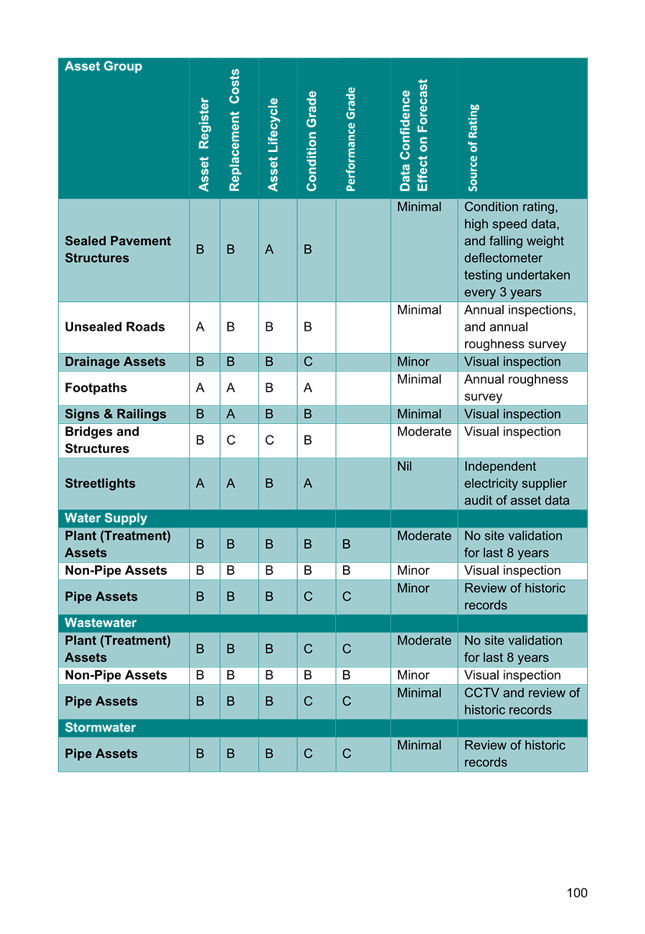

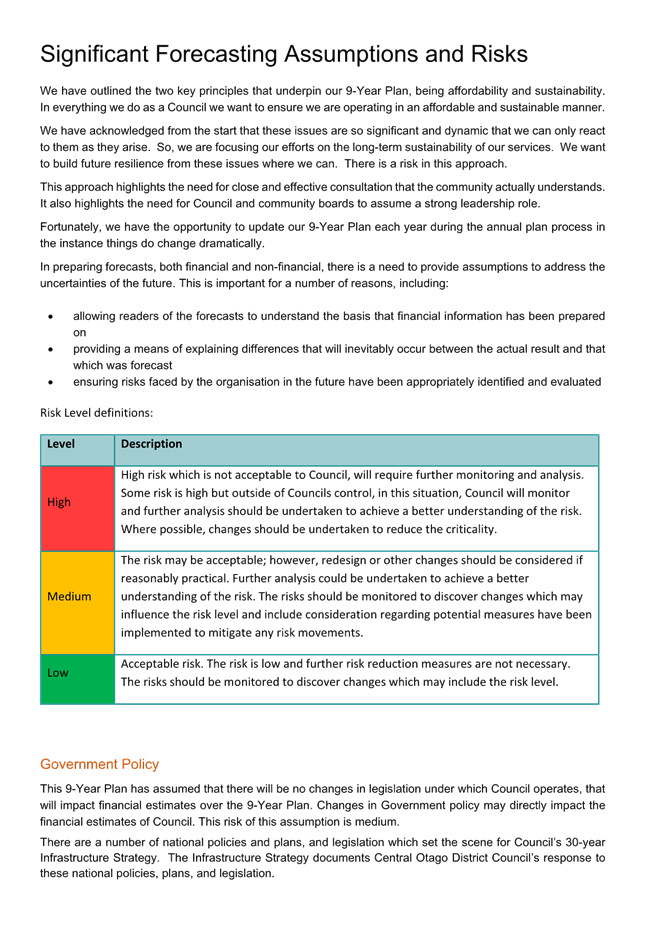

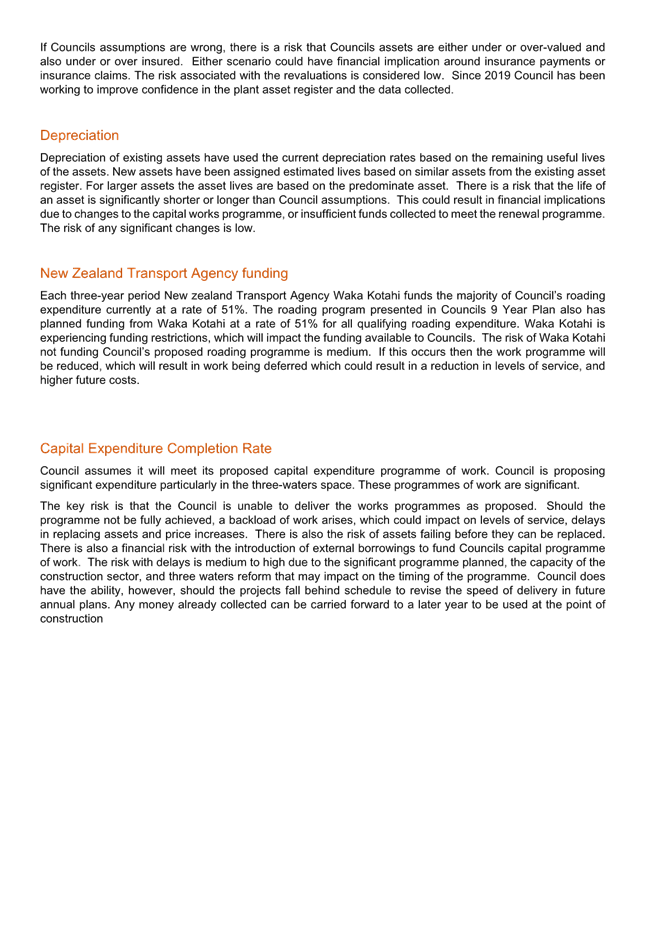

Forecasting Assumptions and Risks

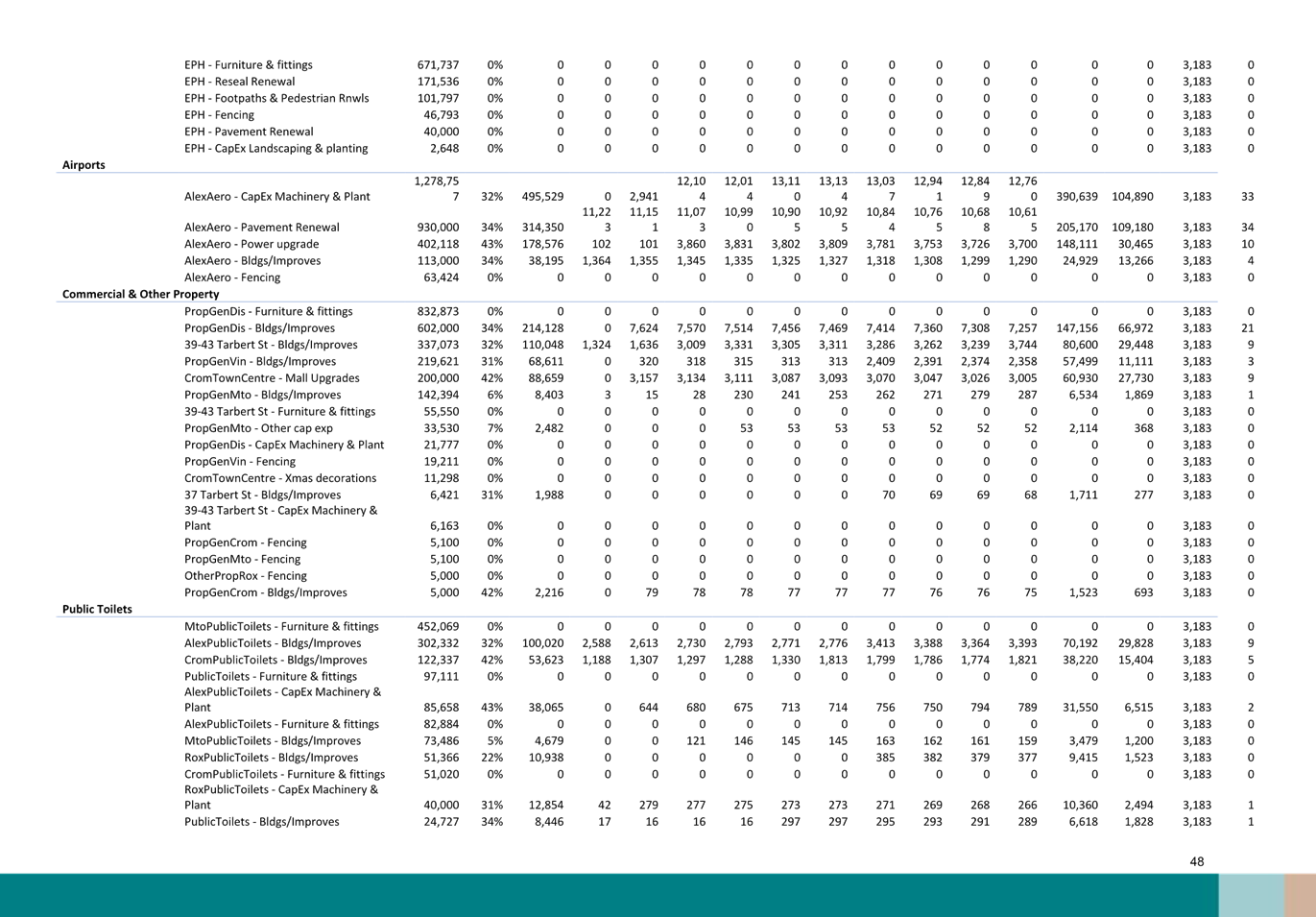

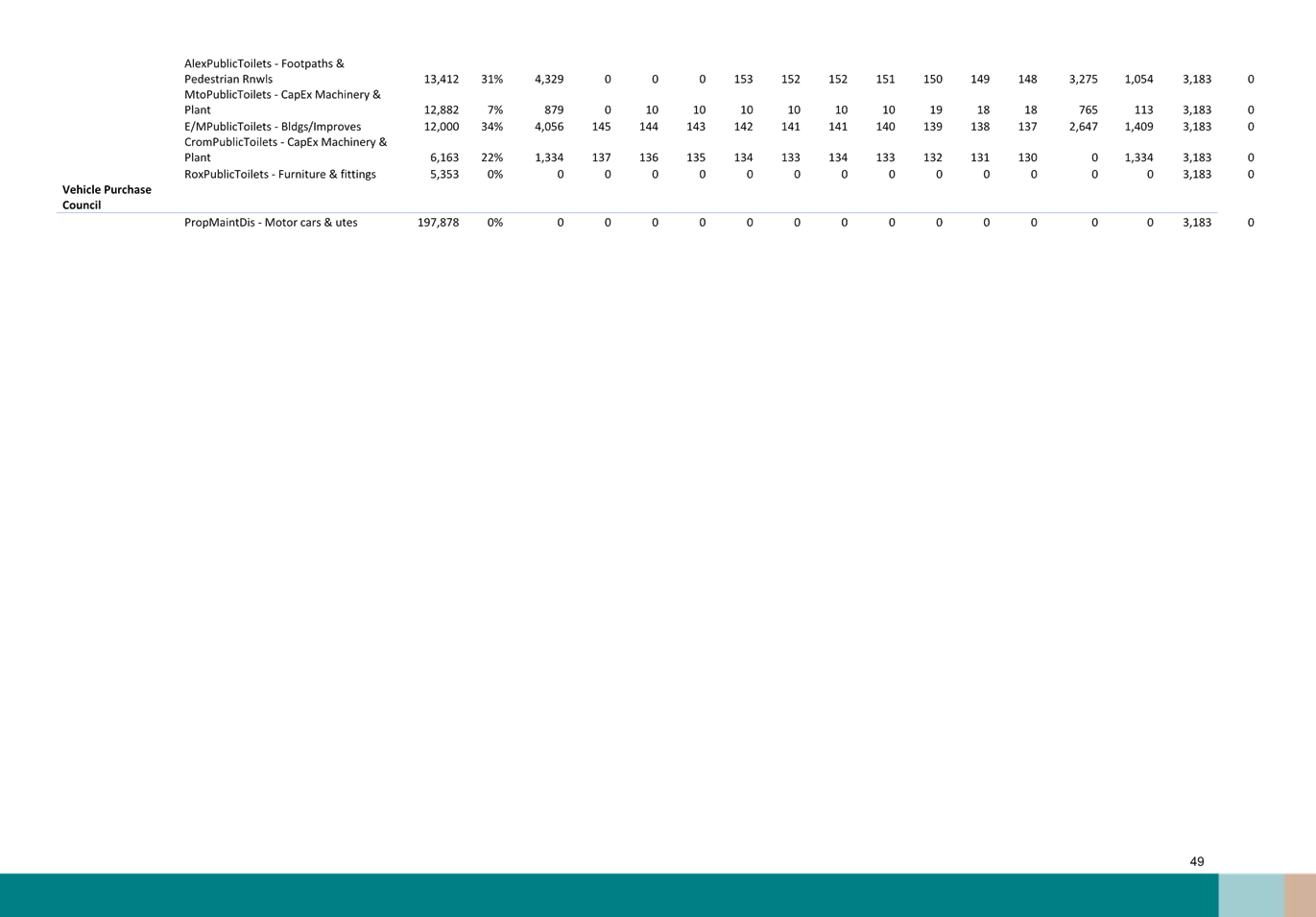

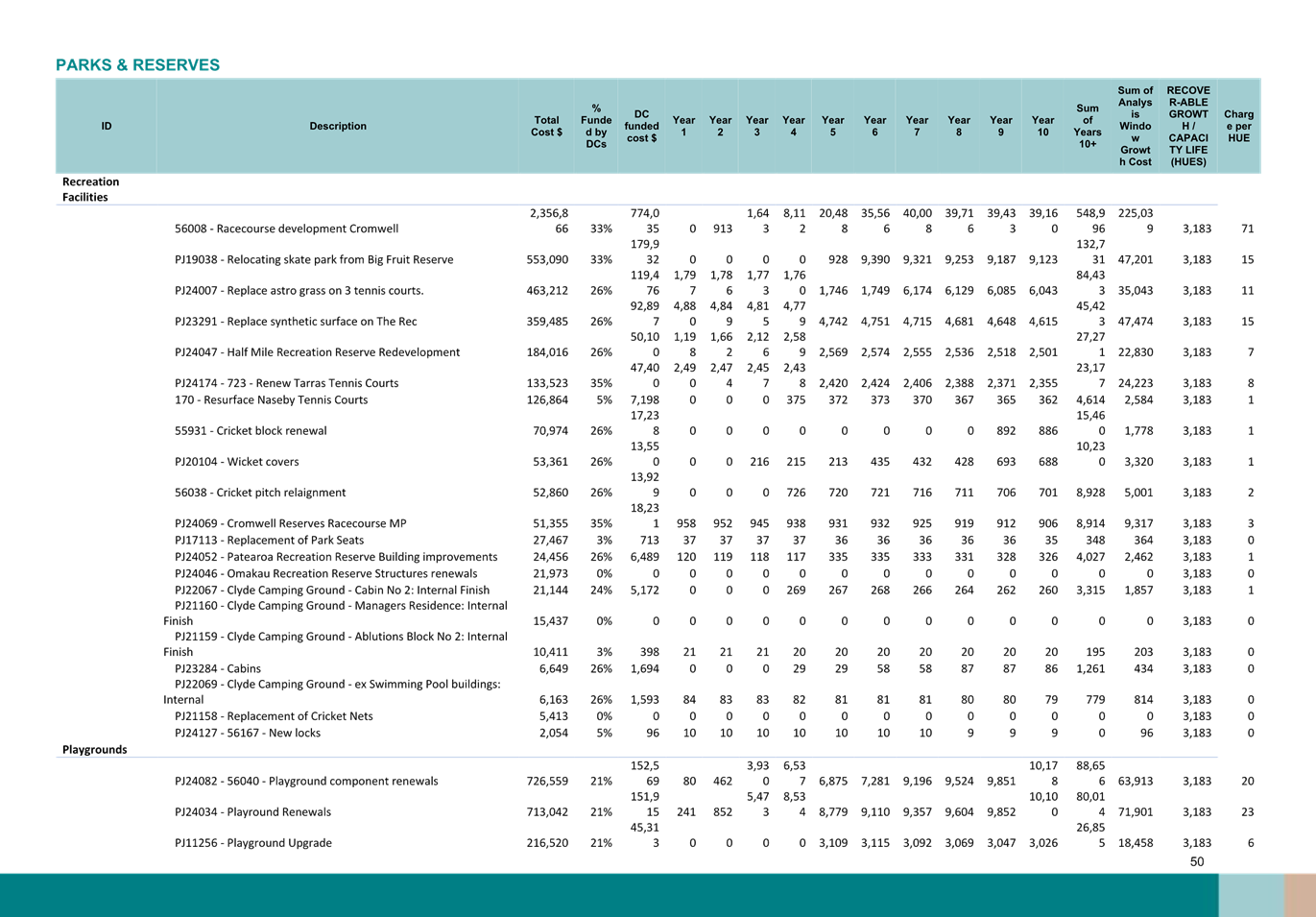

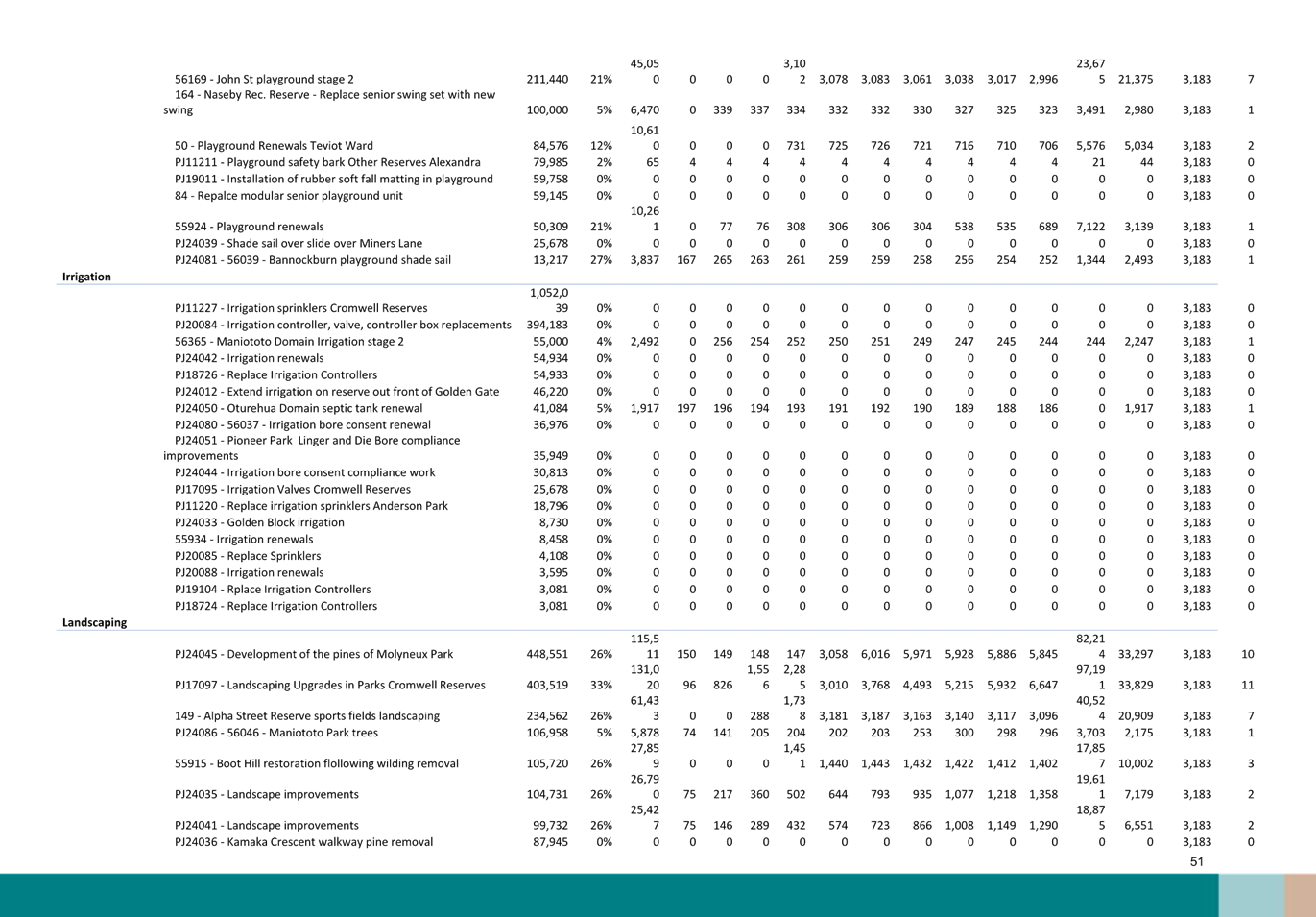

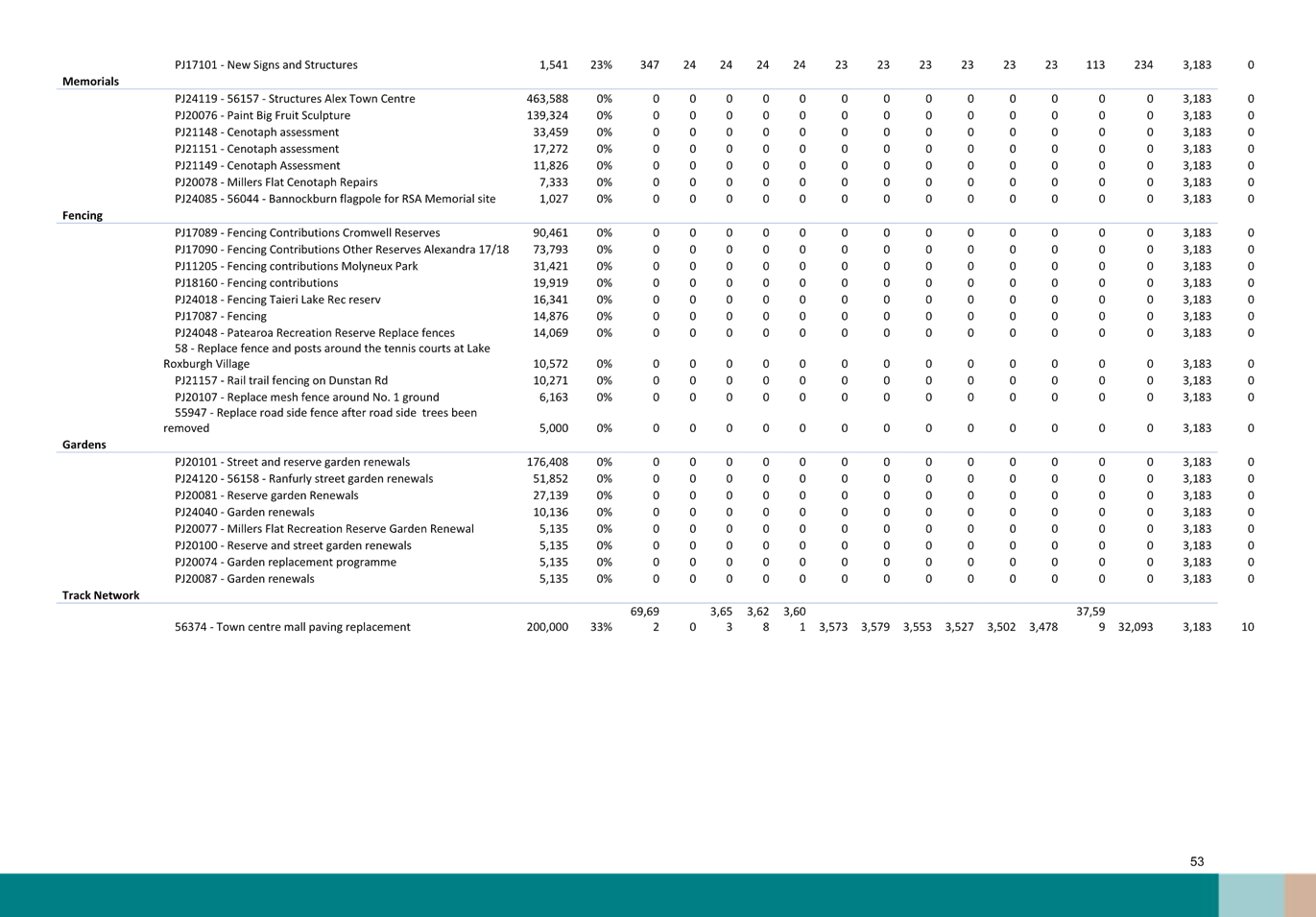

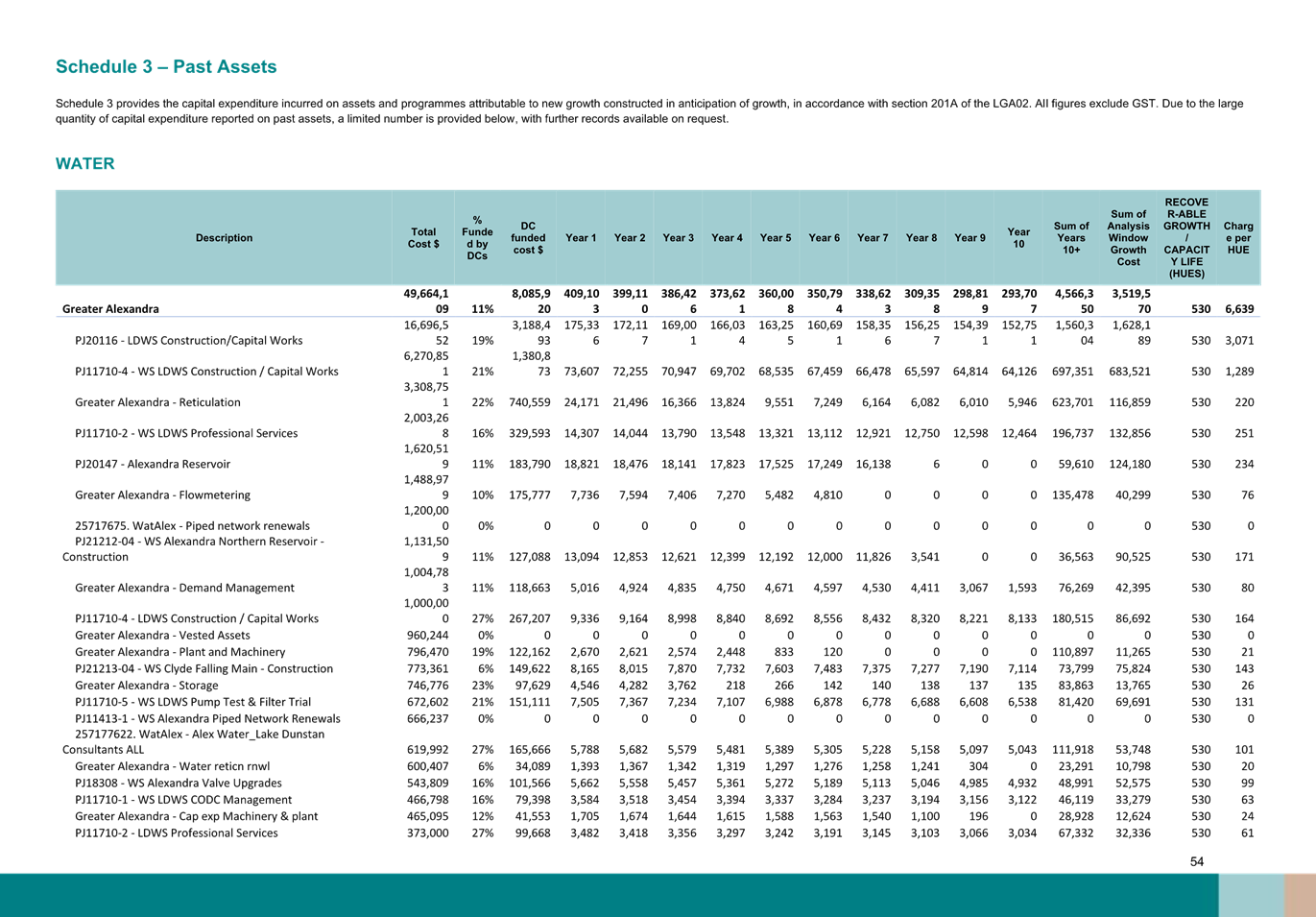

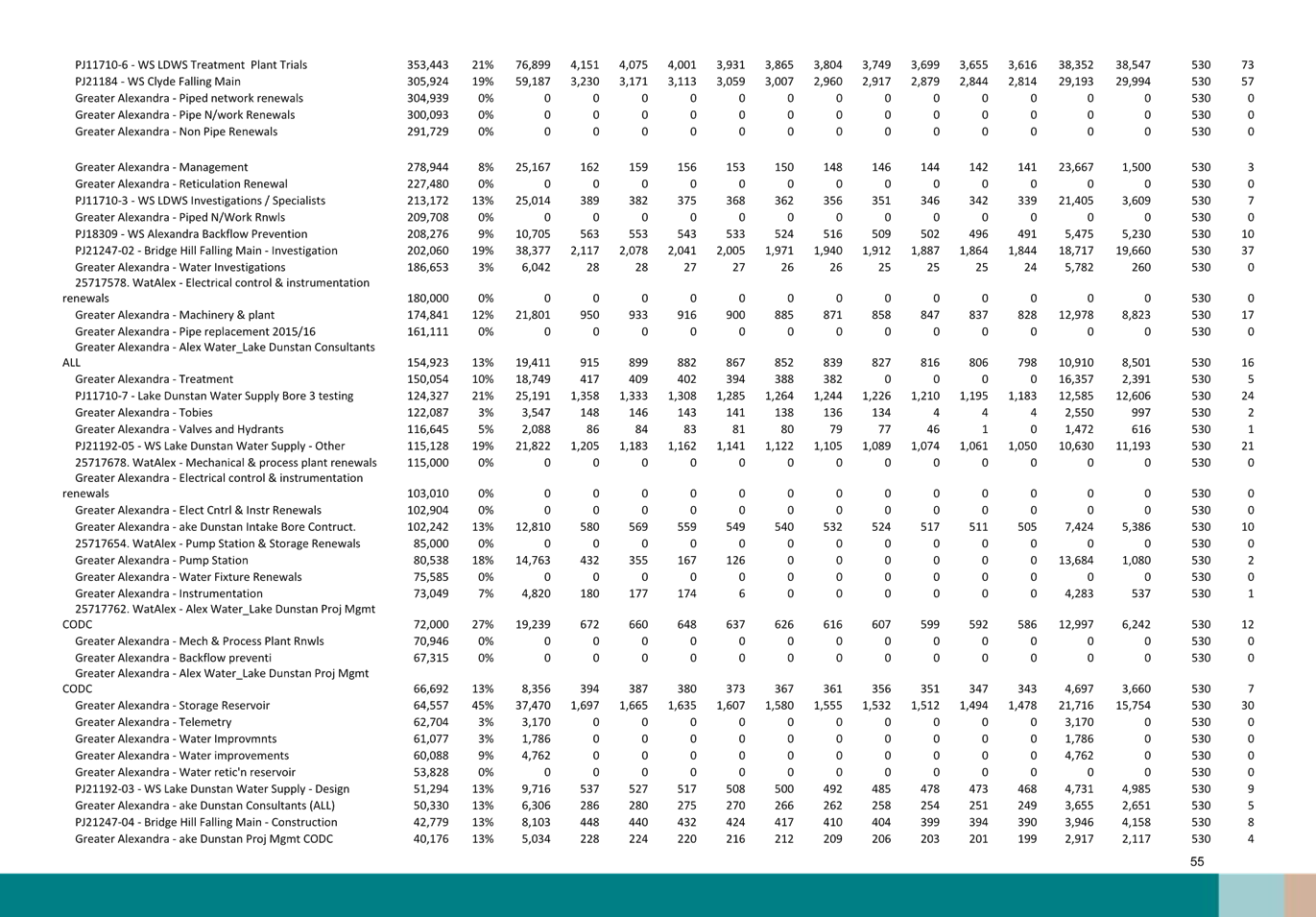

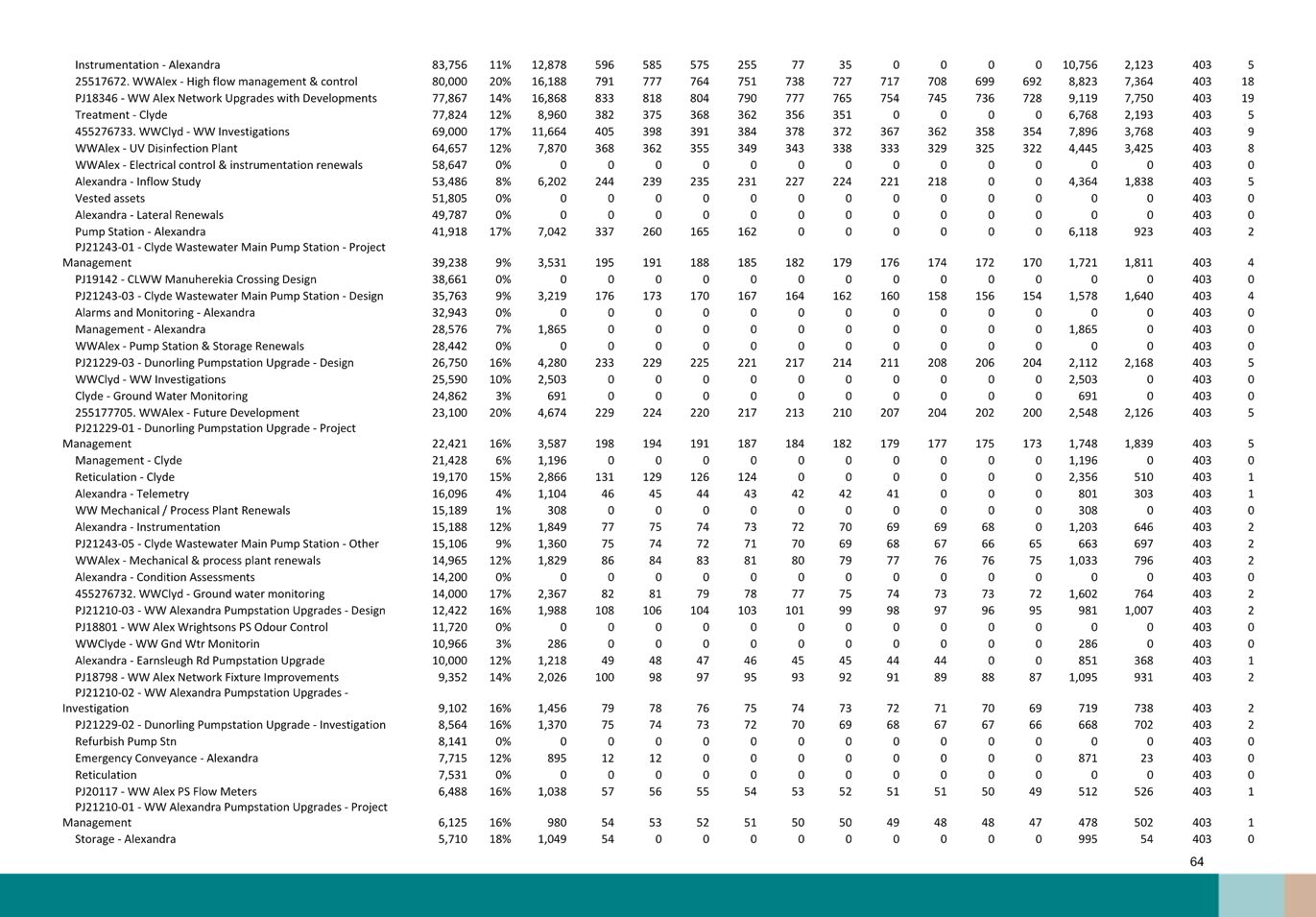

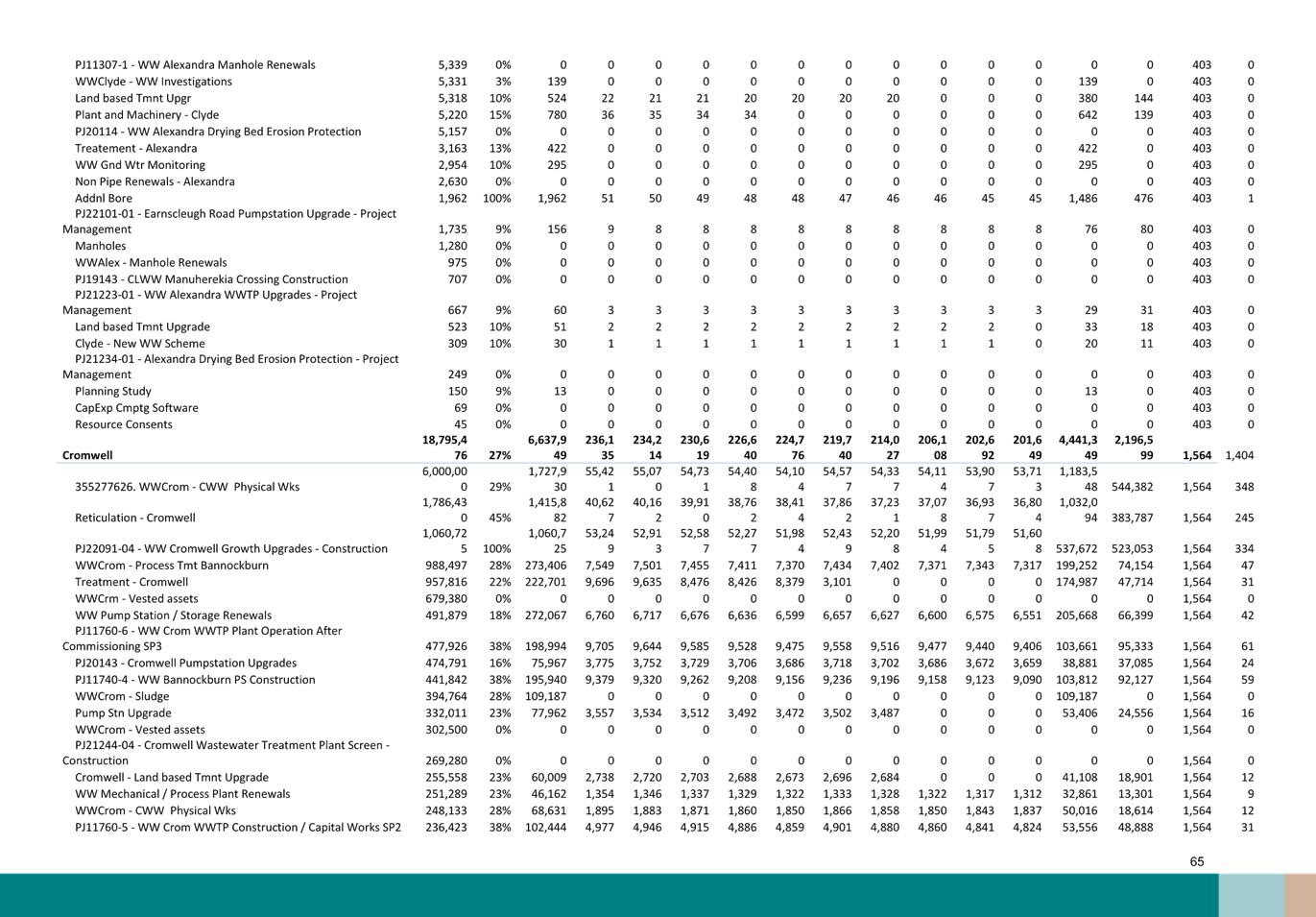

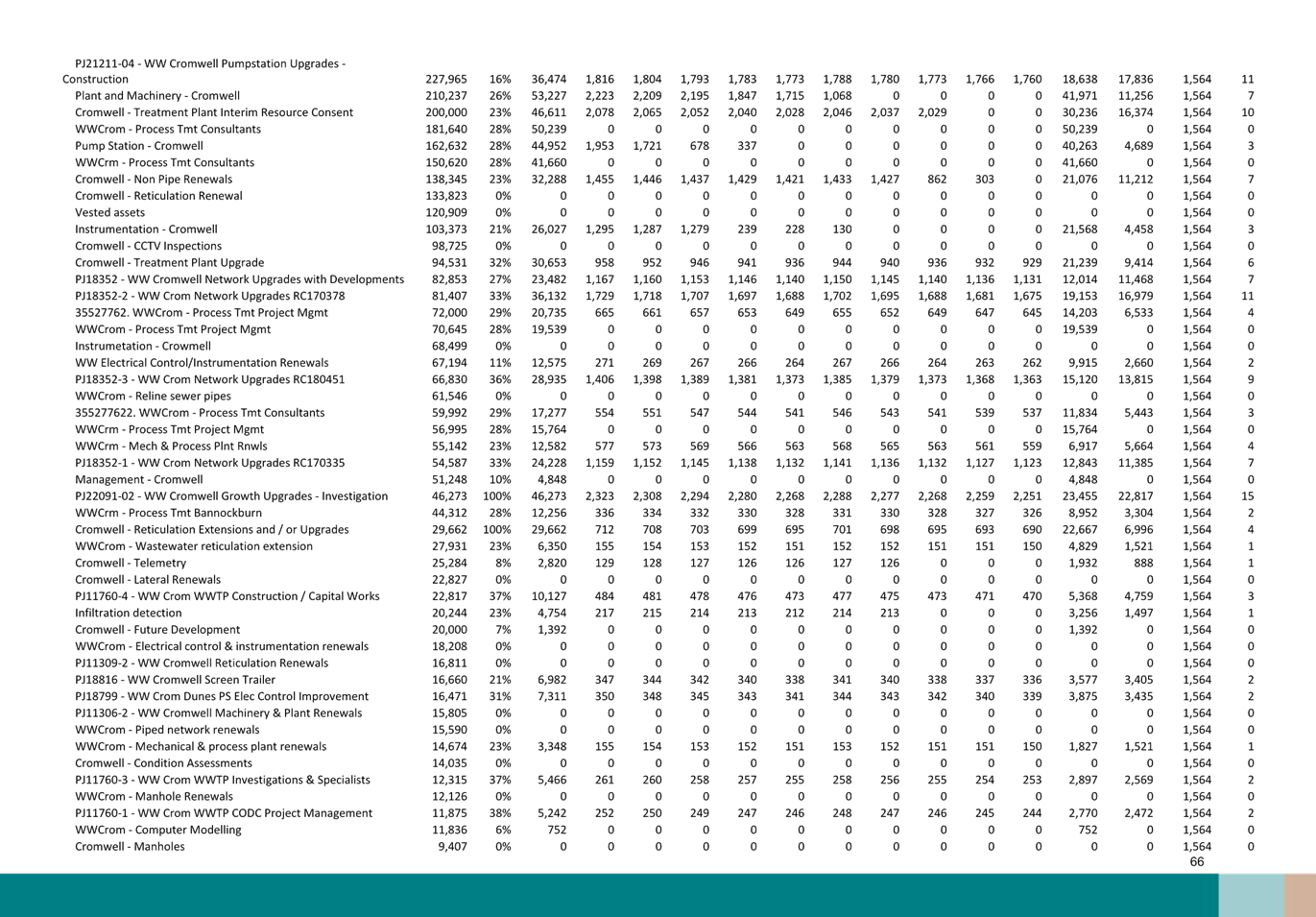

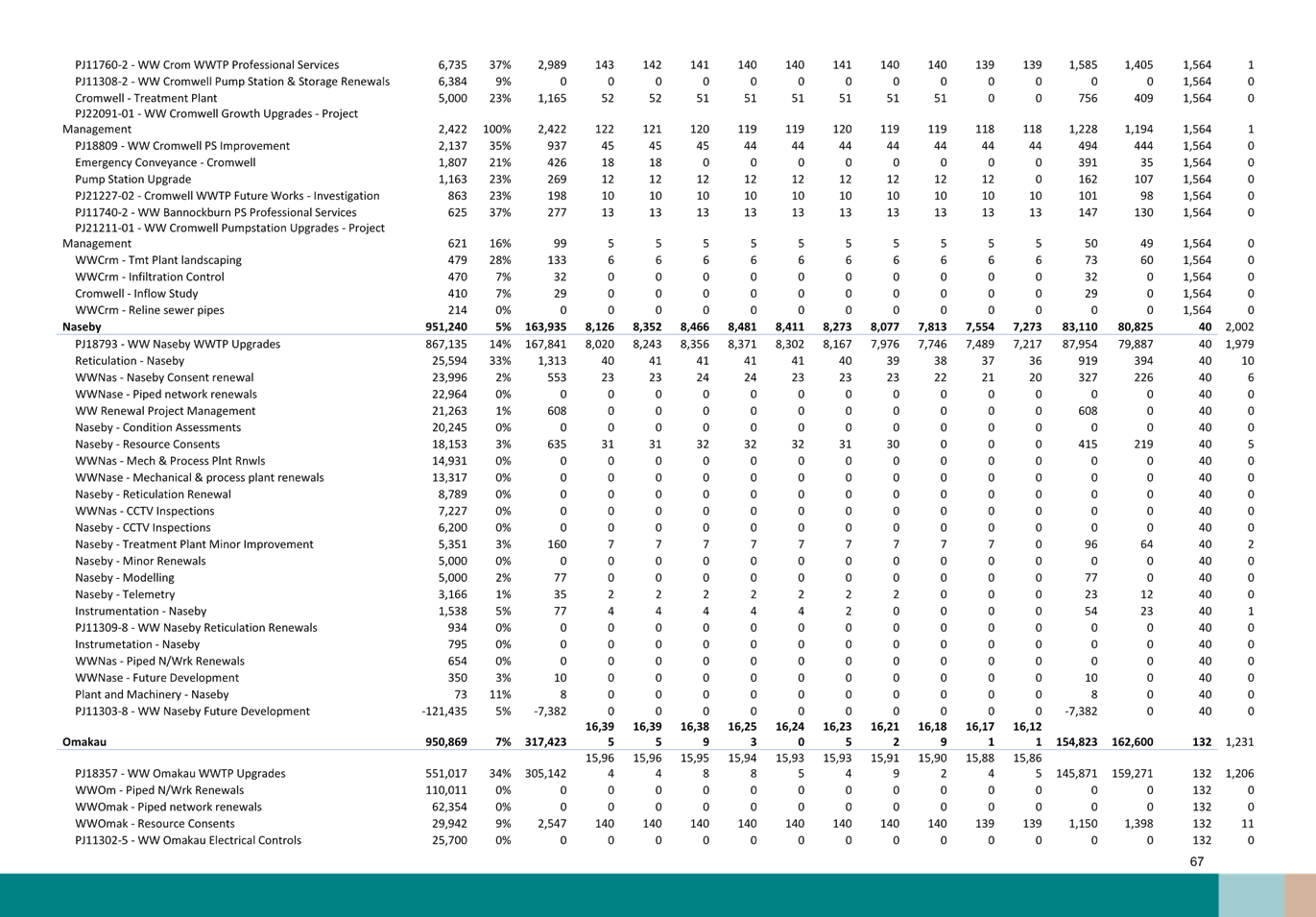

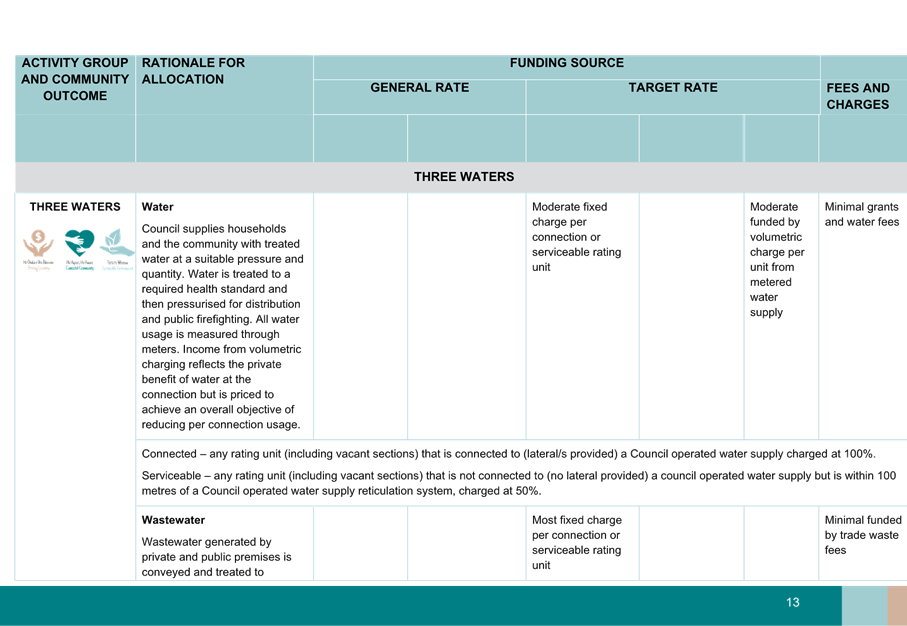

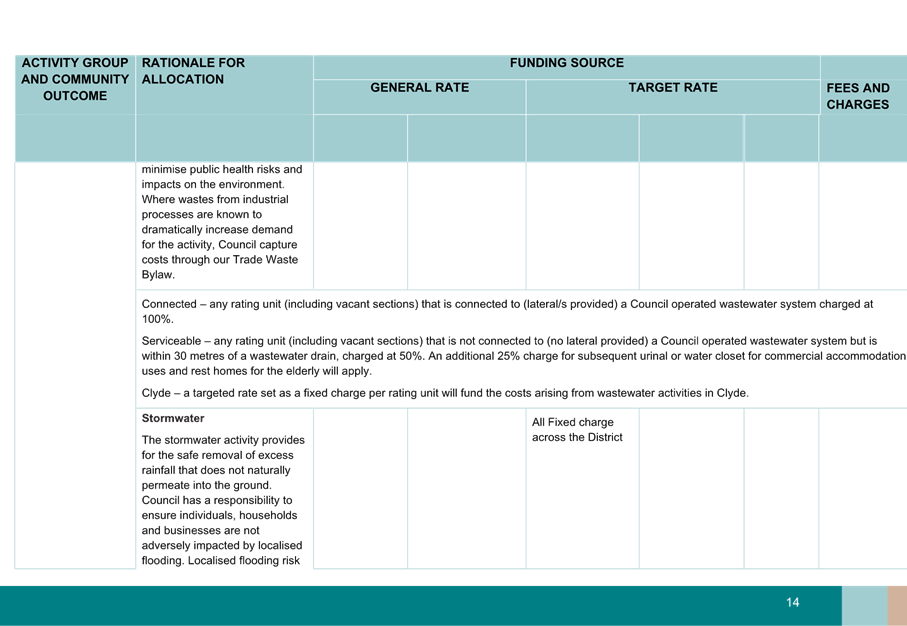

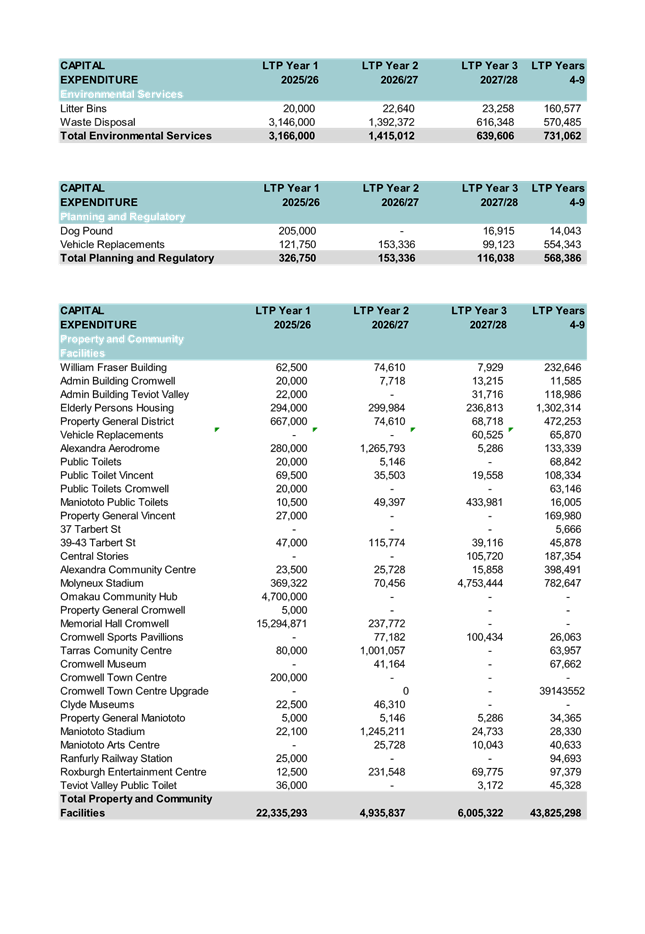

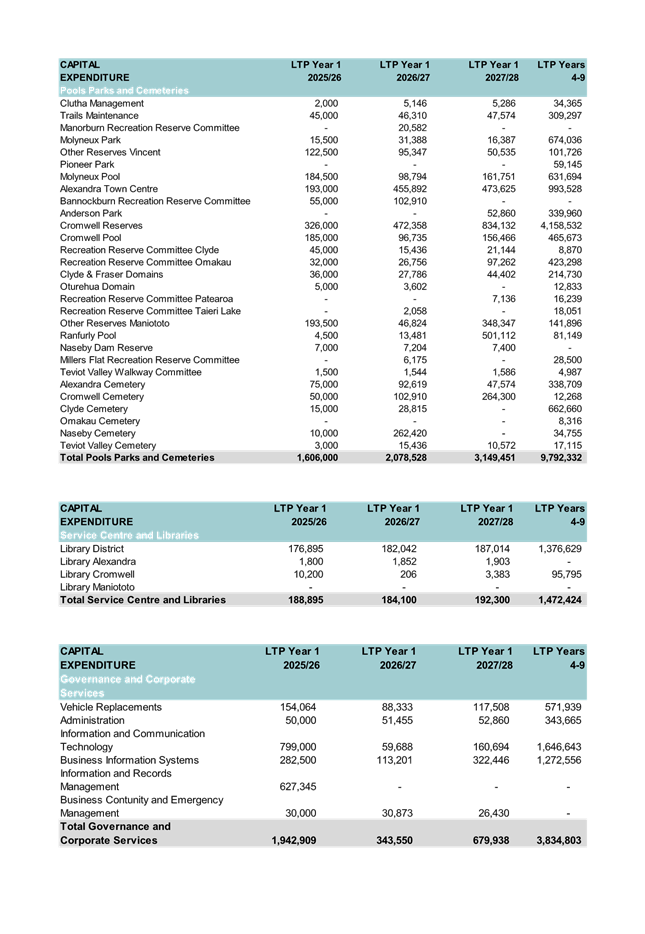

(m) Capital

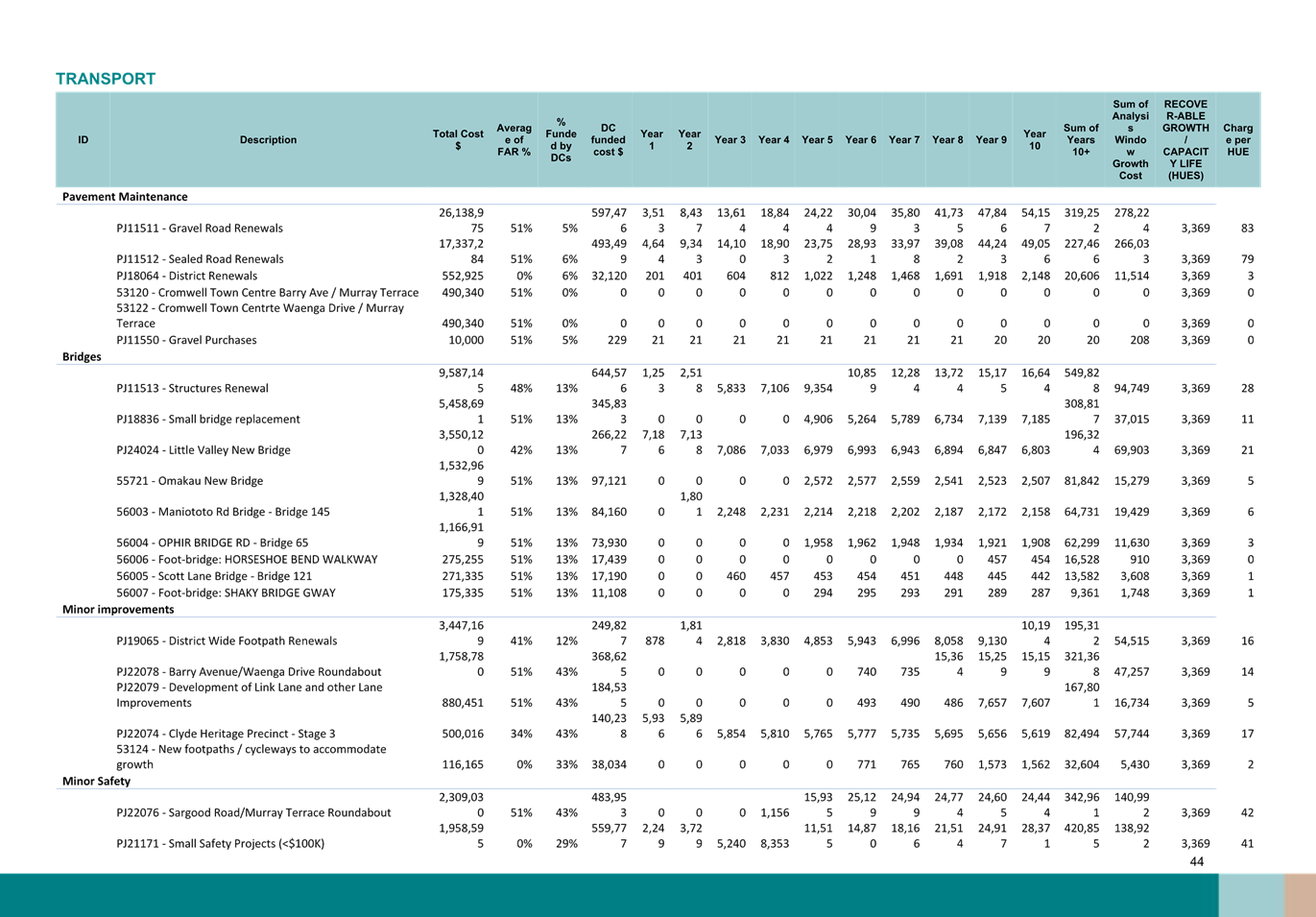

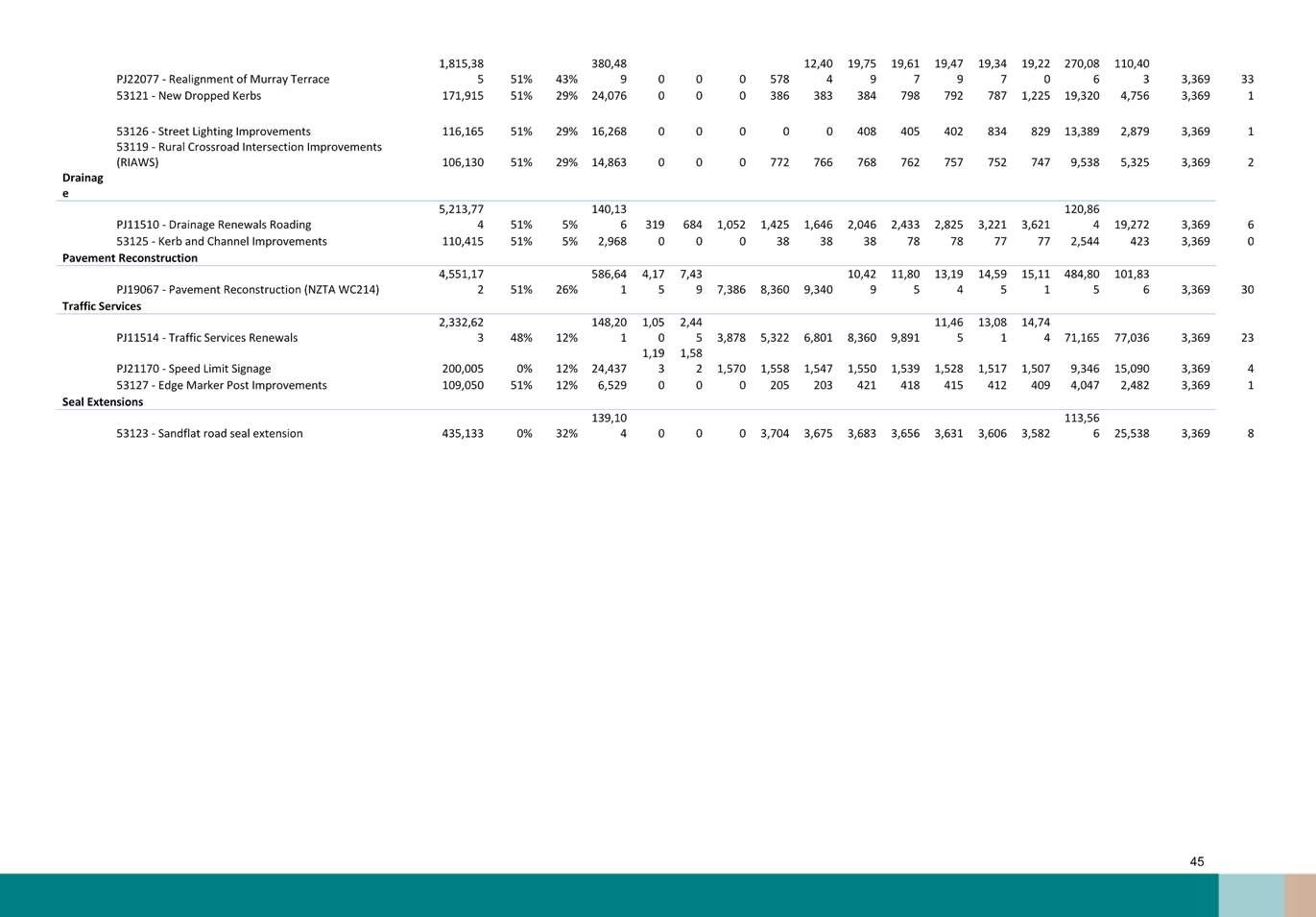

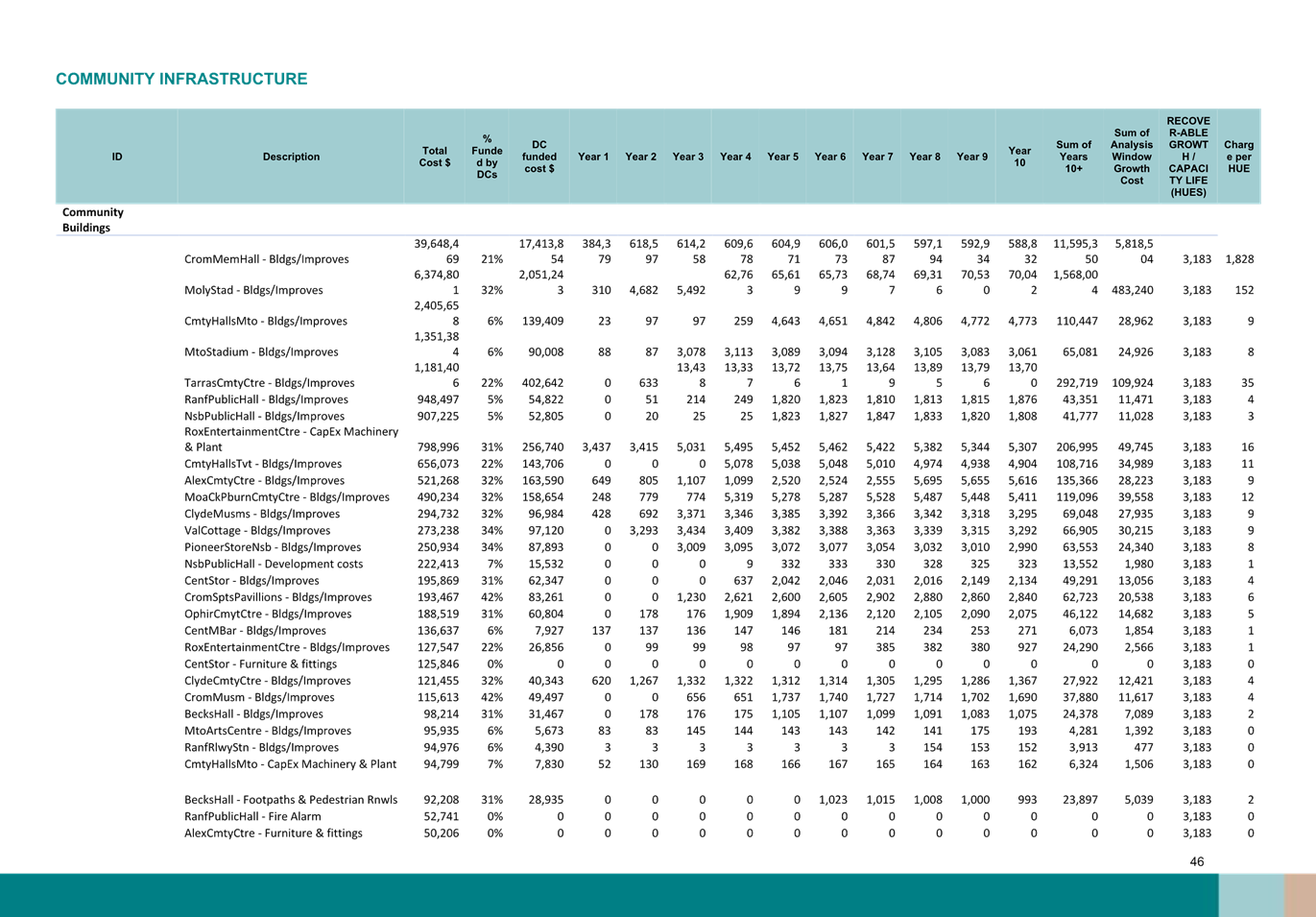

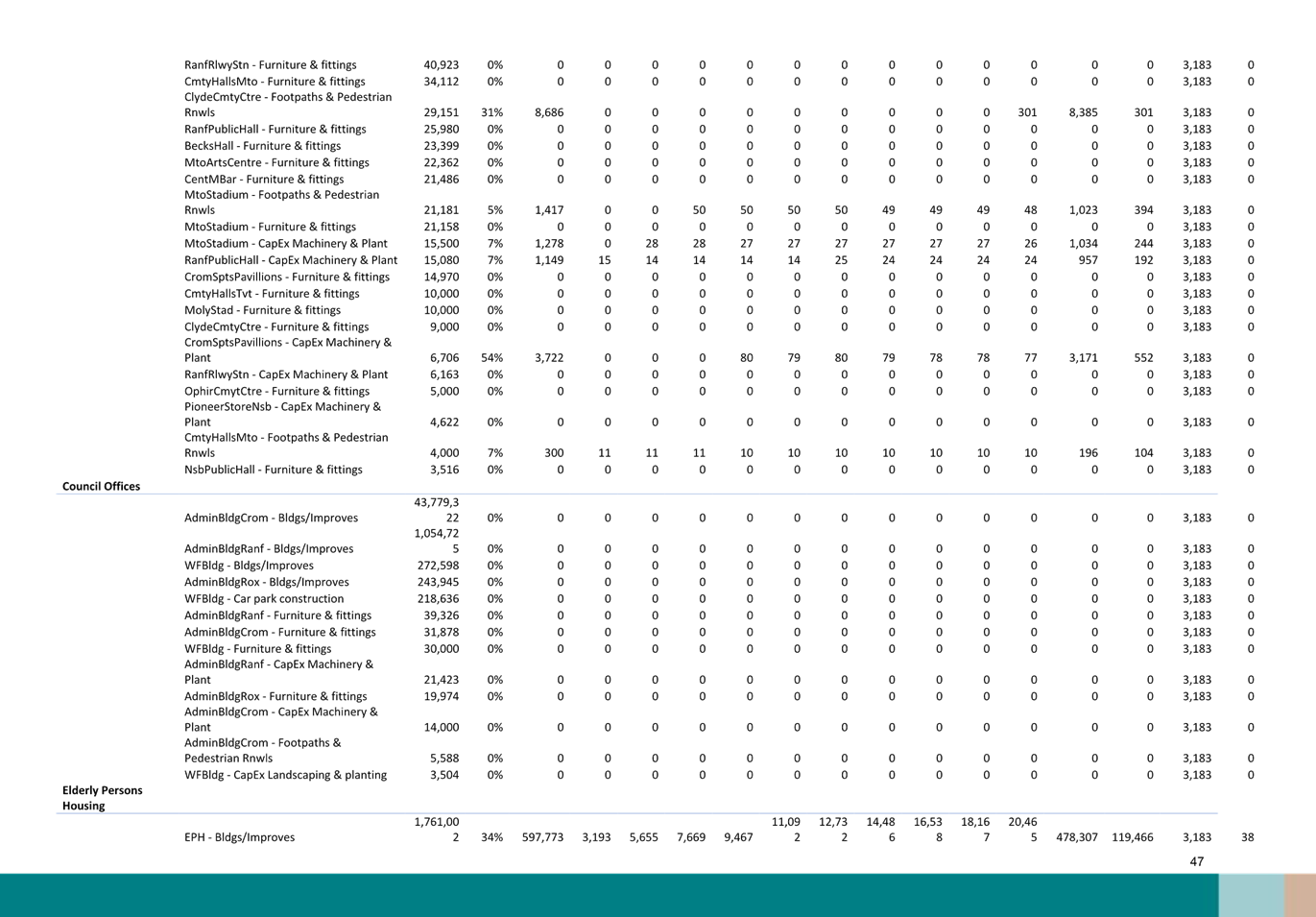

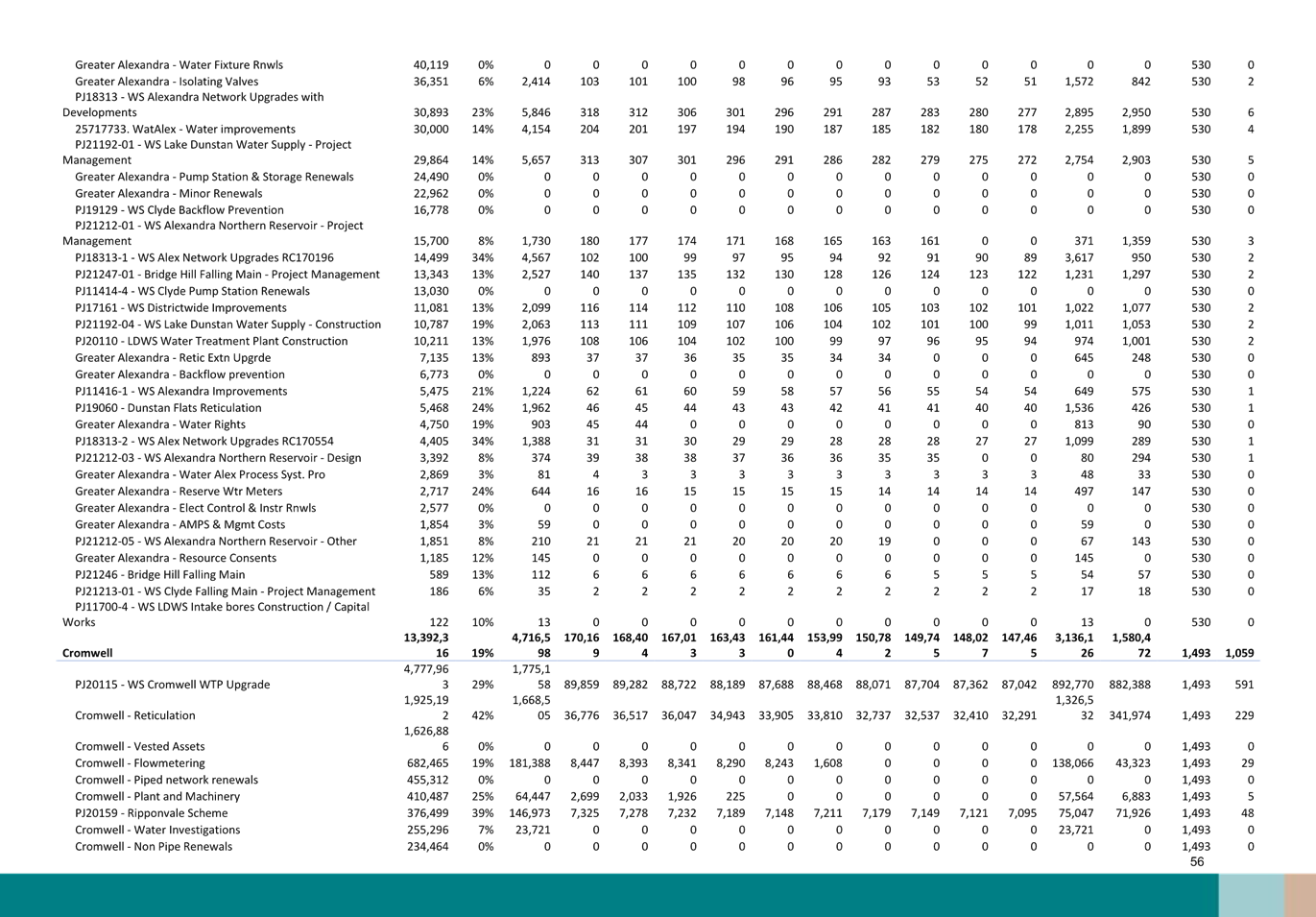

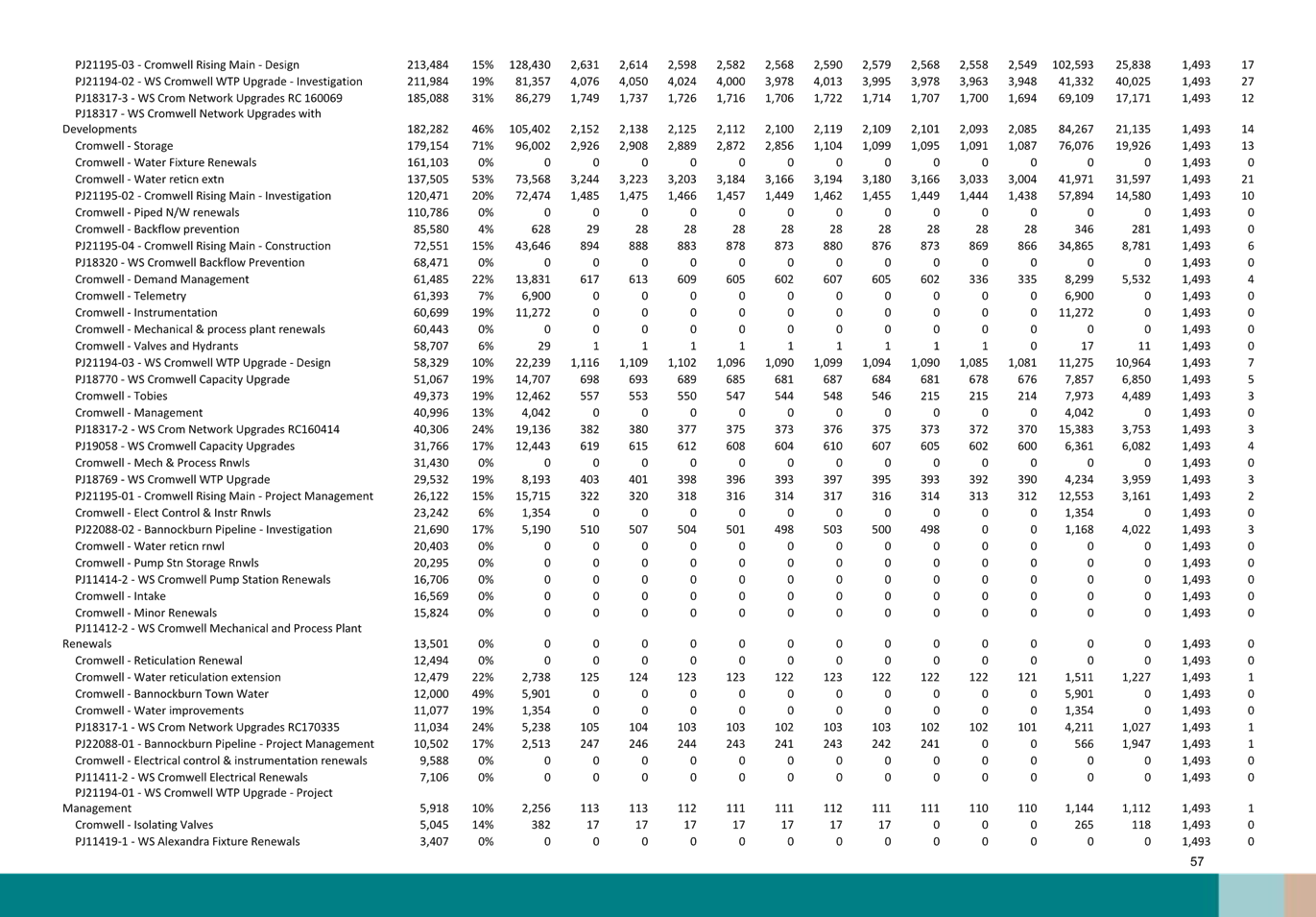

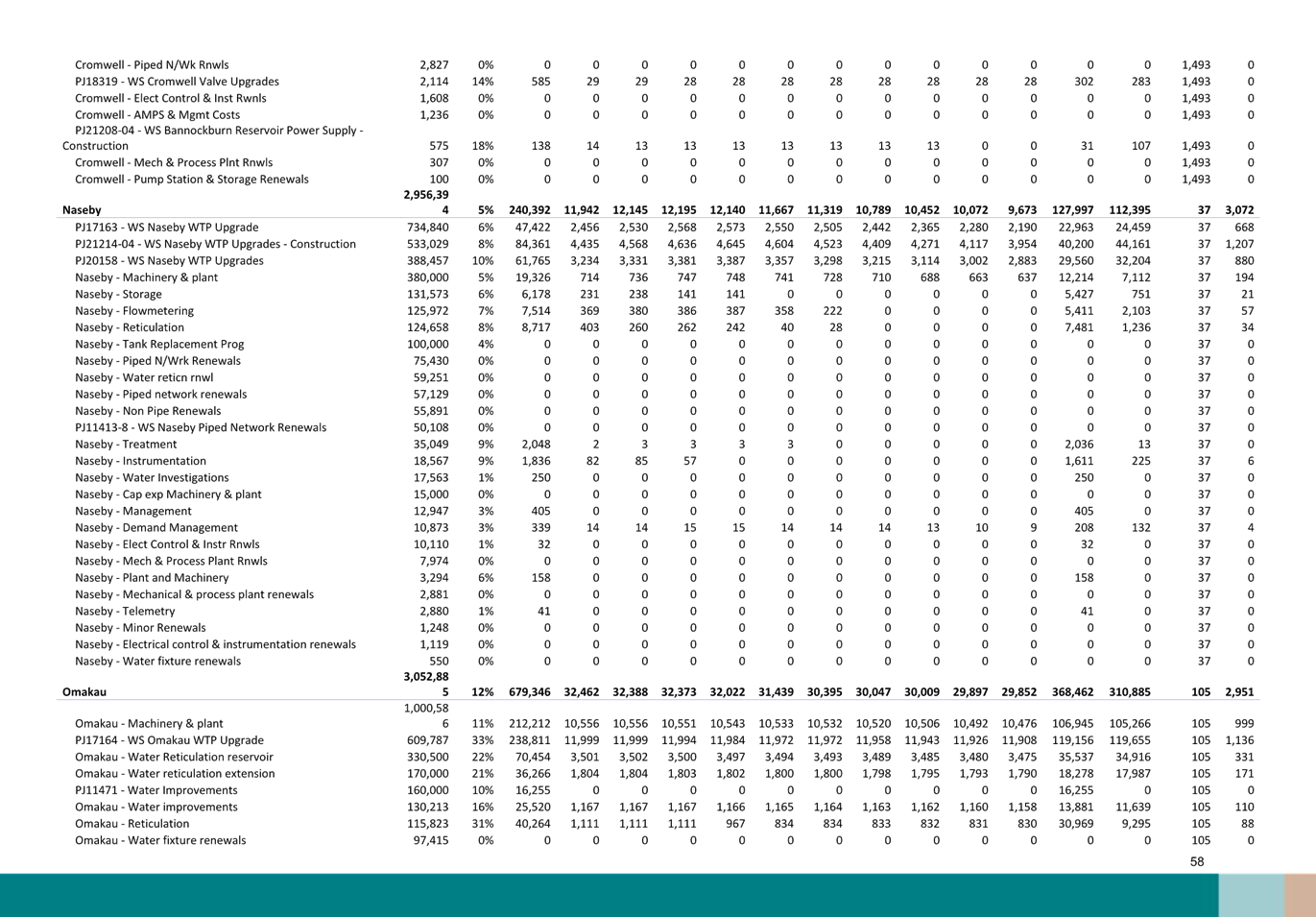

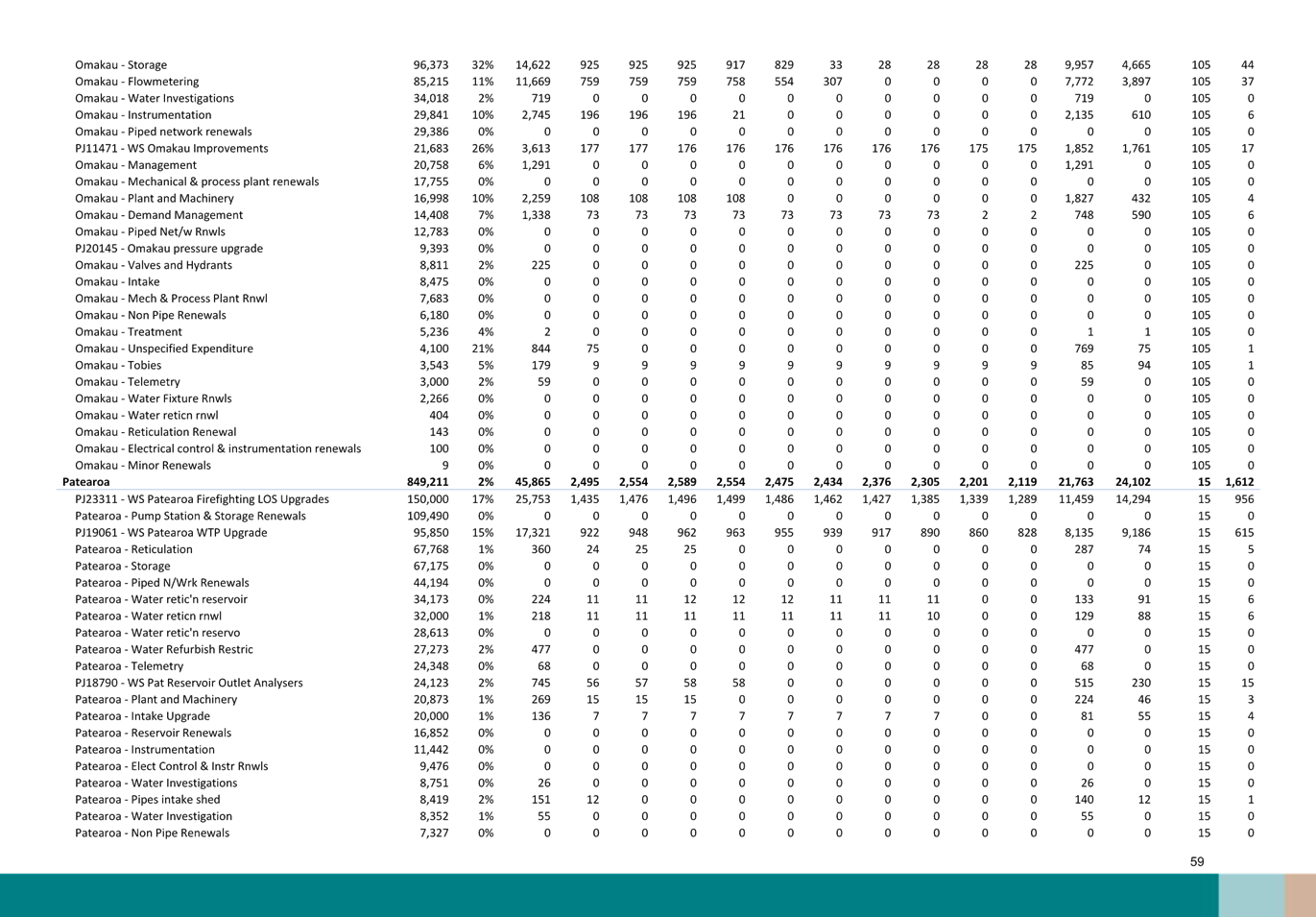

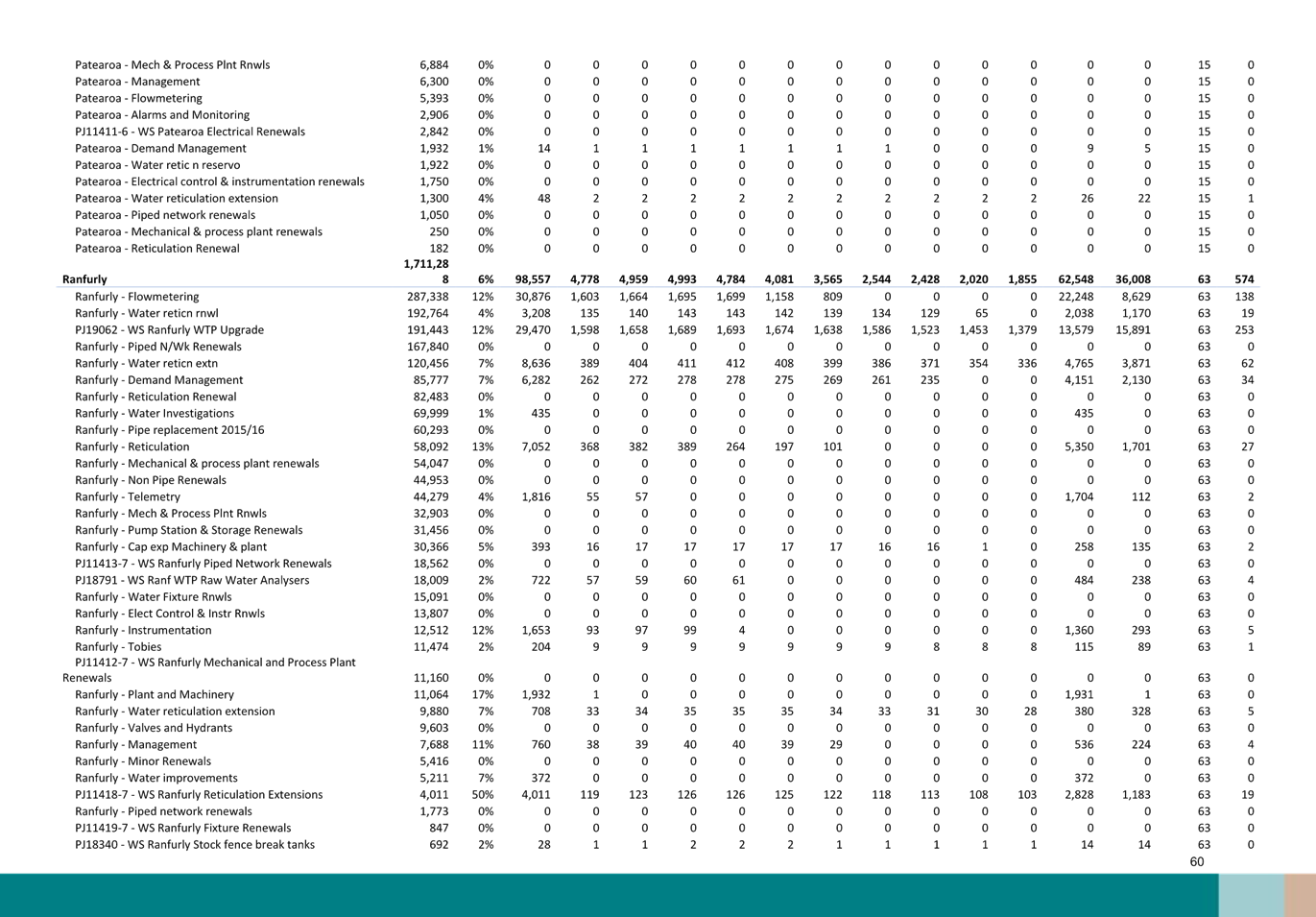

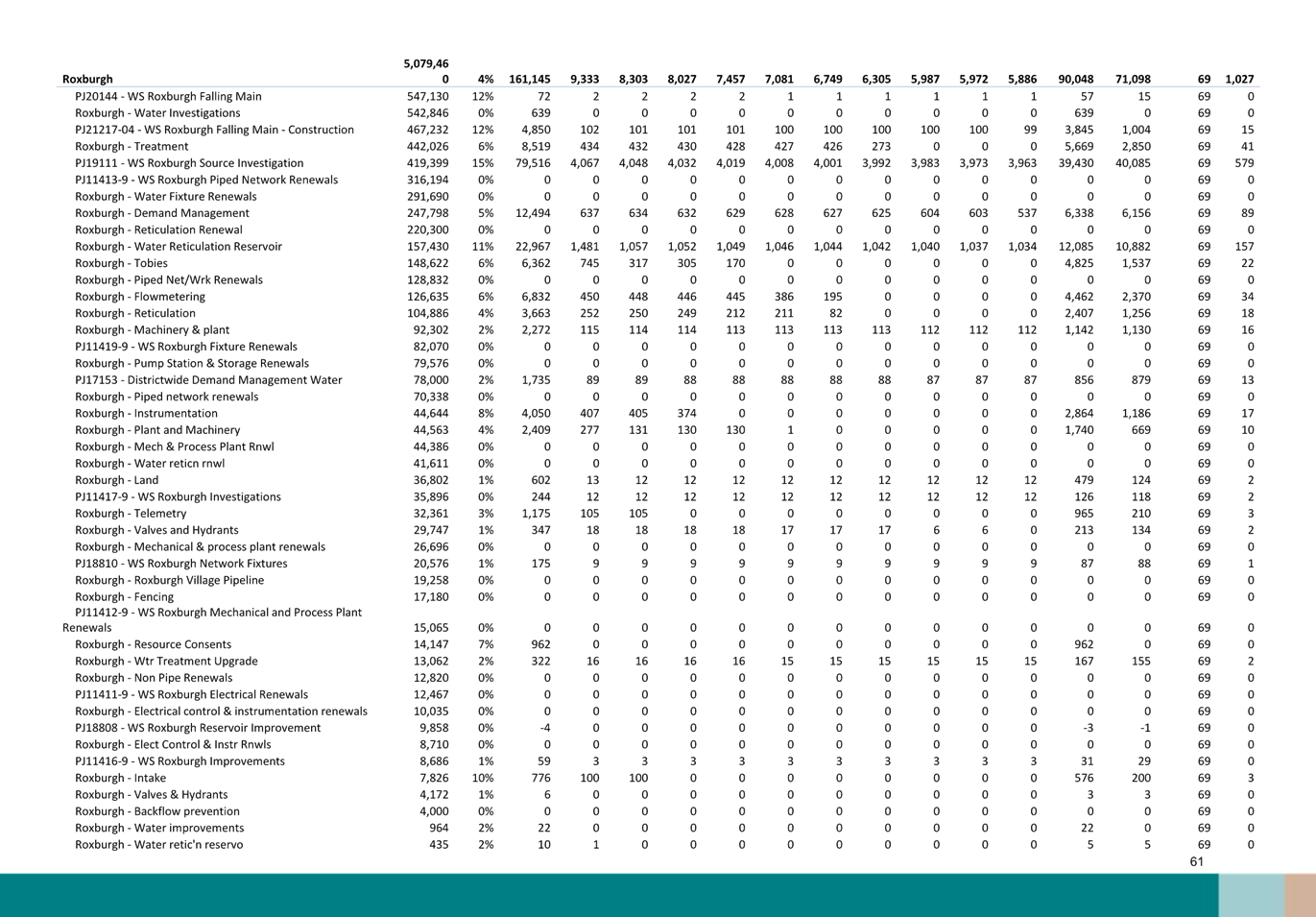

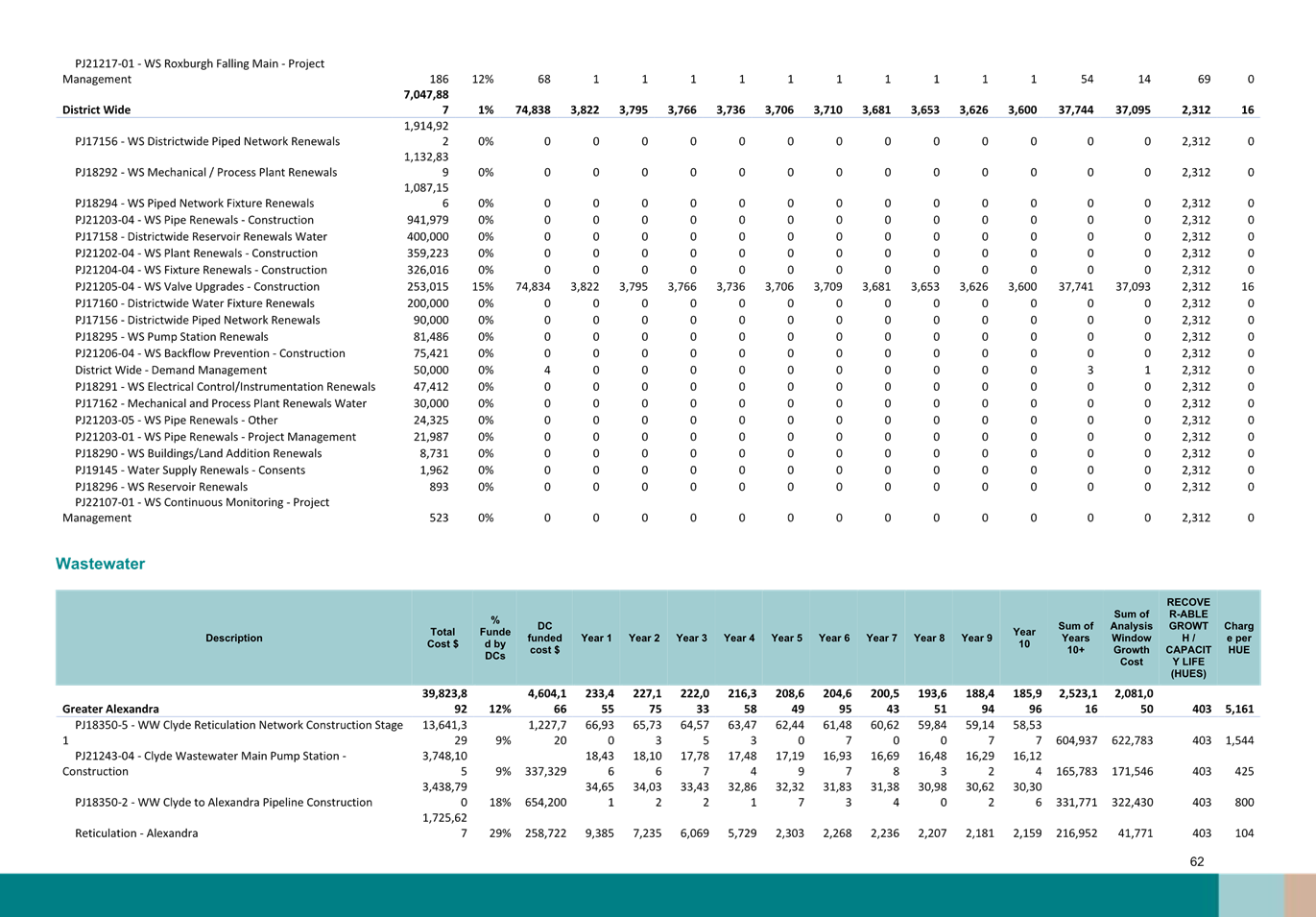

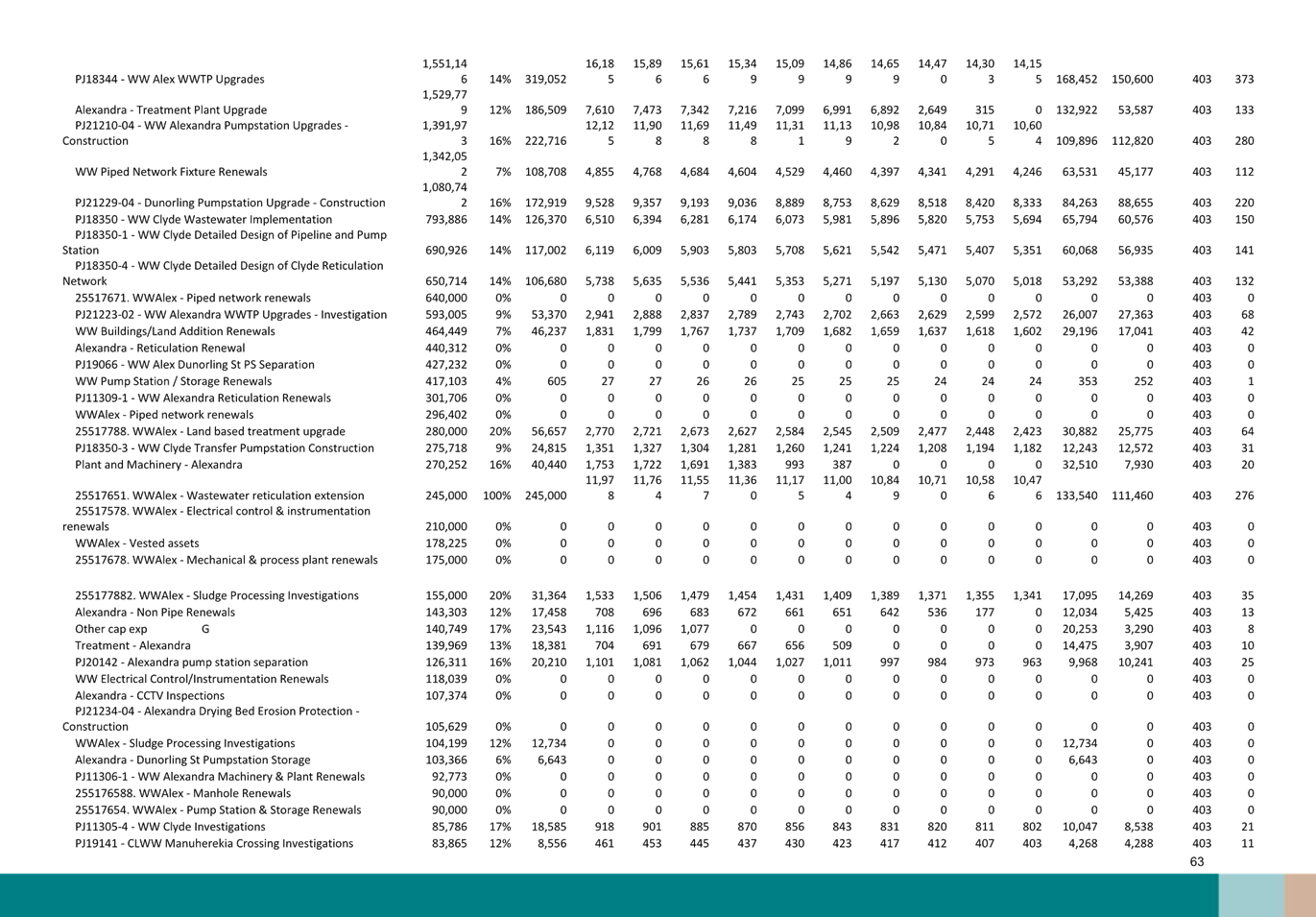

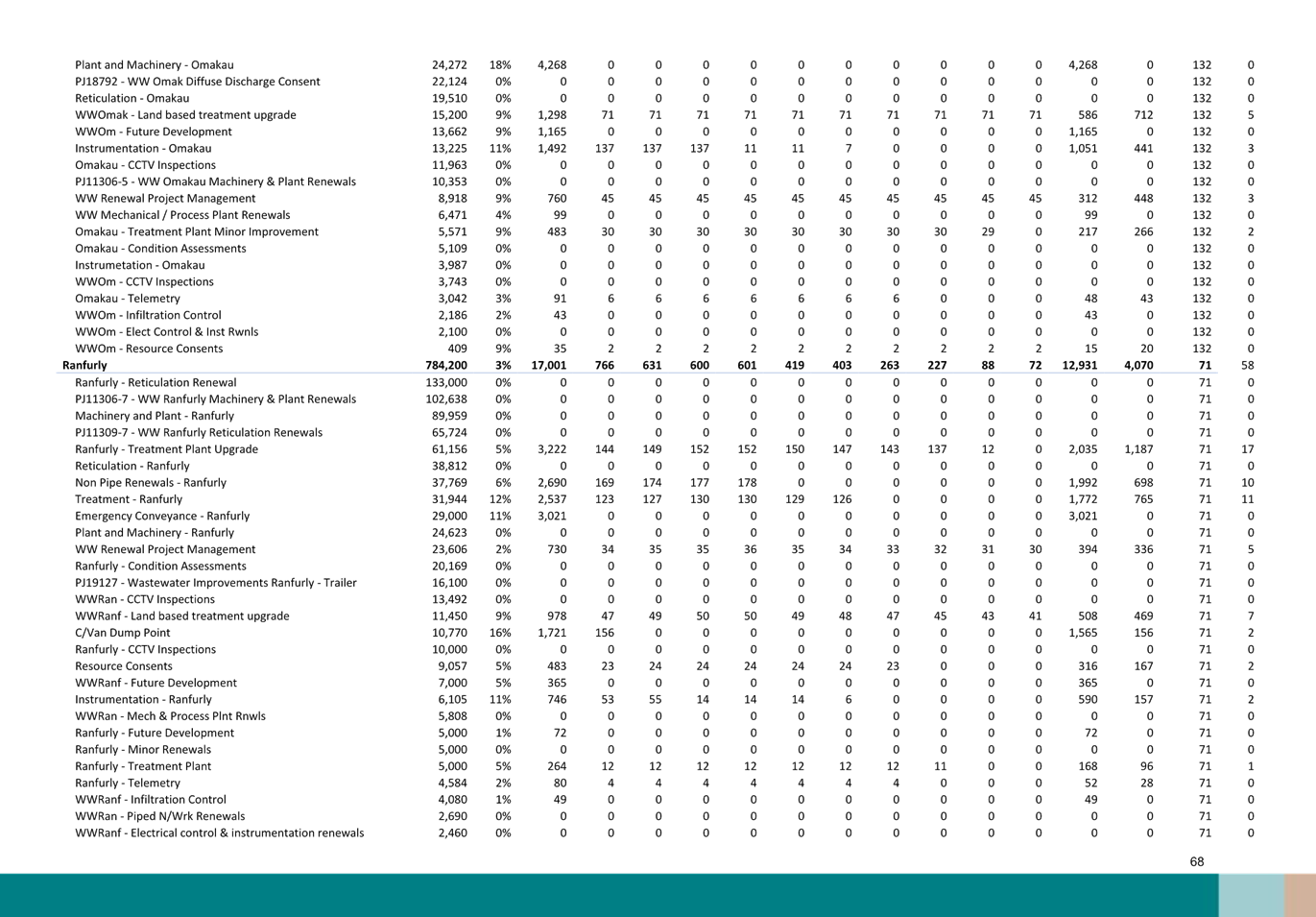

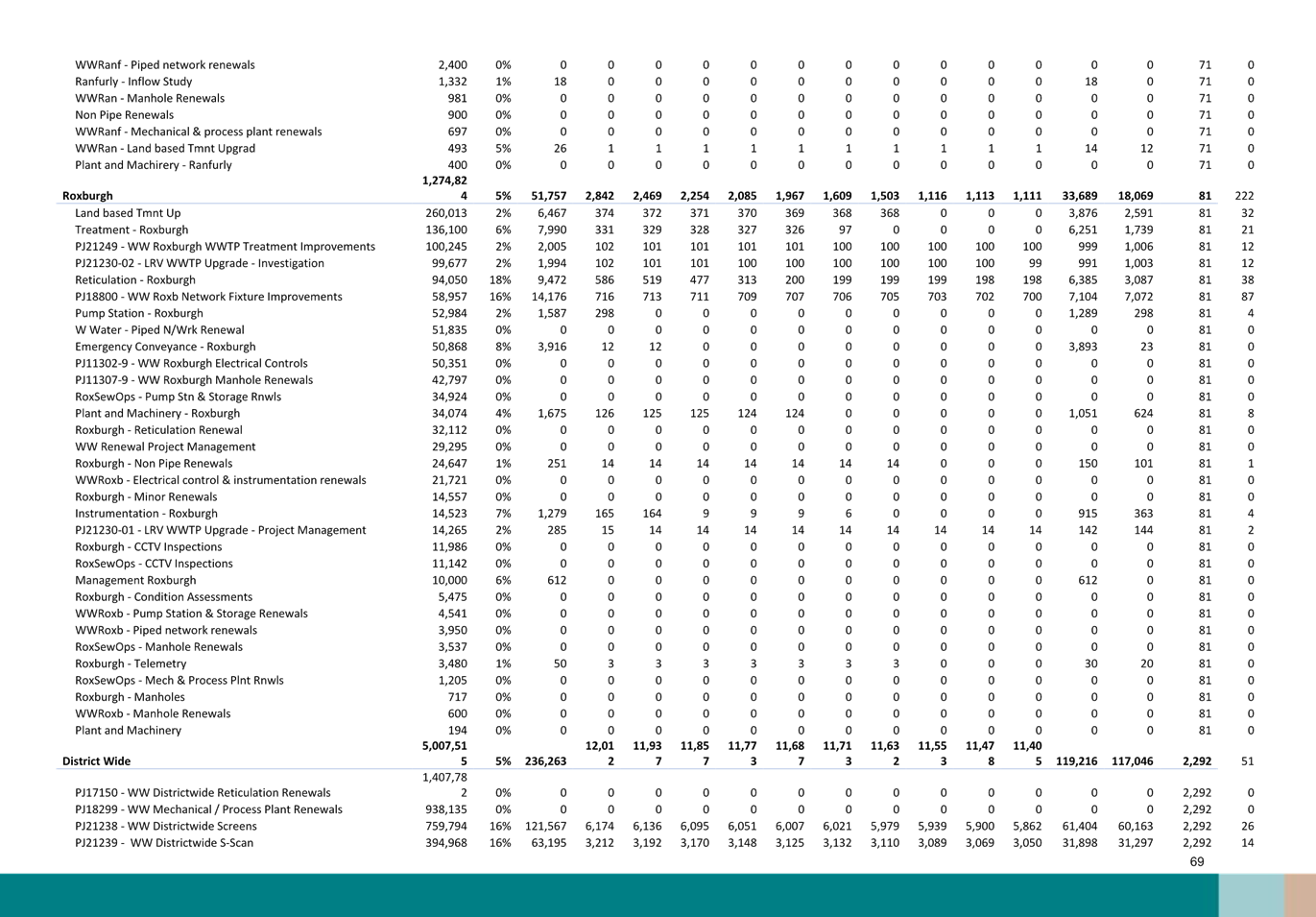

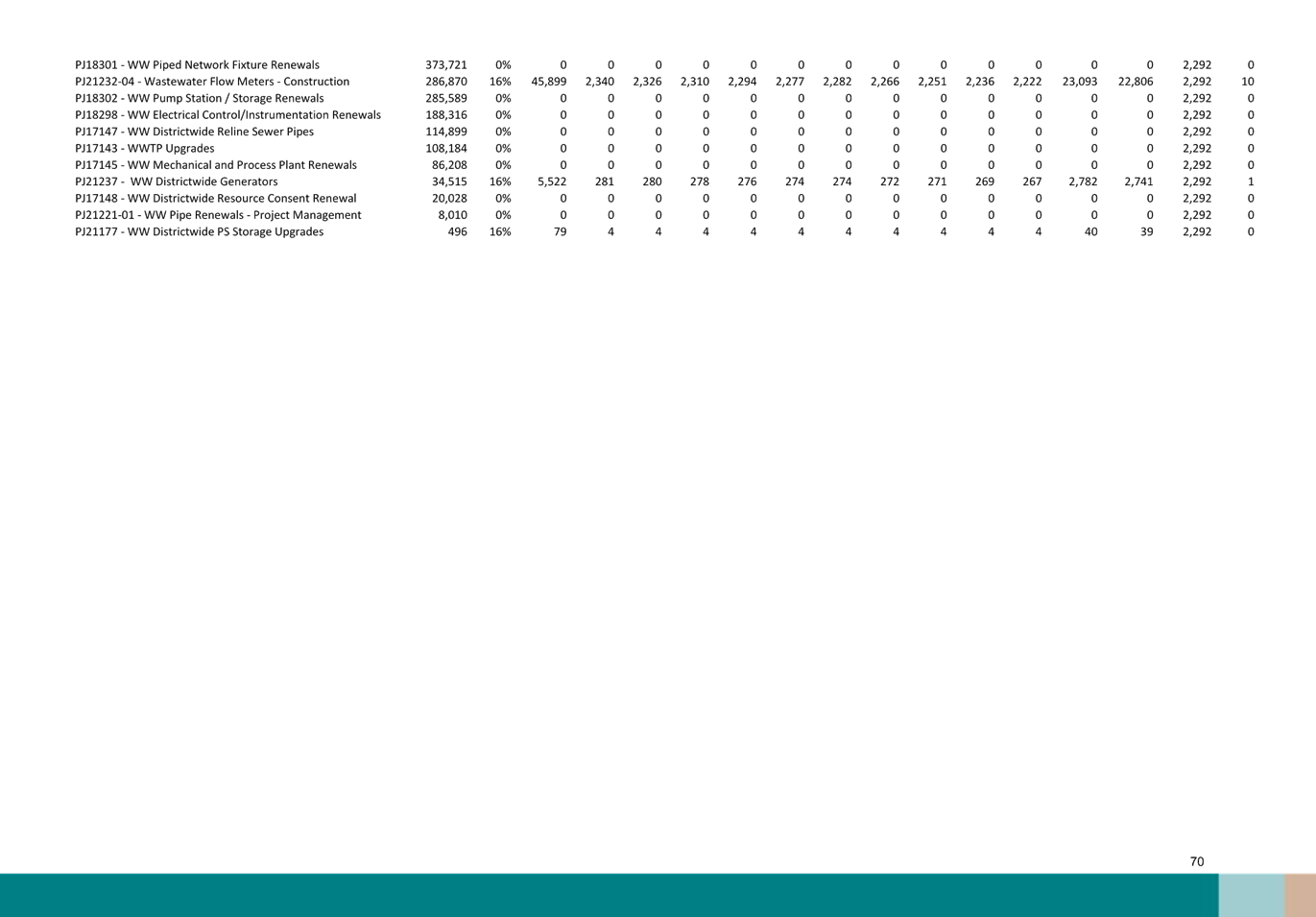

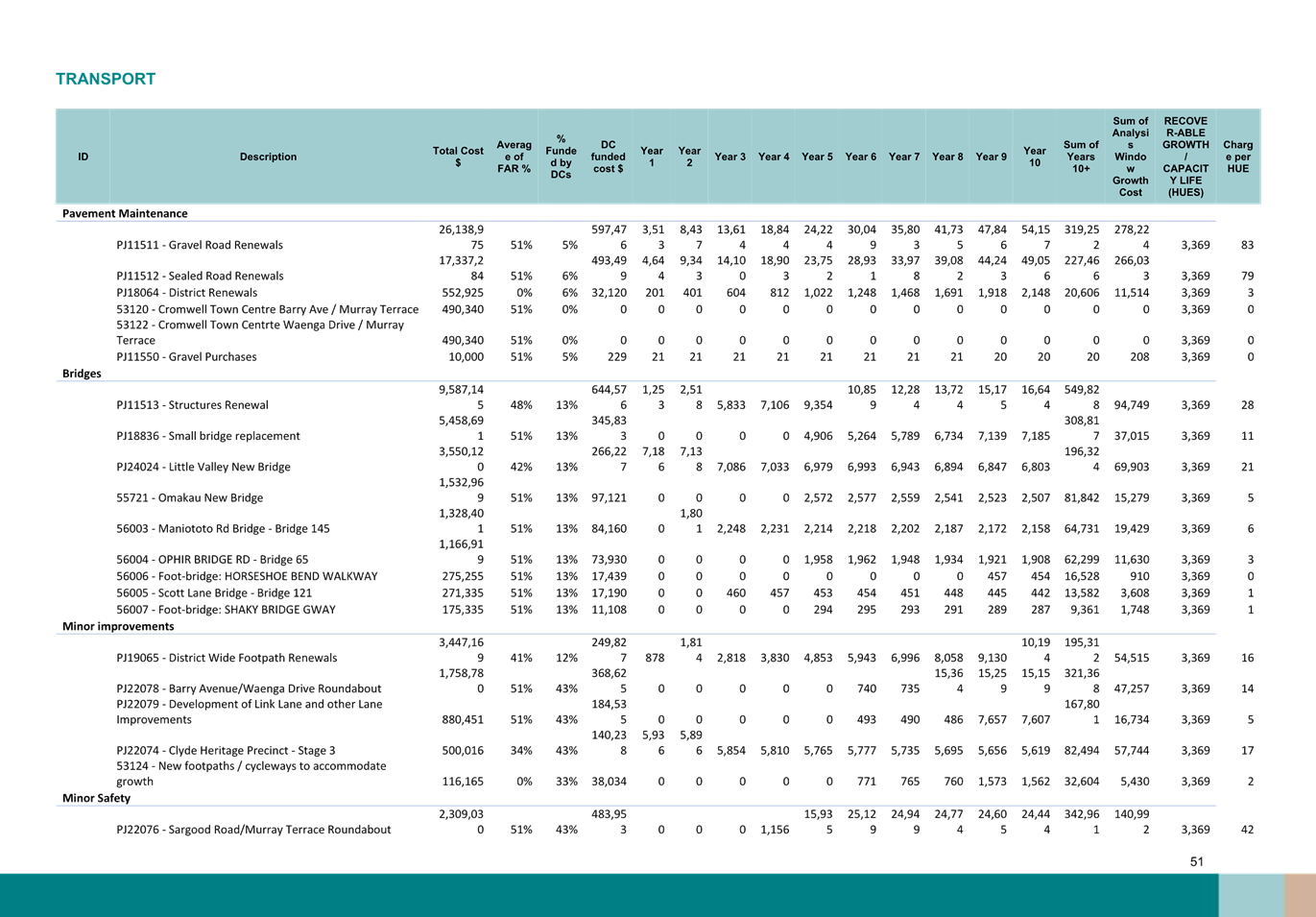

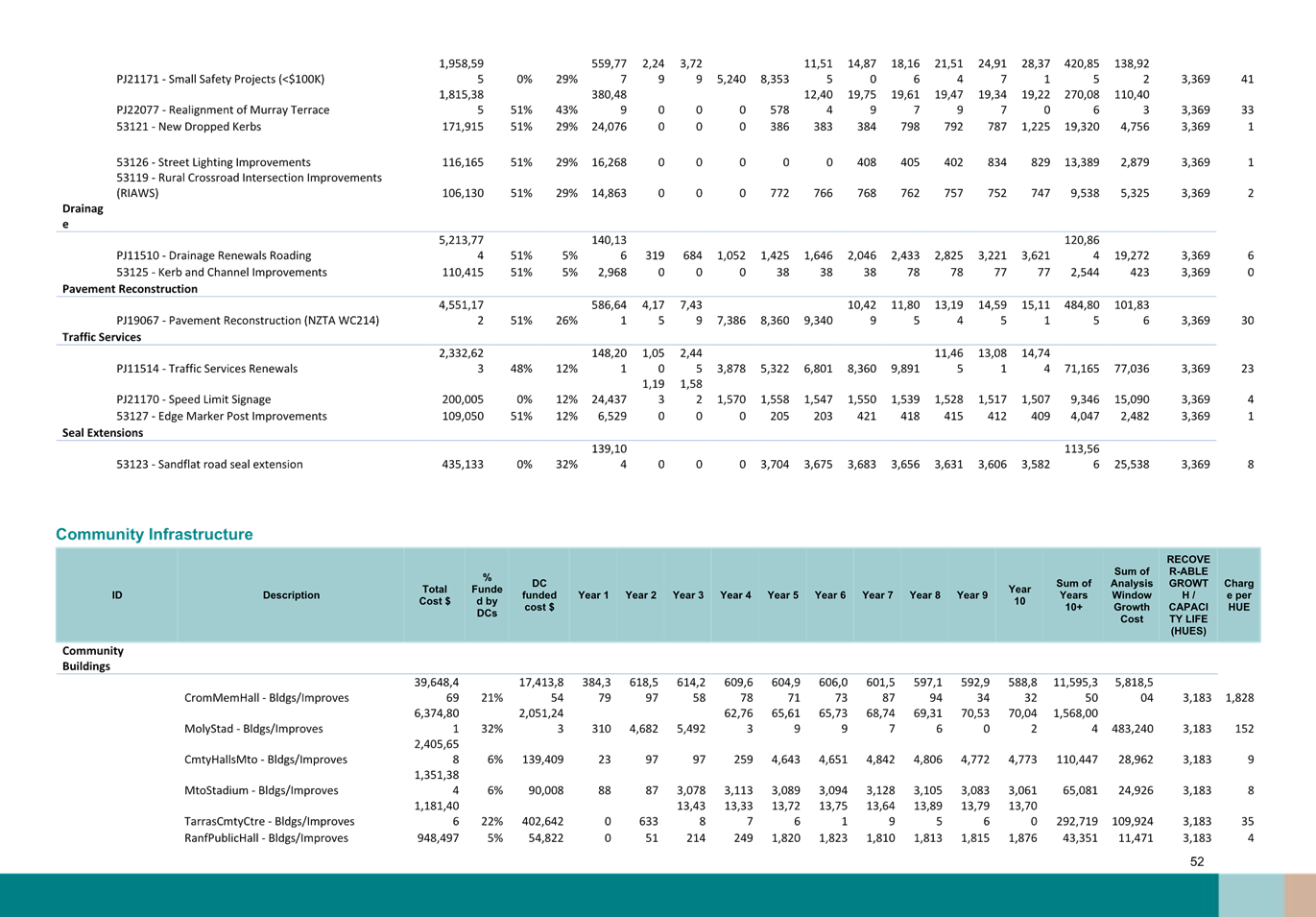

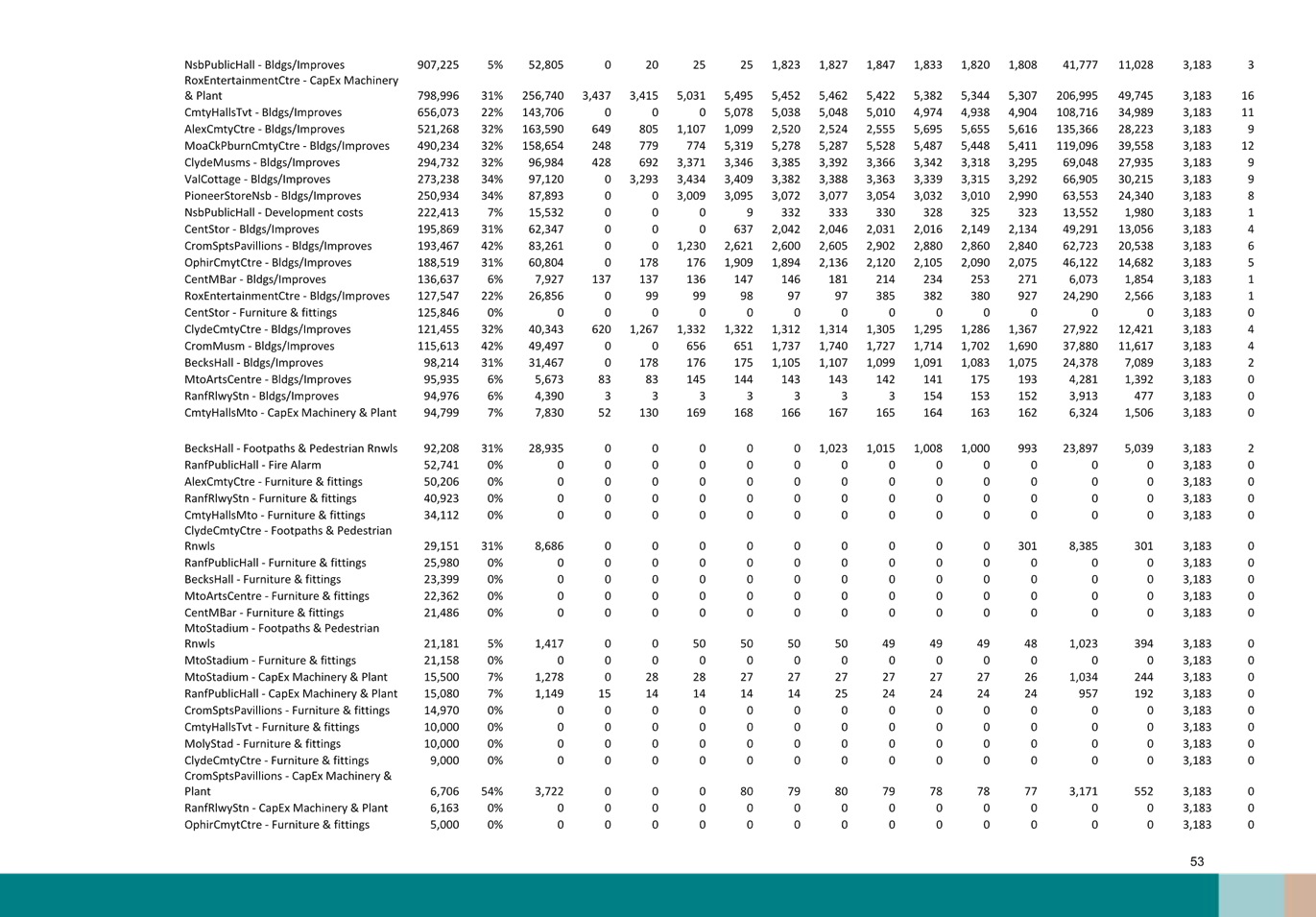

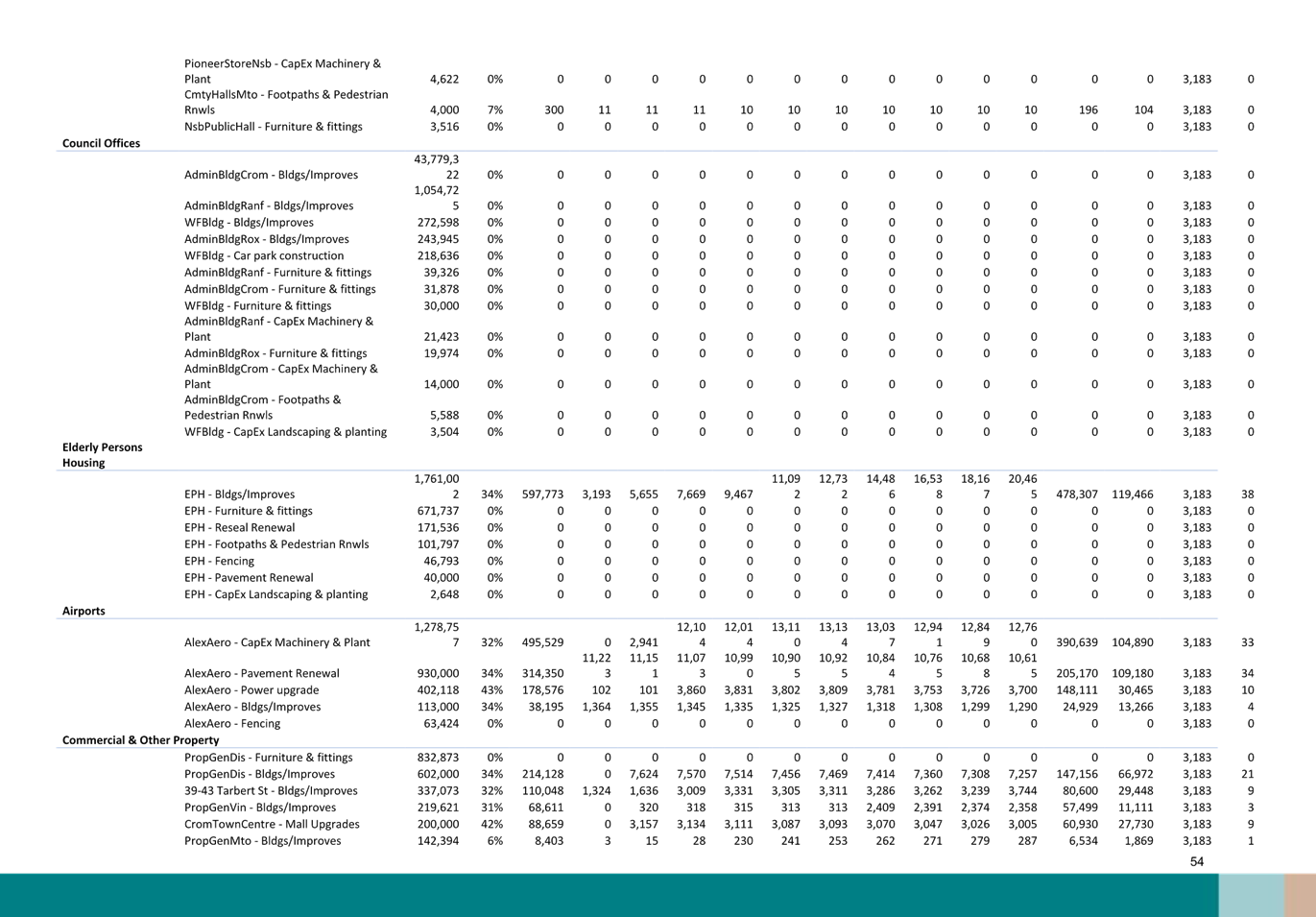

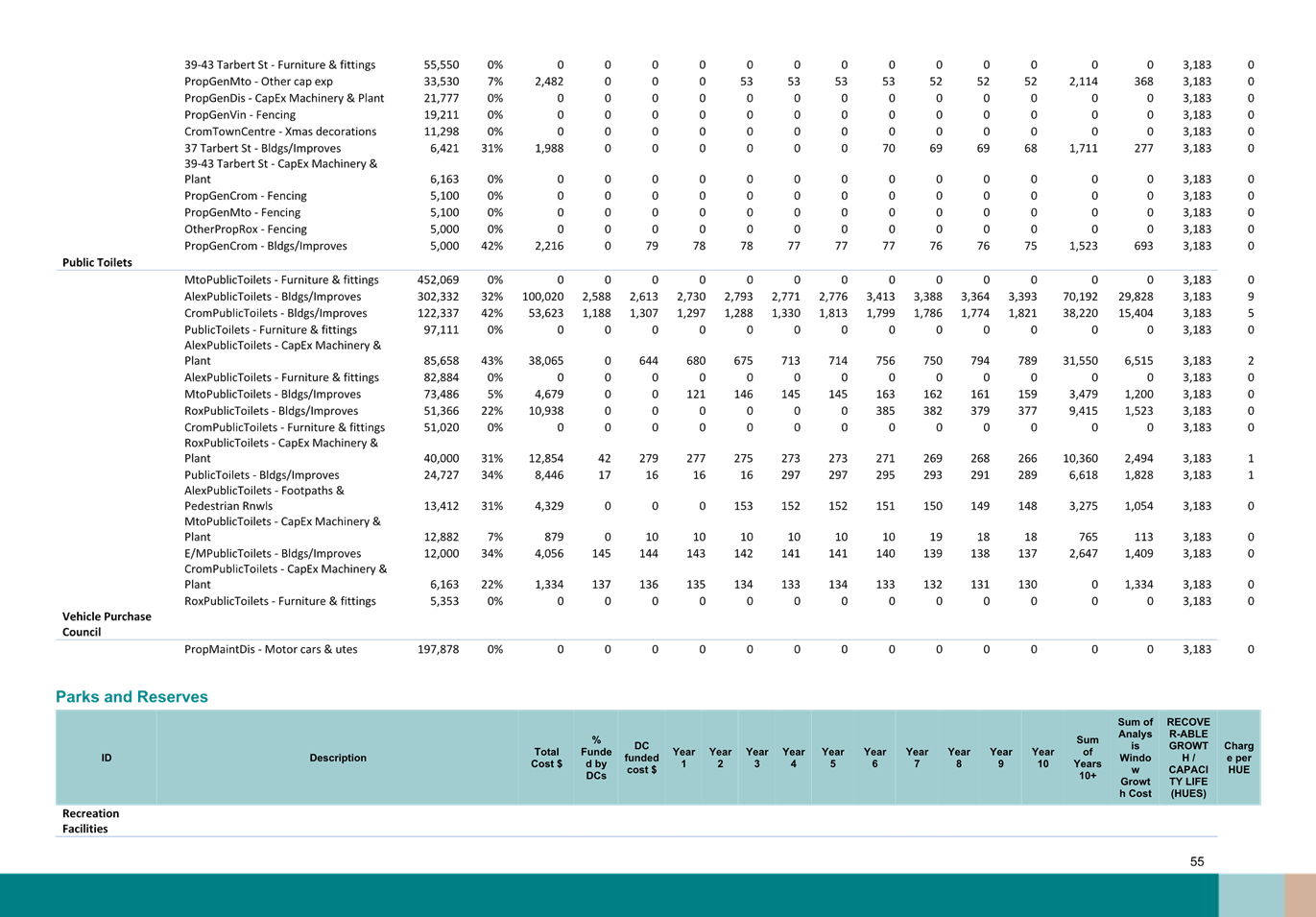

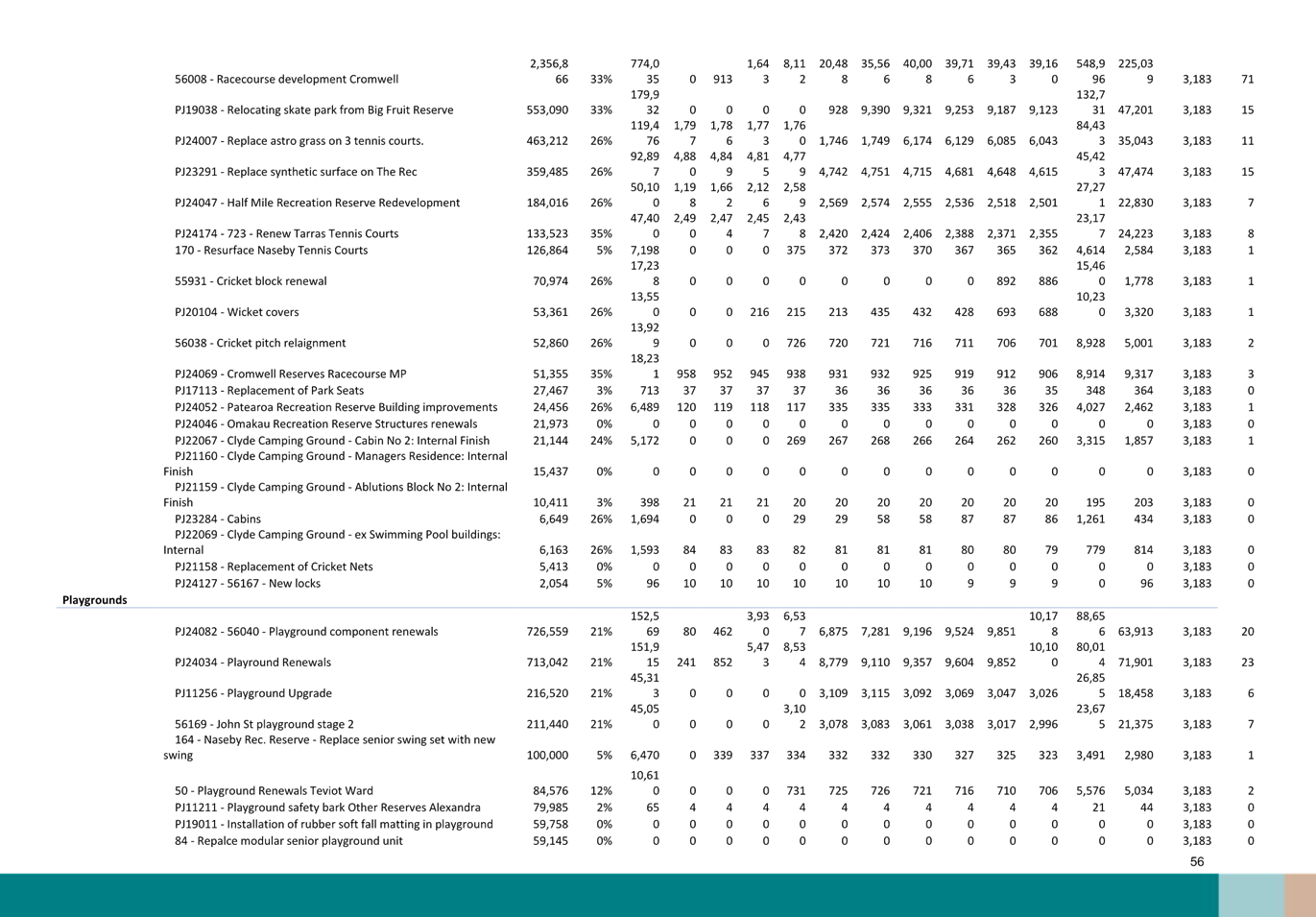

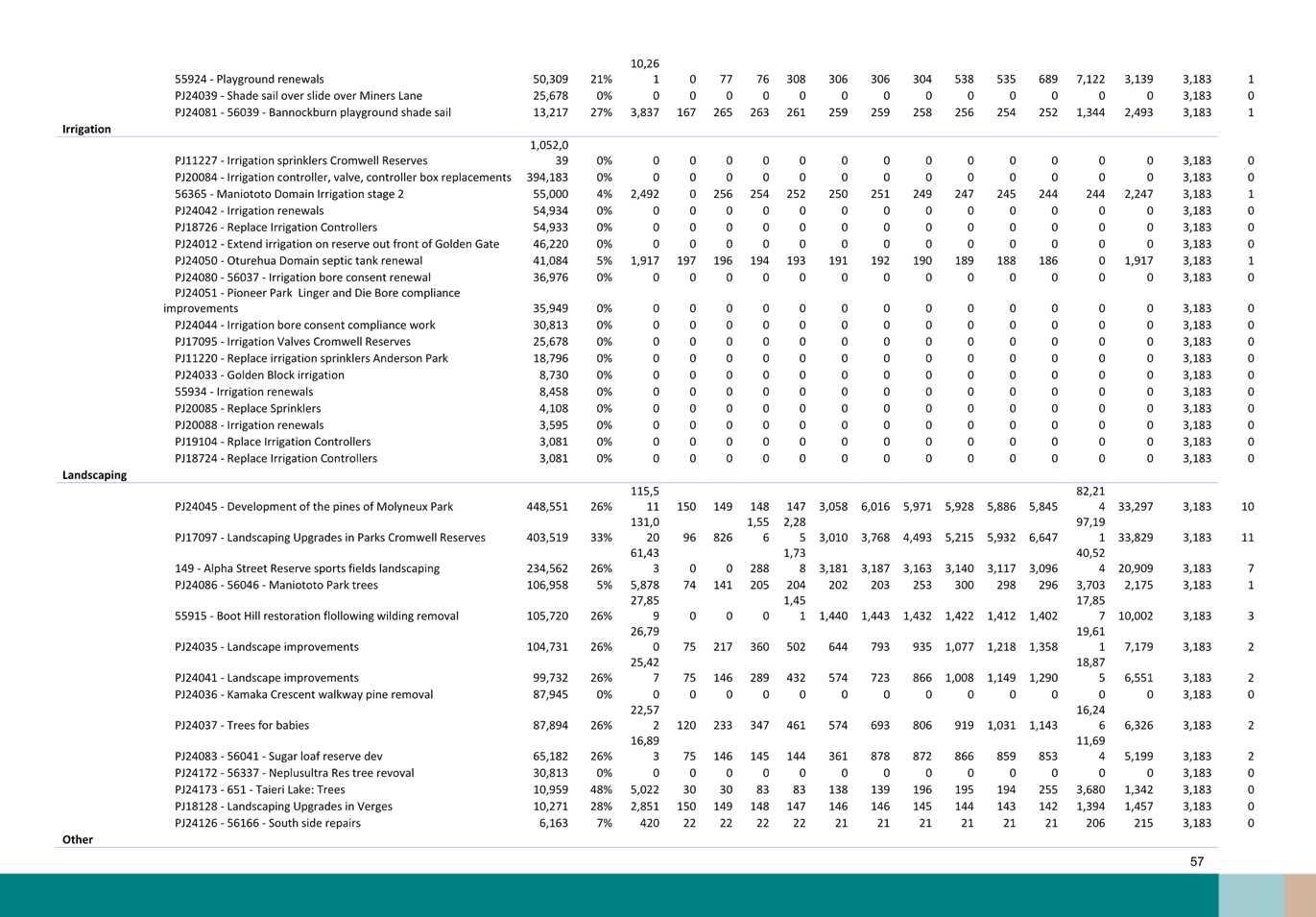

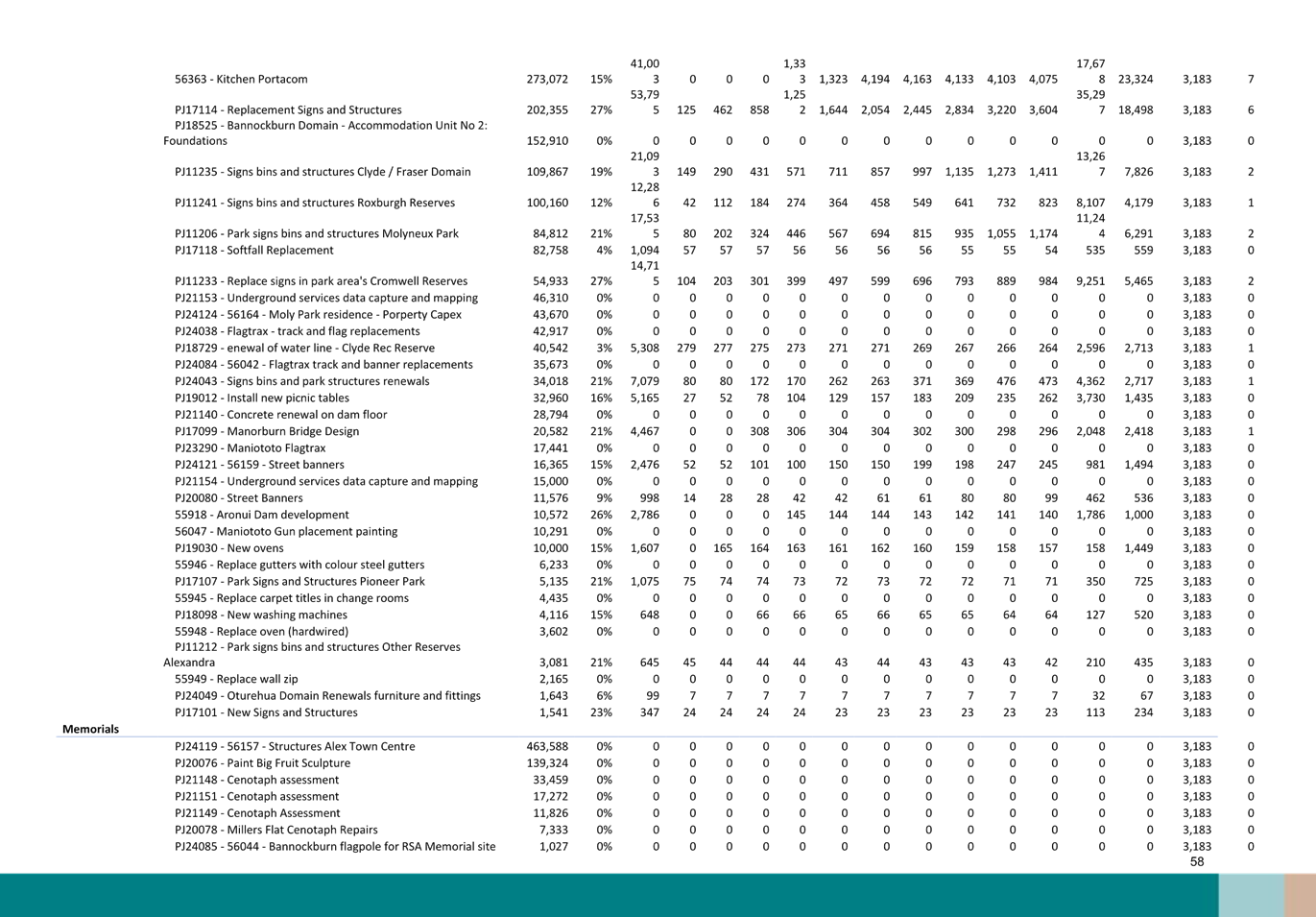

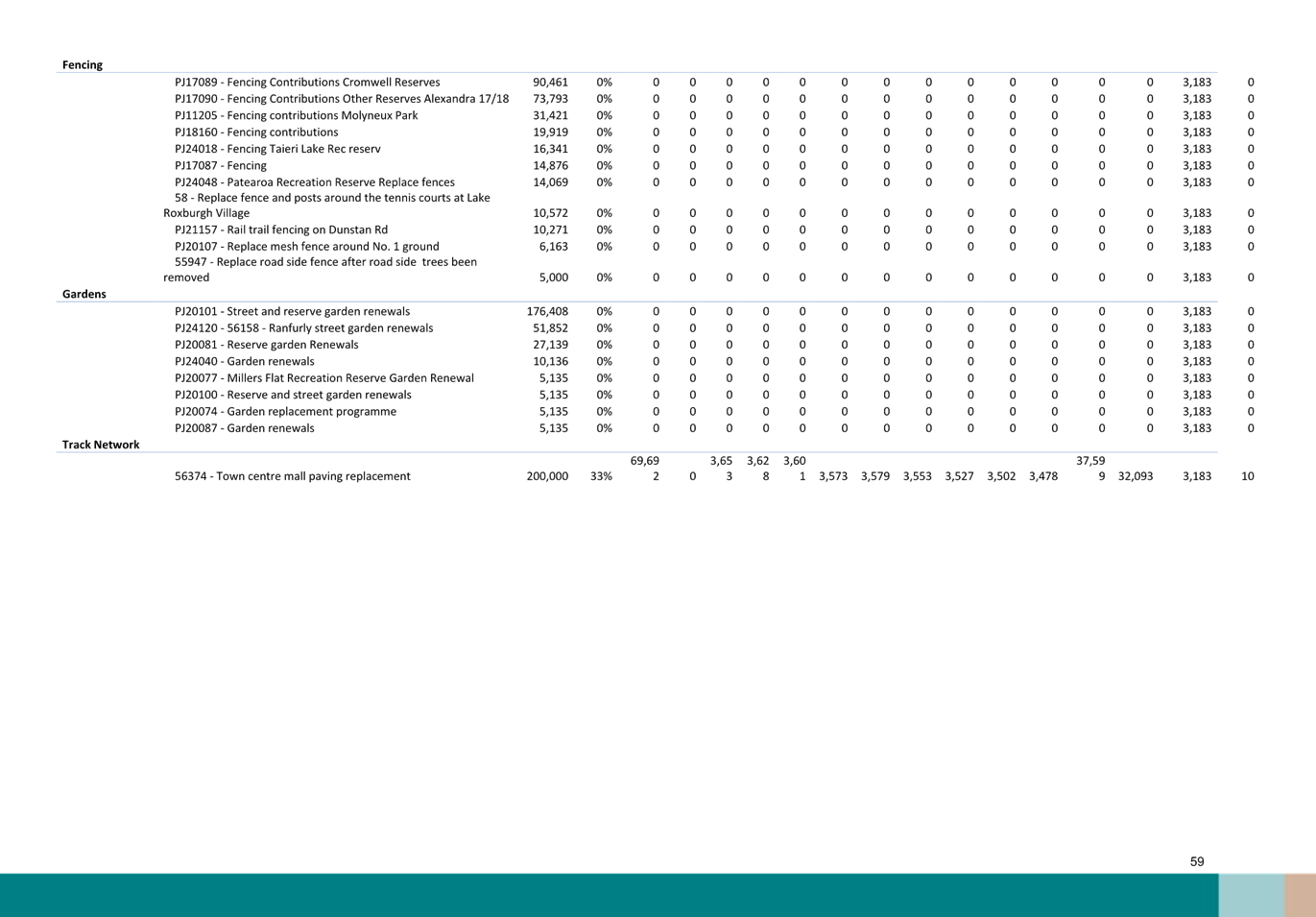

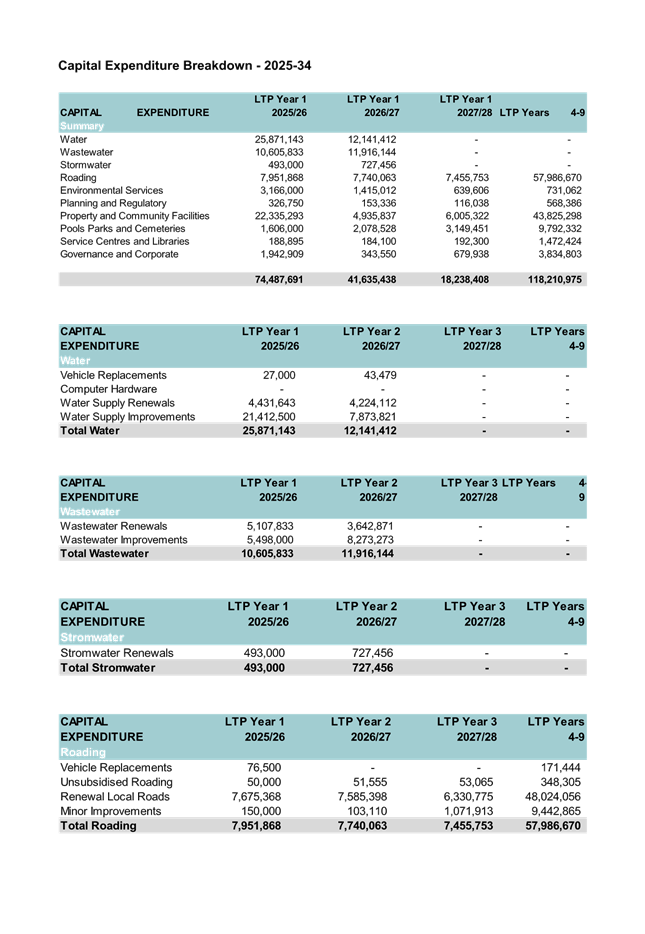

Expenditure for Activity Groups

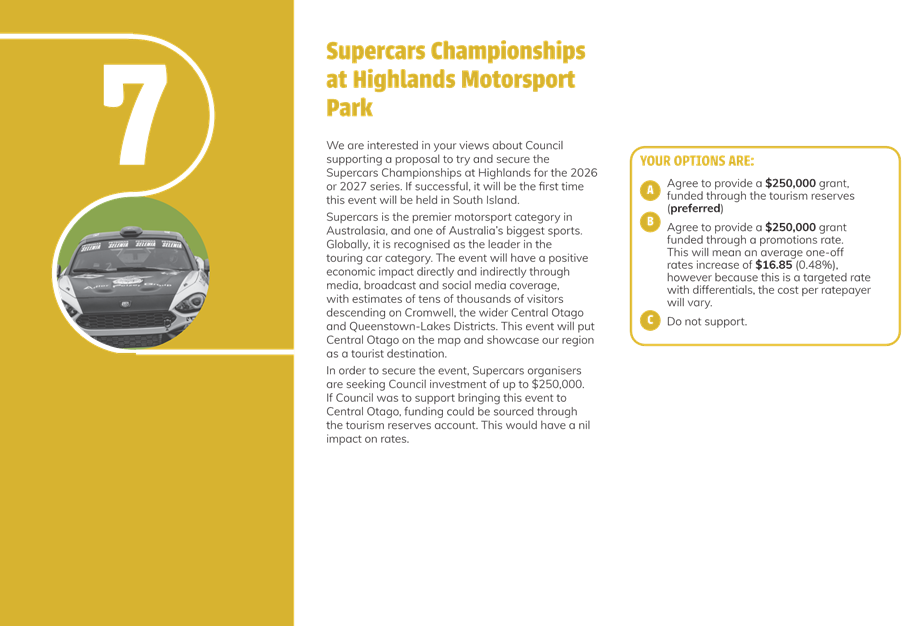

D. Agrees

that the consultation item for the Supercars grant that the preferred option

is to support the grant of $250,000 with funding from the tourism reserves.

E. Agrees that

the Chief Executive Officer is authorised, in consultation with the Mayor, to

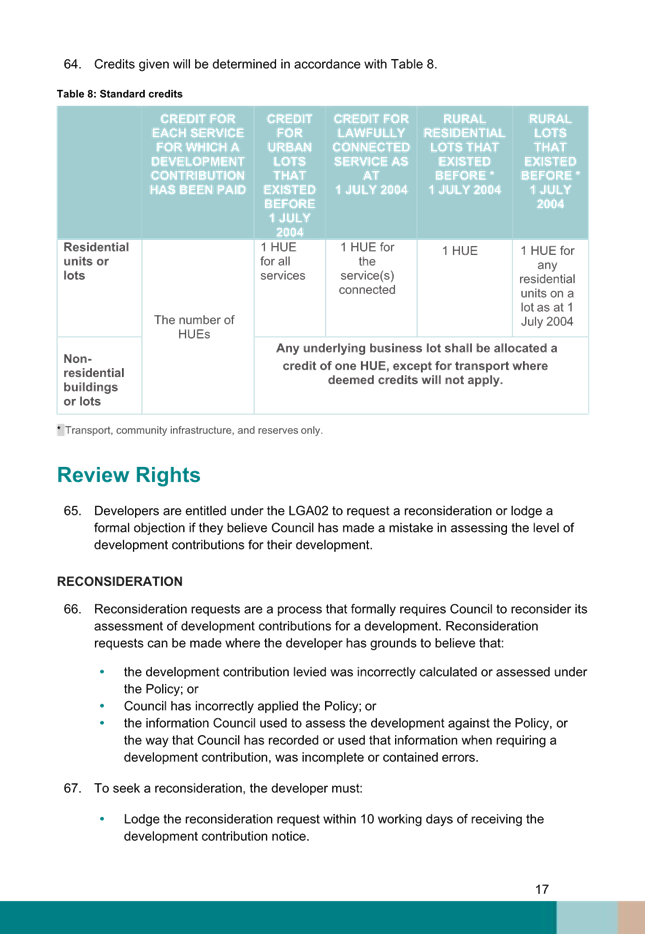

make any necessary formatting or editorial changes, or other such changes

required by Audit New Zealand, to finalise the material ahead of presentation

back to Council in March 2025.

|

2. Background

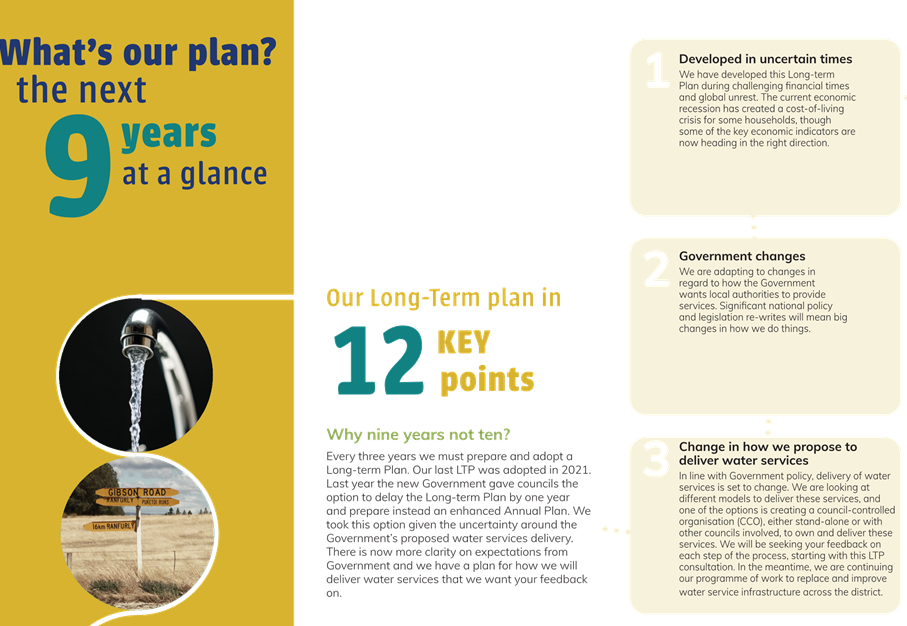

The Local Government Act

2002 (S 93 and 93A) requires Council to prepare and adopt a Long-term Plan

every three years. At the February 2024 Council meeting it was agreed

that the 2024-34 Long-term Plan be deferred and Council prepare an enhanced

2024-25 Annual Plan (under the options provided by the Government in the

legislative changes surrounding the repeal of the three waters legislation).

This decision results in

this being a nine-year plan (2025-34). Council will prepare the next long-term

plan in two years’ time (2027-37 Long-term Plan) to get back into cycle

with the requirements of the Local Government Act 2002.

The long-term plan process

requires that Council prepare a Consultation Document and supporting

information that has been audited by Audit New Zealand. Both the

Consultation Document and the supporting information will be made available to

the public.

Members of Council and the

community boards have attended a number of workshops to identify the topics to

be included in the 2025-34 Long-term Plan Consultation Document.

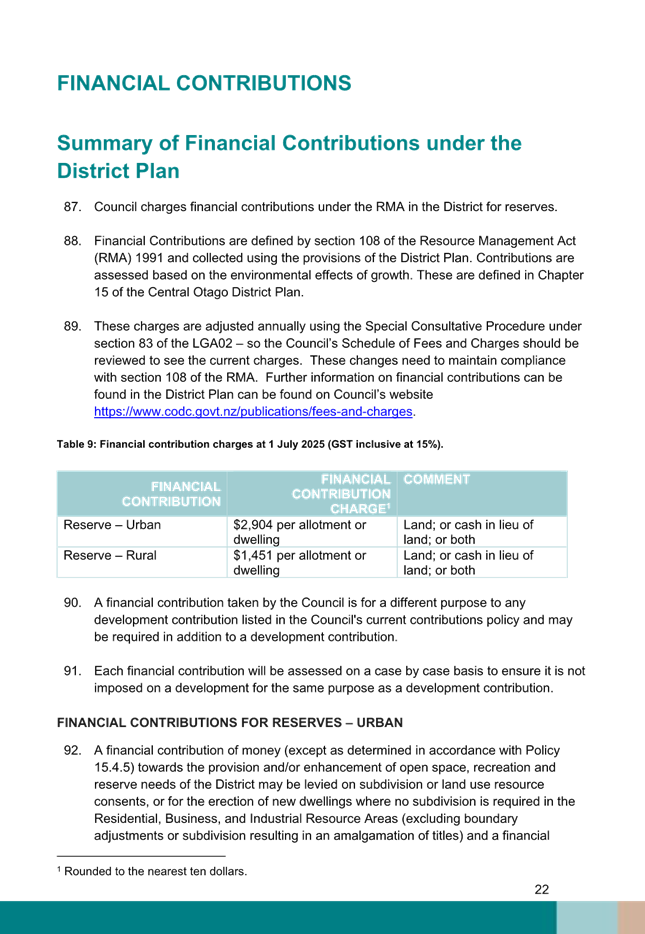

Community boards have reviewed their proposed grant budgets and have

recommended those proposed budgets be included in Council’s overall

proposed rate increases (refer to the separate paper being presented at this

meeting).

3. Discussion

Council is required to

adopt a Consultation Document for the 2025-34 Long-term Plan that has been

audited by Audit New Zealand. The Consultation Document outlines

Council’s consultation ideas for the future and provides instructions to

the public on the submission process.

At the meeting on 18

December 2024, Council agreed the following would be included as consultation

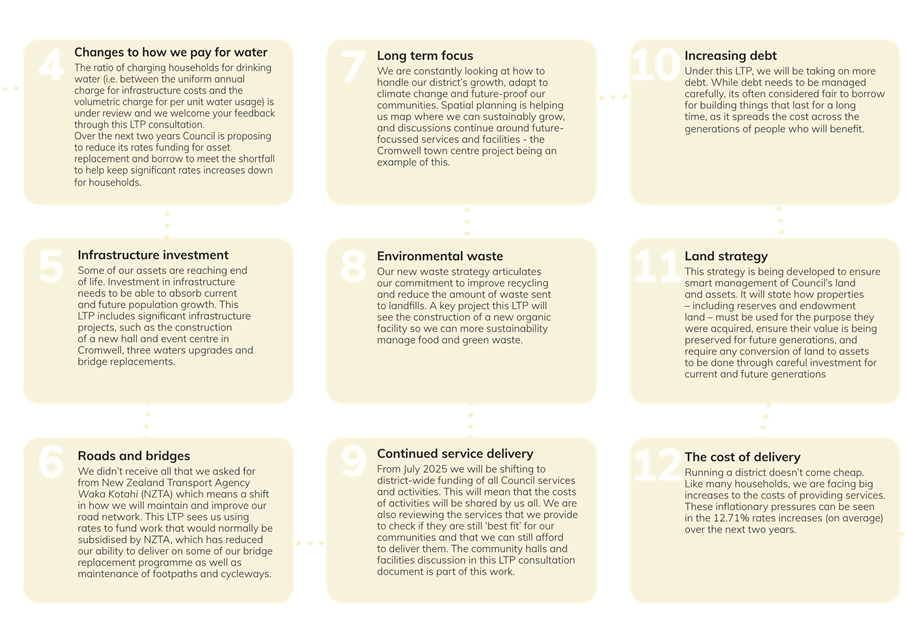

items:

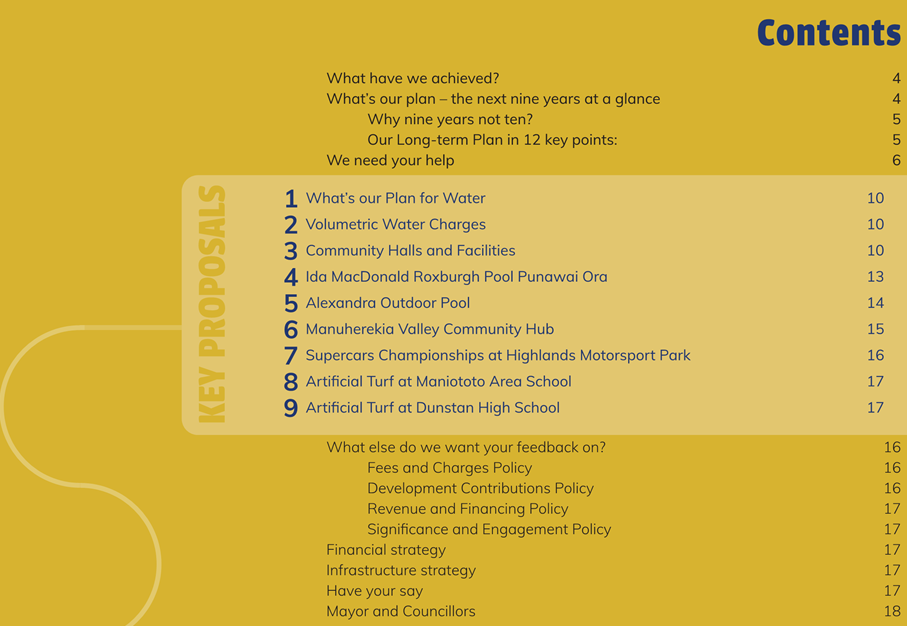

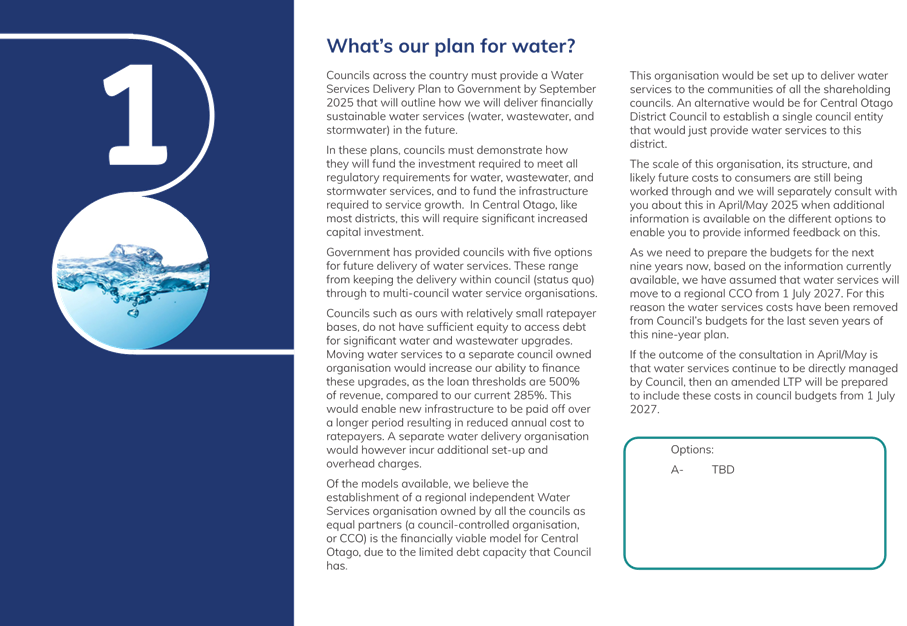

1. What’s

our plan for water?

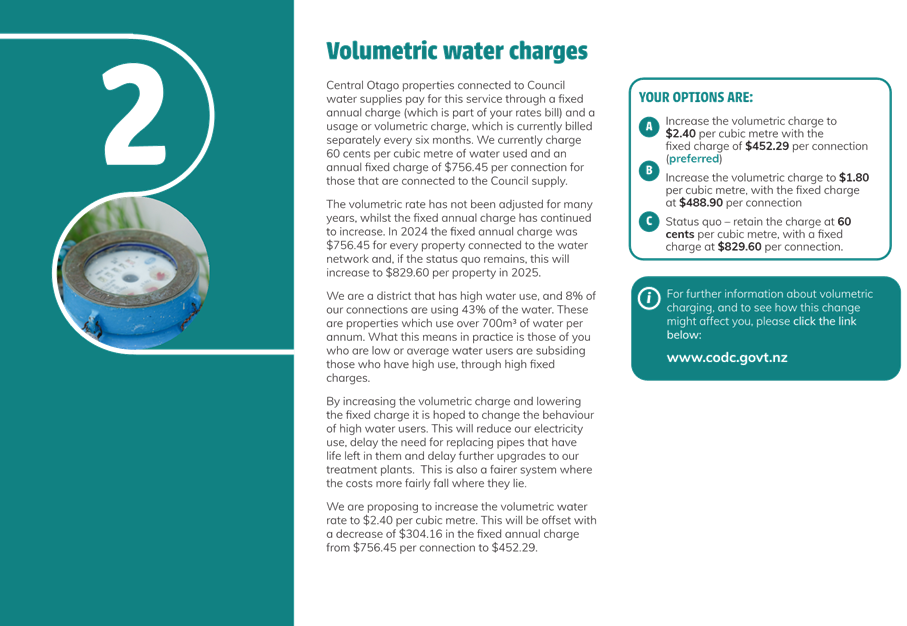

2. Volumetric

water charges

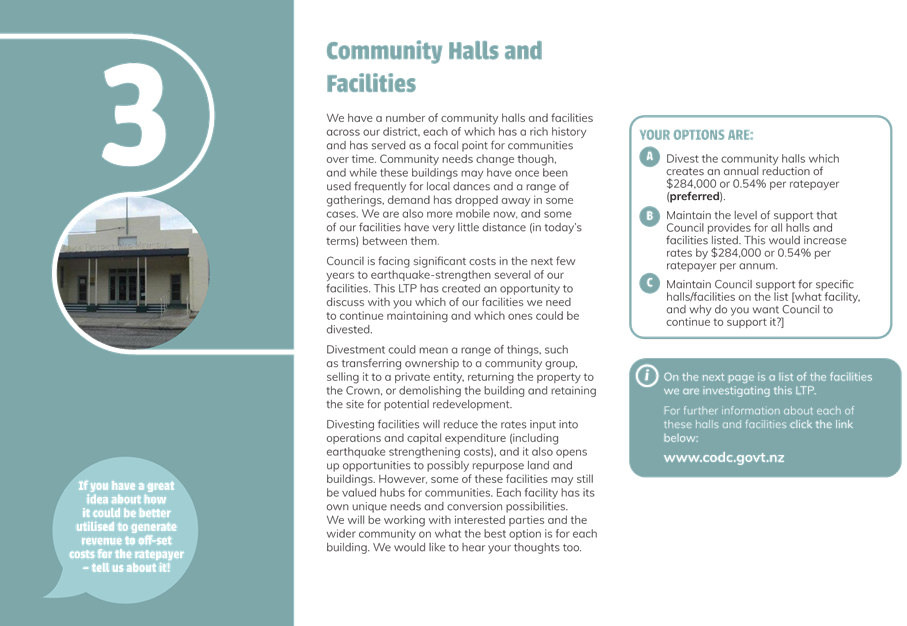

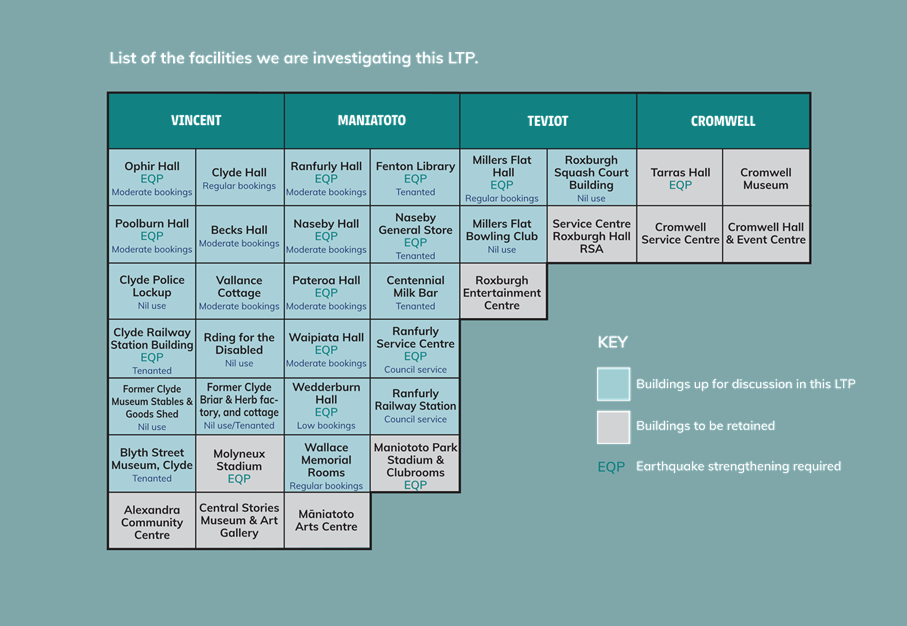

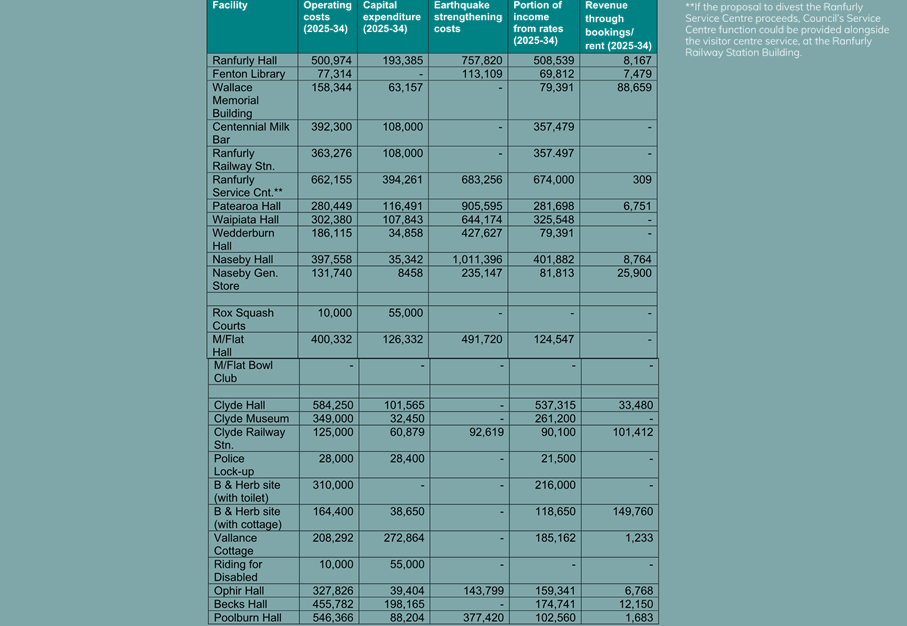

3. Community

halls and facilities

4. Ida

MacDonald Roxburgh Pool Punawai Ora

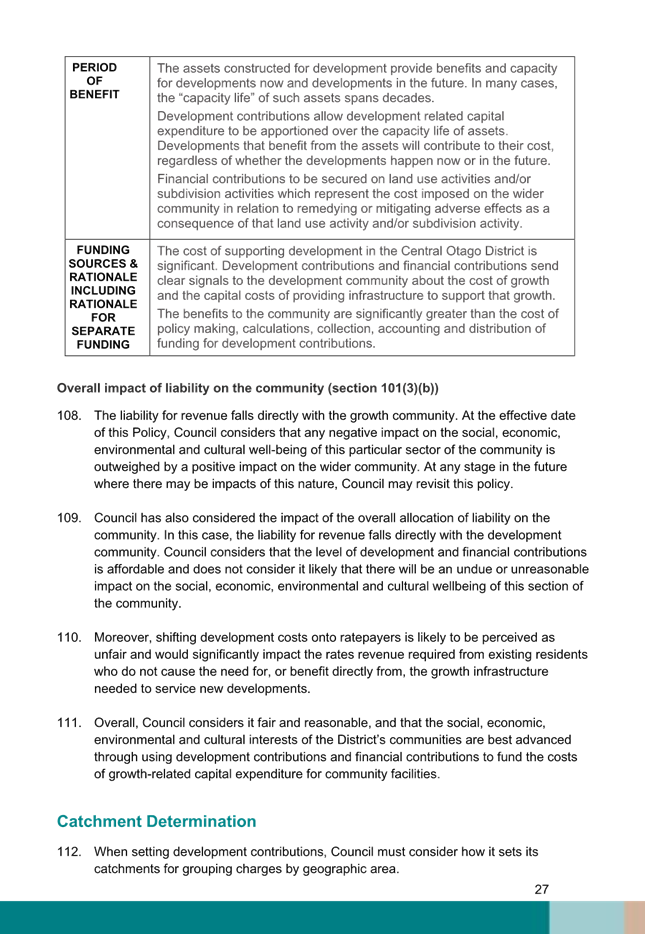

5. Alexandra

Outdoor Pool

6. Manuherekia

Valley Community Hub

7. Supercars

Championships at Highlands Motorsport Park

8. Artificial

Turf at Maniototo Area School

9. Artificial

Turf at Dunstan High School

At this meeting Council

also agreed their preferred option for each item. On further analysis, there is

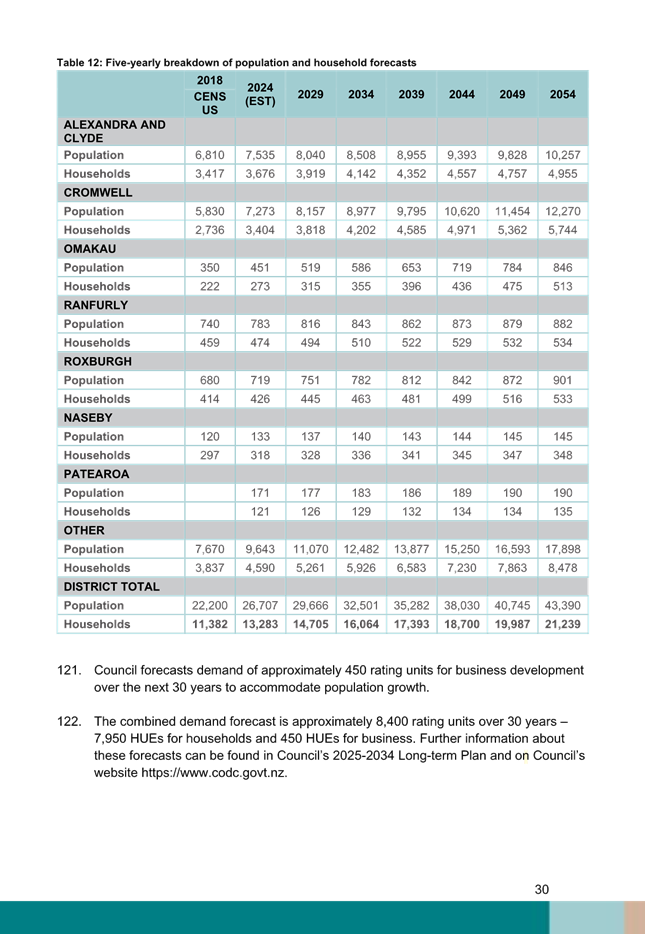

$400,000 in the tourism reserves. Staff recommend rather than funding the

proposed grant of $250,000 from a promotions rate, that these reserves are used.

This would result in a nil impact on ratepayers.

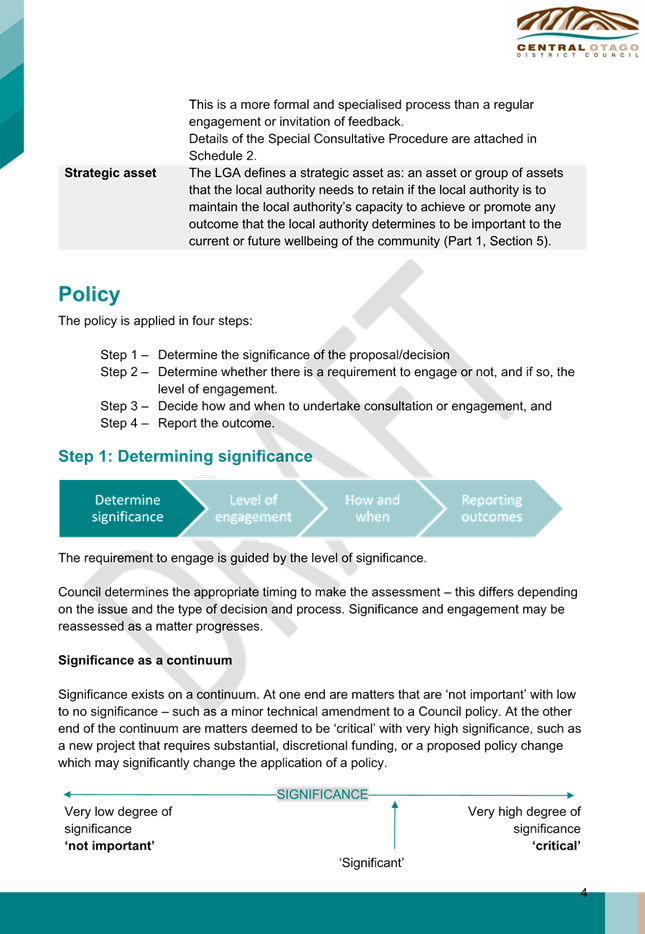

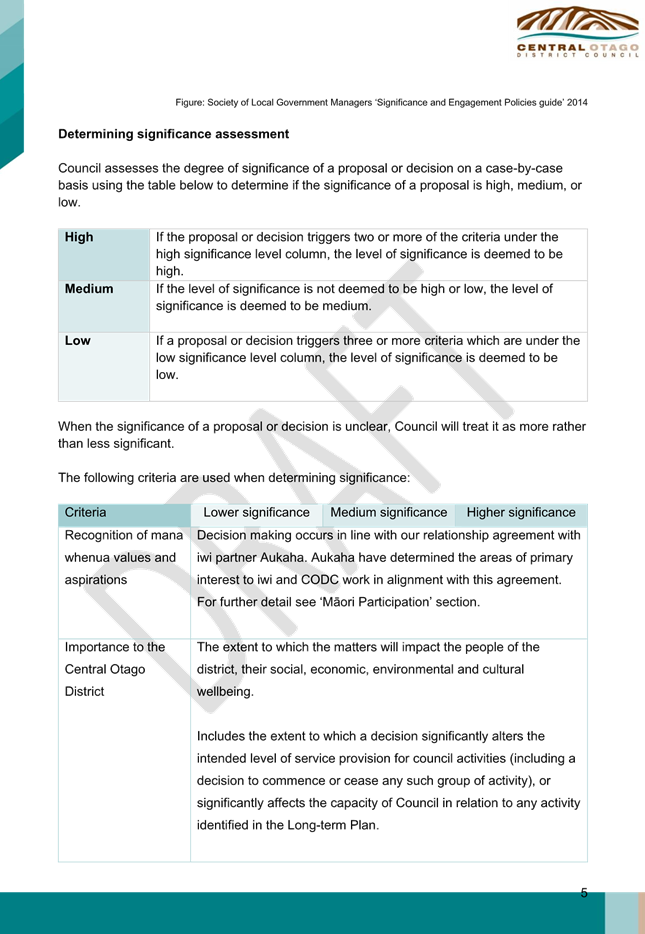

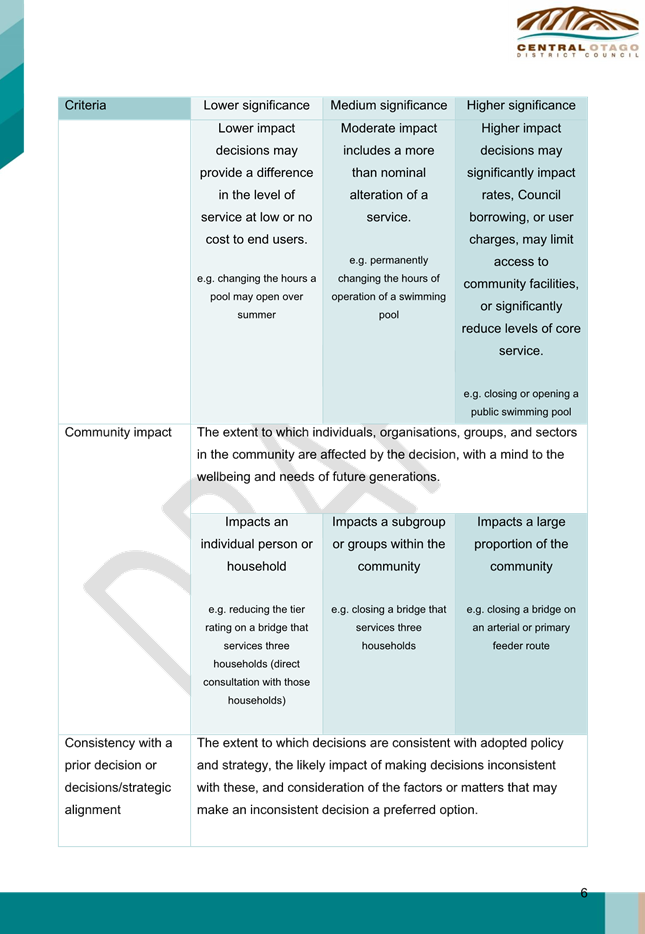

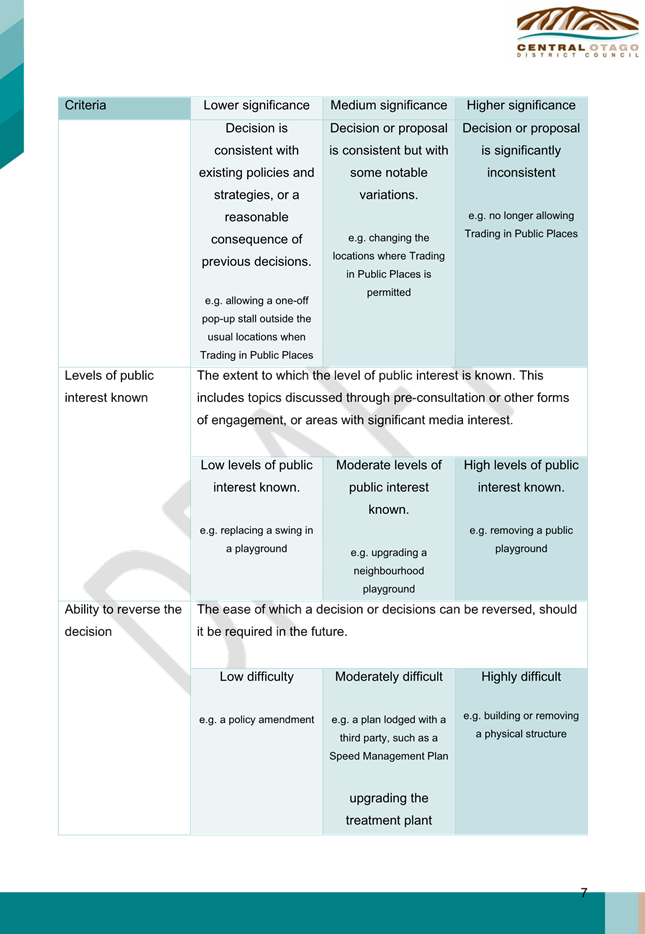

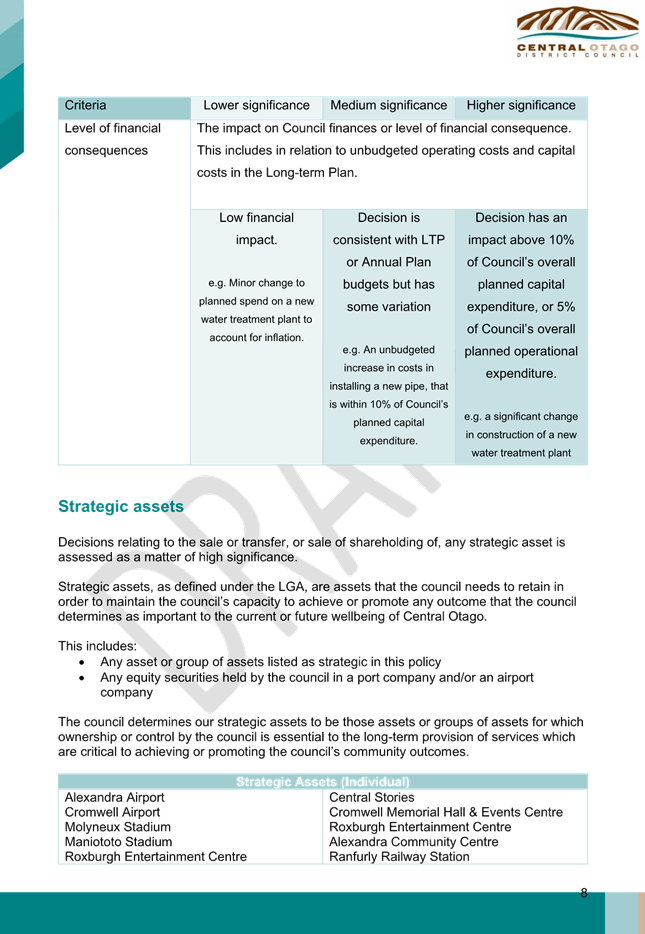

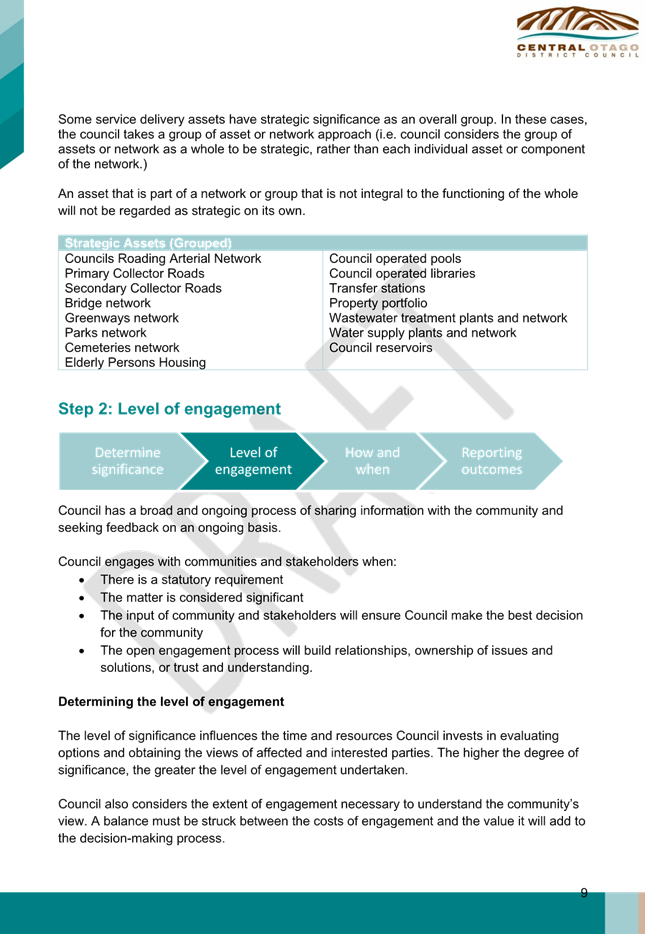

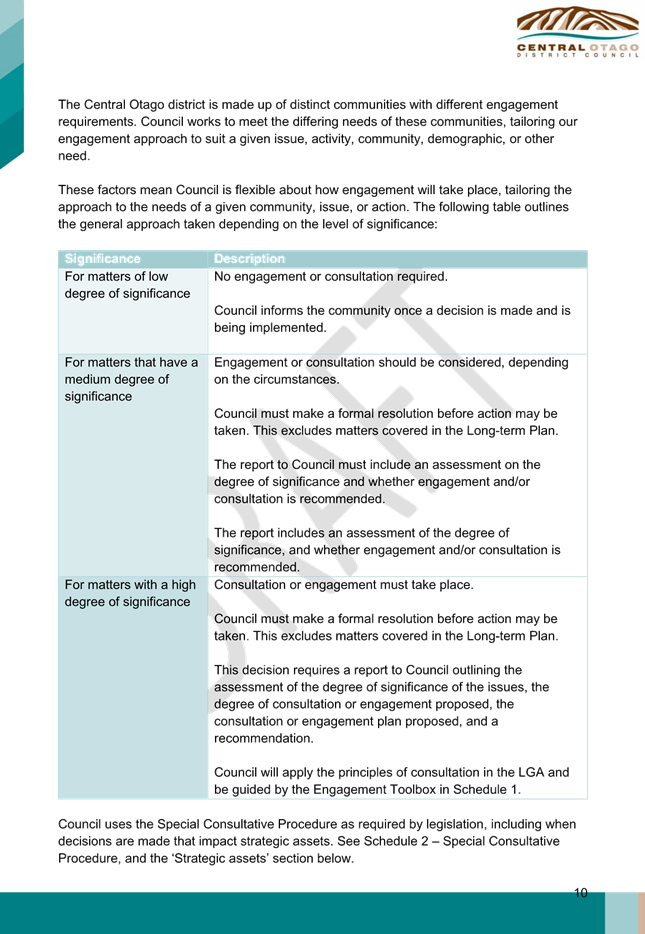

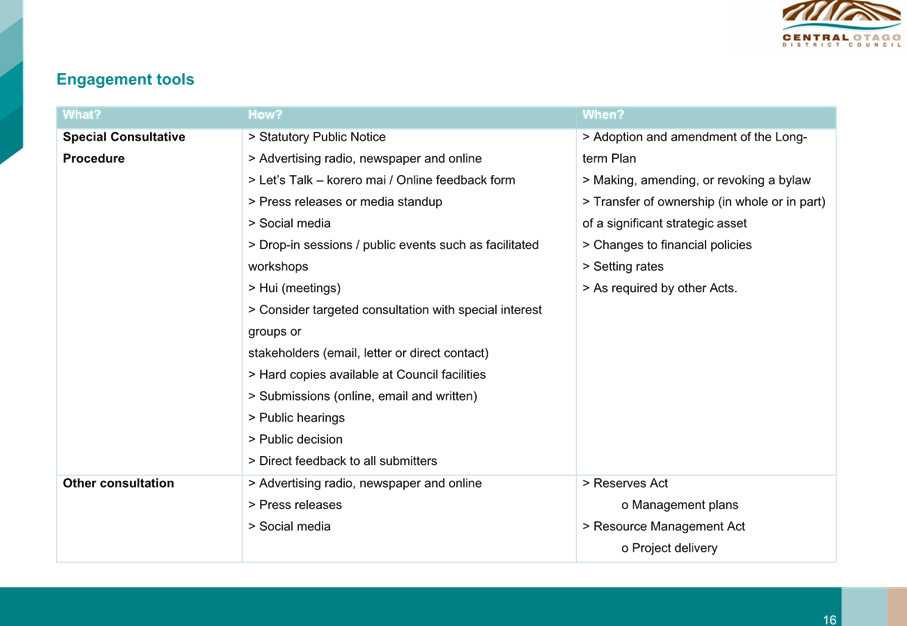

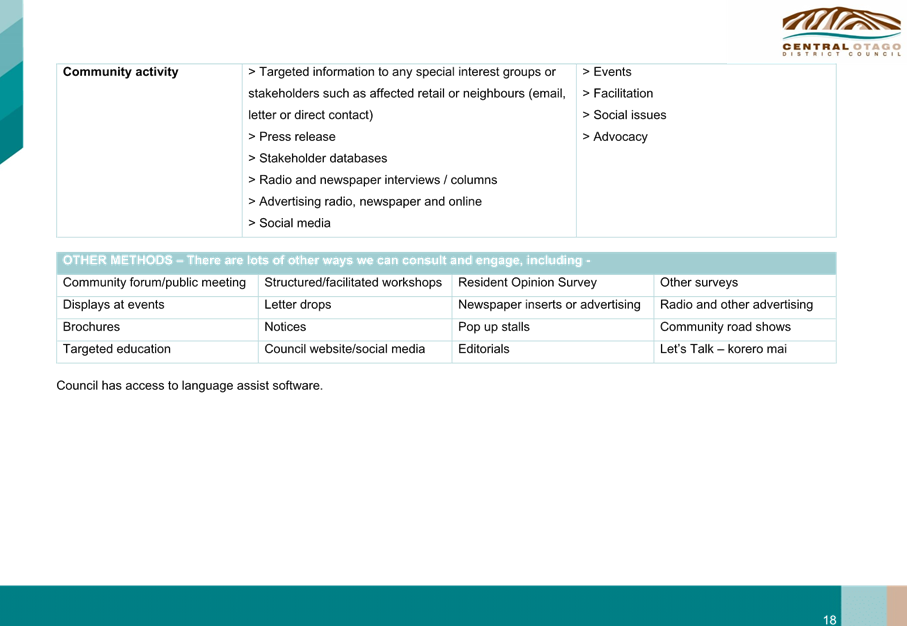

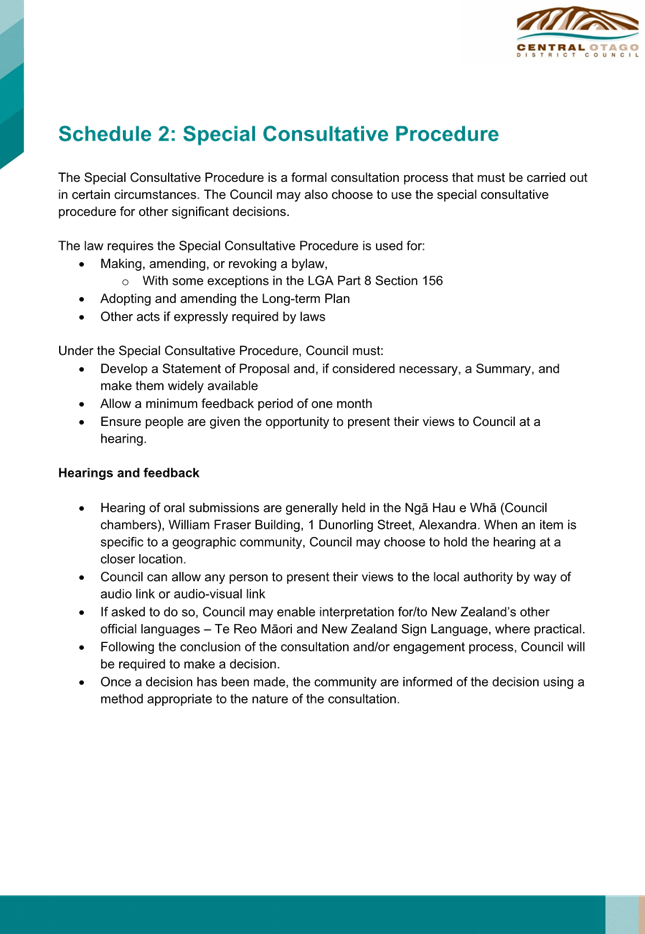

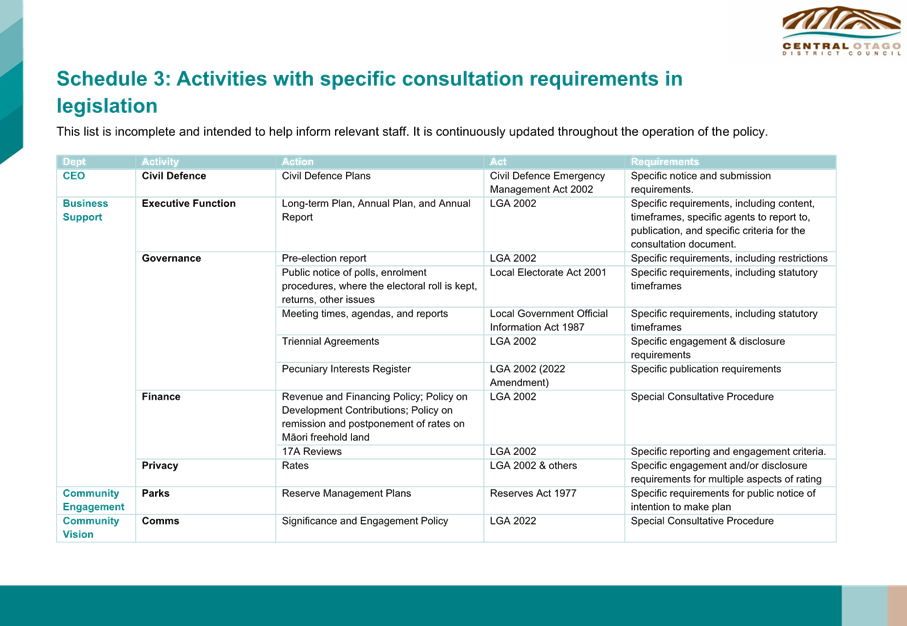

The Significance and

Engagement Policy was reviewed by the Audit and Risk Committee. As a result of

feedback, the following changes were updated: finalising the Strategic Asset

section and grouping some of the individually listed items; removed phrase ‘all

aspects of decision making’ in the Māori Participation Framework;

amended typos; adjusted wording in the table on mana whenua engagement; changed

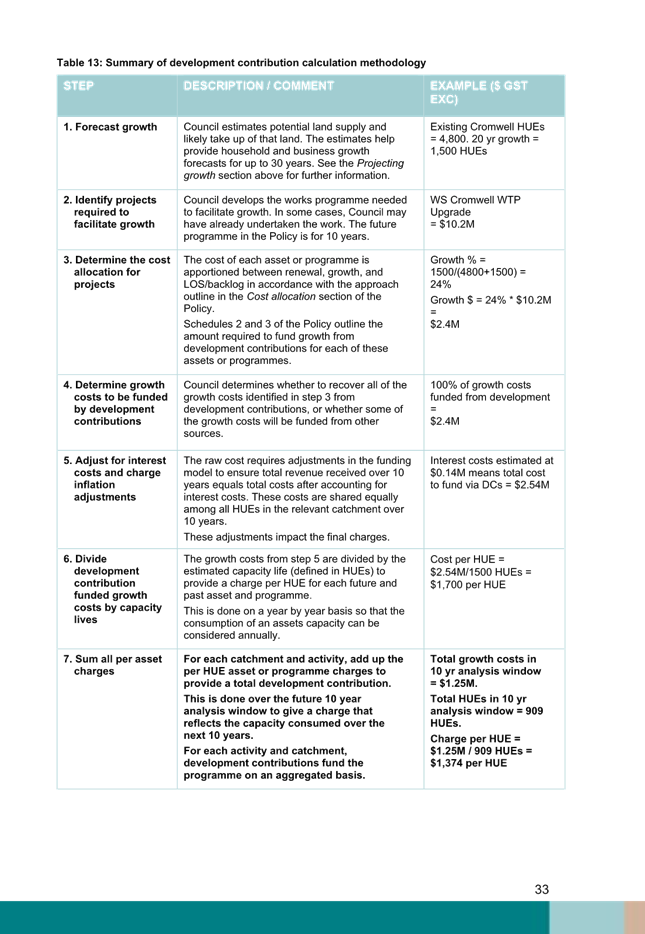

‘Promise to the Public’ to ‘Commitment to the Public’

in Schedule 1; and adjusted the arrow in the Significance Continuum on page 4

of the Policy. Staff felt these adjustments reflected the feedback of the

Committee while adhering to the guidance of the Office of the Auditor General,

that the Policy meets the expectations of the specific community with regard to

significance.

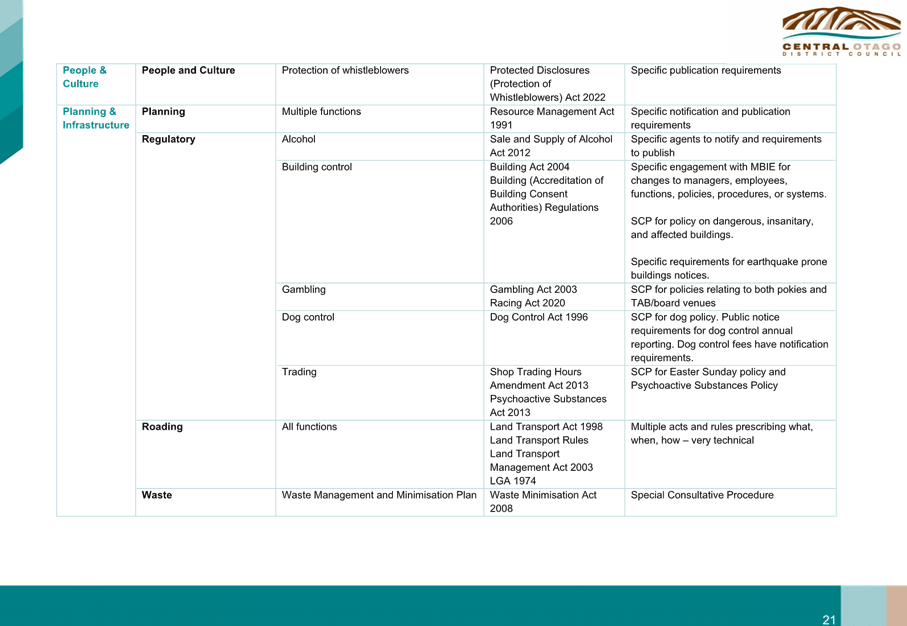

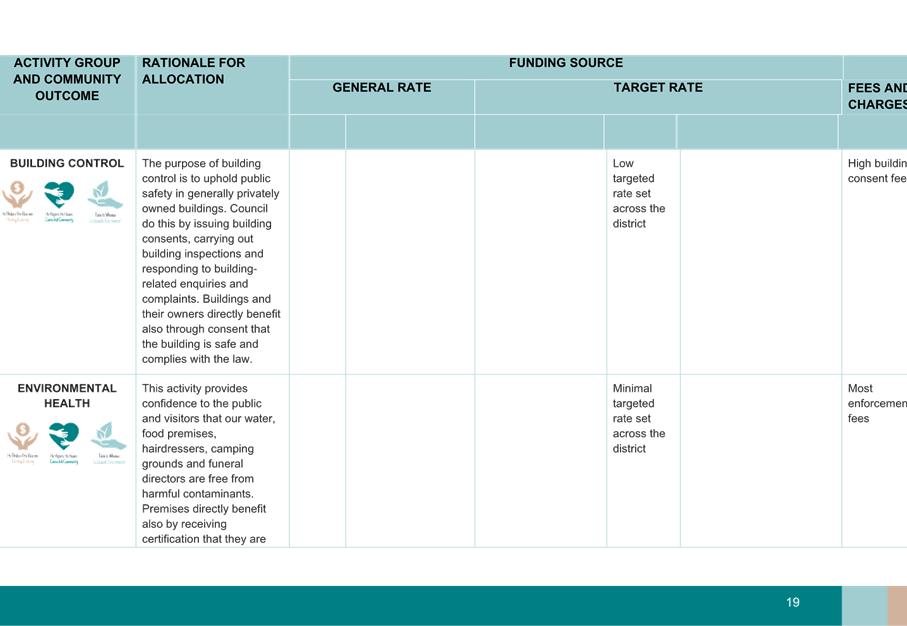

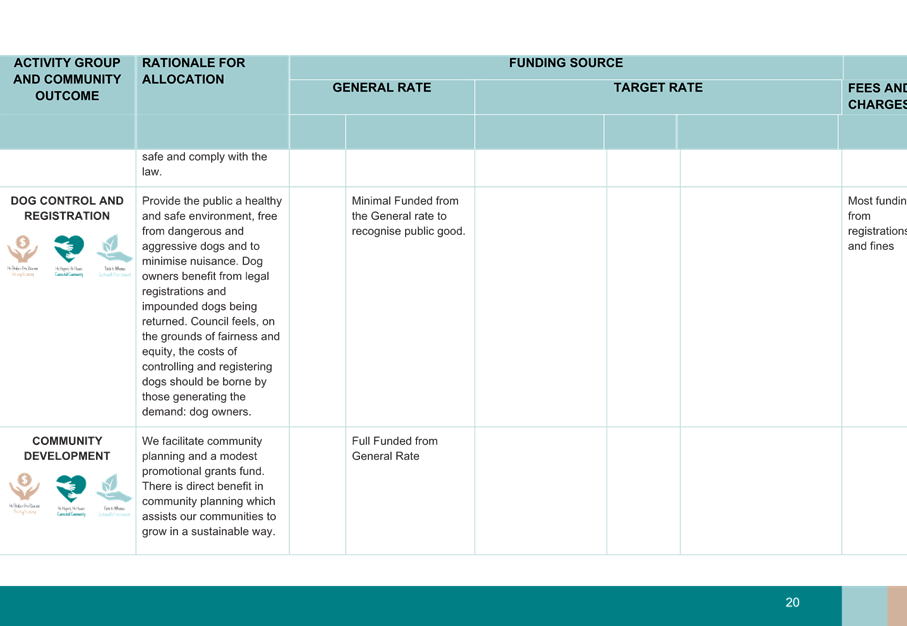

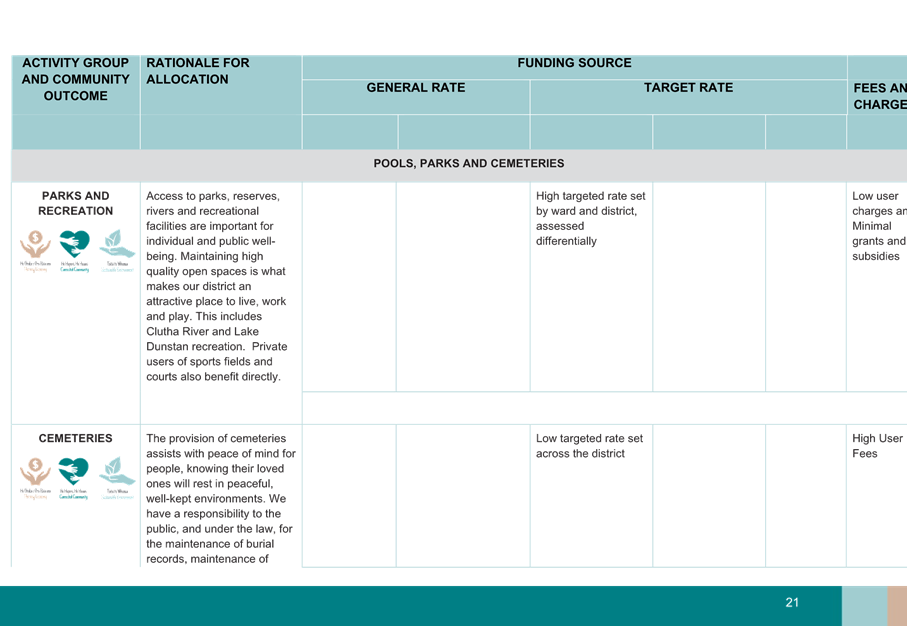

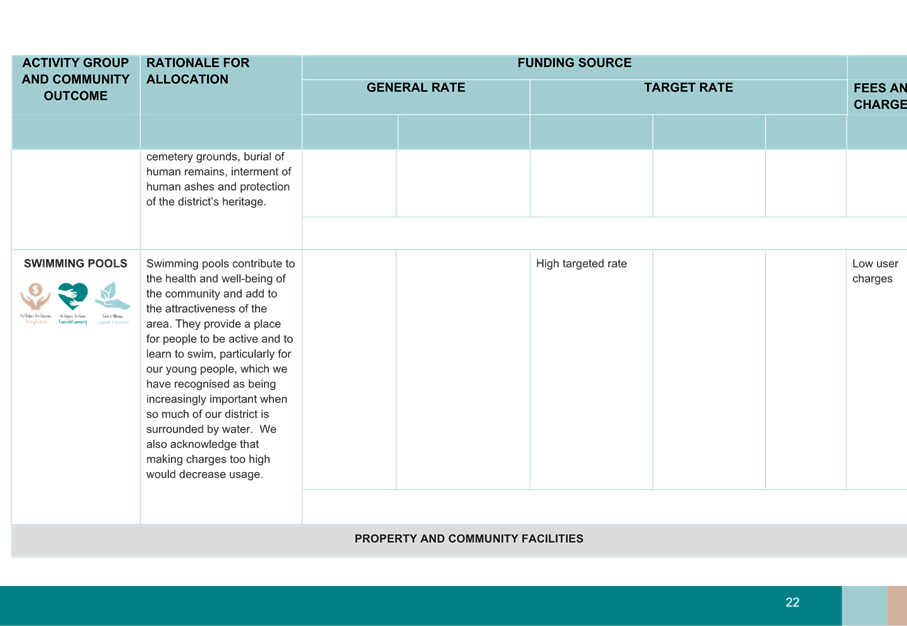

In order to facilitate the audit process Council is required to provide

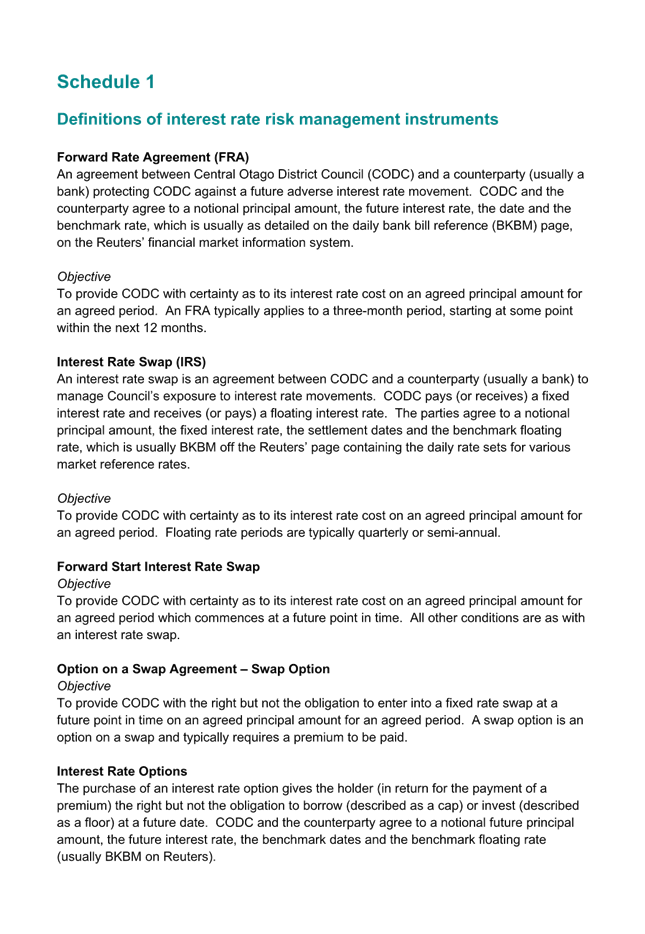

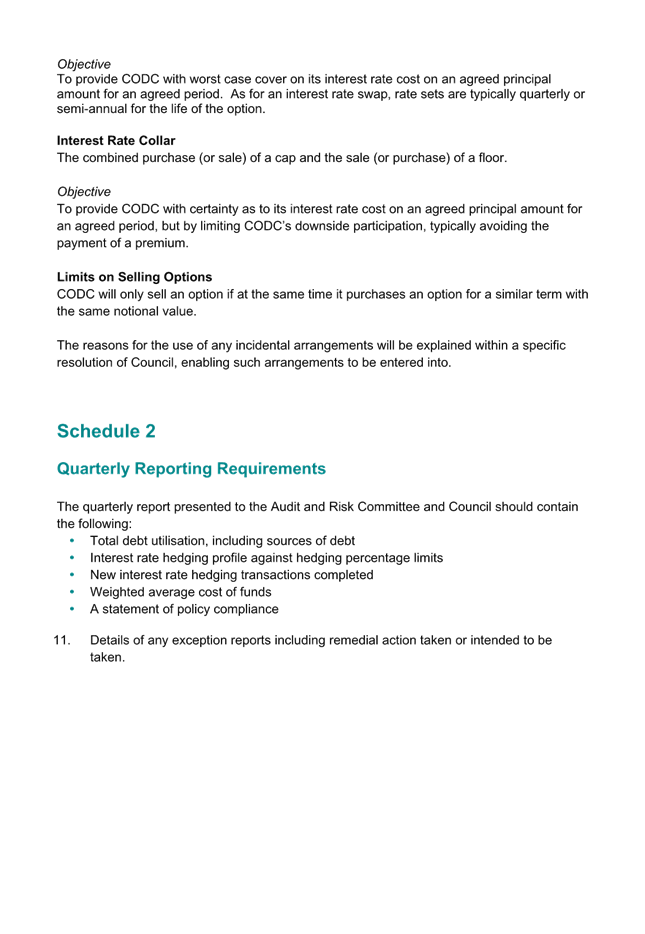

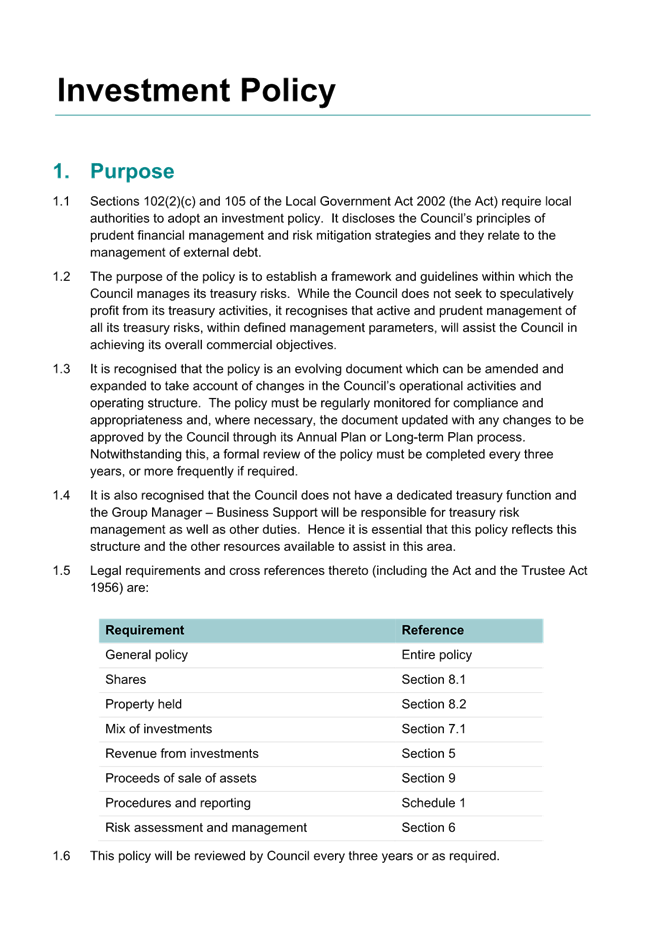

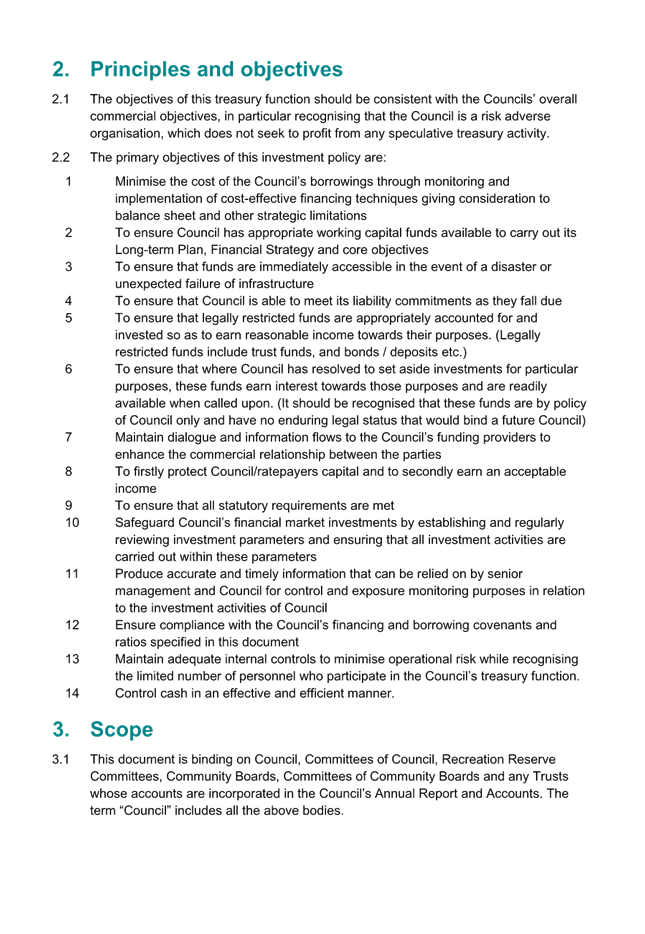

supporting material to Audit New Zealand. This information comprises the

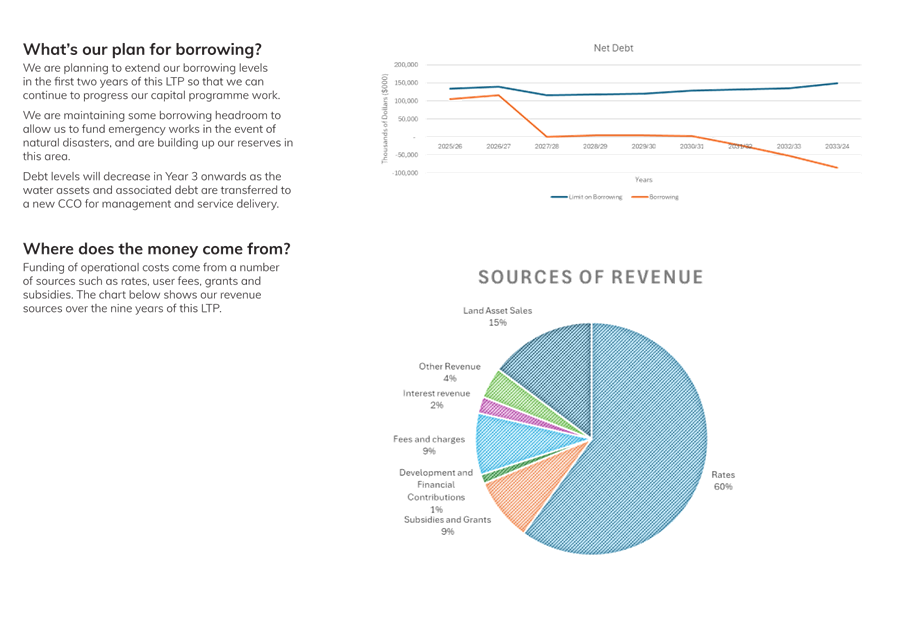

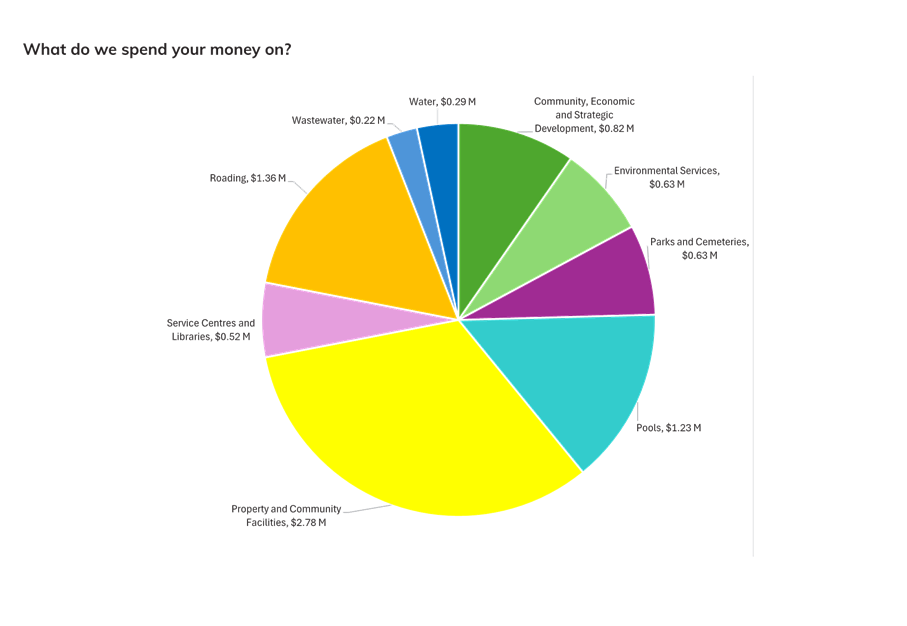

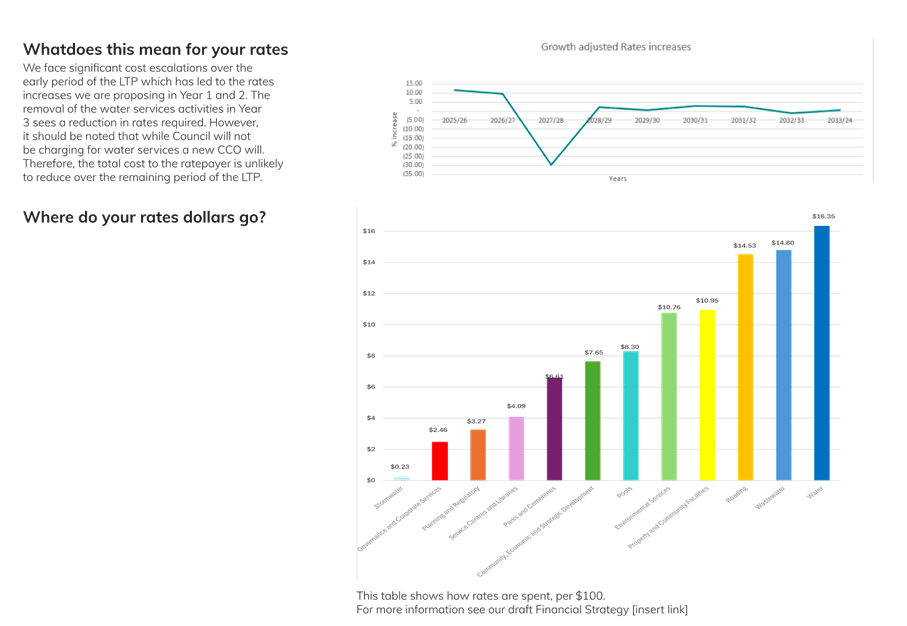

Infrastructure Strategy, Financial Strategy, Prospective Financial Information,

Funding Impact Statement (Rates), Revenue and Financing Policy, Rates Remission

and Postponement Policy, Investment Policy, Liability Management Policy,

Significance and Engagement Policy, Significant Forecasting Assumptions and

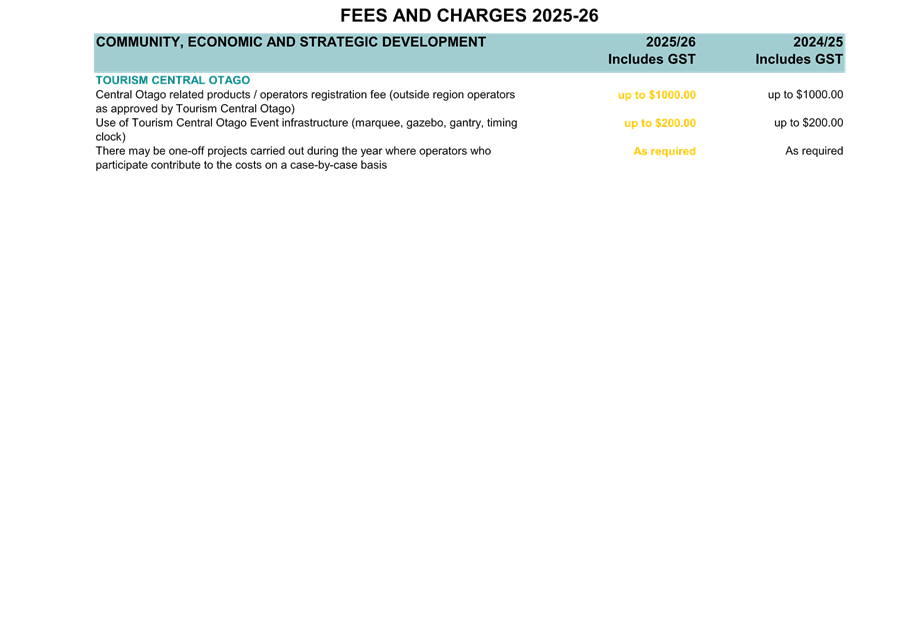

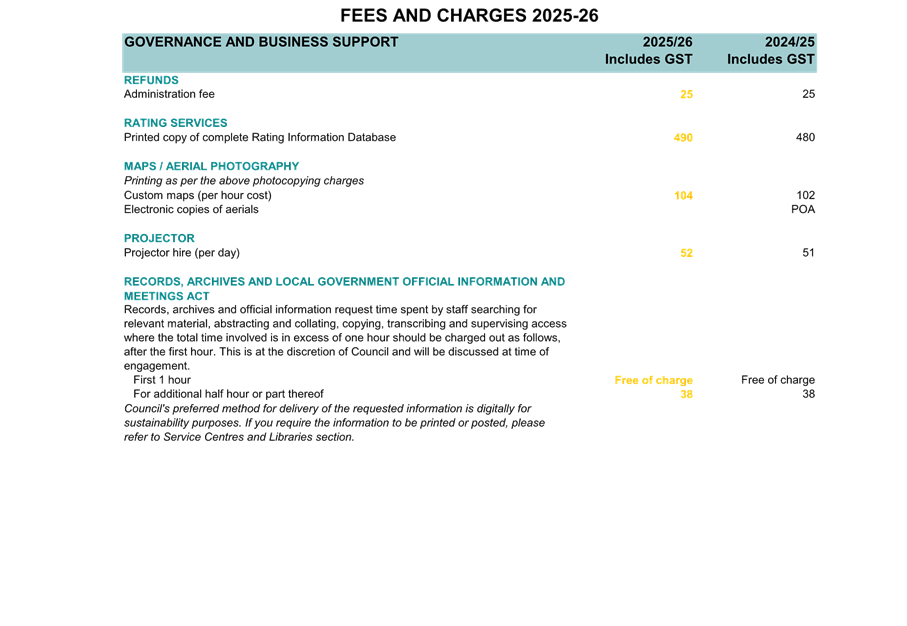

Risks, Development and Financial Contributions Policy and the Schedule of Fees

and Charges. Changes may be made to these documents as a result of the audit

and the public consultation process. These documents will also form the basis

for the final 2025-34 Long-term Plan which is planned to be adopted by Council in

June 2025.

This material will be considered by the Audit and Risk Committee on 28

January 2025. Due to time constraints their feedback will be verbally presented

to Council. Note at the

time of generation of this agenda, staff are waiting for a decision on how to

treat water services in the consultation document. The challenge is that

Central Otago District Council is in conversations with other councils about a

joint Council Controlled Organisation, of which consultation will occur after

the audit of the consultation document. The material in the consultation

document may well change during the audit in February.

4. Financial

Considerations

These are covered in the attached financials.

5. Options

Option 1 –

(Recommended)

Approve that the

consultation document and supporting material is provided to Audit New Zealand

to enable the audit to commence on 3 February 2025.

Advantages:

· Adheres

to the scheduled programme for the development of 2025-34 Long-term Plan.

· Ensures

compliance with the requirements of the Local Government Act 2002.

· Meets

community expectations.

.

Disadvantages:

· None

identified.

Option 2

Approve that the

consultation document and supporting material with amendments is provided to

Audit New Zealand to enable the audit to commence on 3 February 2025.

Advantages:

· Adheres

to the scheduled programme for the development of 2025-34 Long-term Plan.

· Ensures

compliance with the requirements of the Local Government Act 2002.

· Meets

community expectations.

Disadvantages:

· None

identified.

Option 3

Do not approve that the

consultation document and supporting material is provided to Audit New Zealand

to enable the audit to commence on 3 February 2025.

Advantages:

· None

identified.

Disadvantages:

· Does

not adhere to the scheduled programme for the development of 2025-34 Long-term

Plan.

· Does

not comply with the requirements of the Local Government Act 2002 and will

likely cause delays. There is a risk that the 2025-34 Long-term Plan would not

be adopted by June 2025, impacting Council’s ability to collect rates for

the planned work programmes.

· Does

not meet community expectations.

6. Compliance

|

Local Government Act 2002 Purpose Provisions

|

This decision enables democratic local decision making and action

by, and on behalf of communities by ensuring the correct legal process is

followed in the development of the 2025-34 Long-term Plan.

|

|

Decision consistent with other Council plans and policies? Such as

the District Plan, Economic Development Strategy etc.

|

The consultation document and supporting material for the 2025-34

Long-term Plan is required under the Local Government Act 2002.

|

|

Considerations as to sustainability, the environment and climate

change impacts

|

There are no direct considerations as to sustainability, the

environment and climate change impacts.

|

|

Risks Analysis

|

There is no risk in approving these documents be provided to Audit

New Zealand. A delay in approving these documents will likely delay the audit

and impact on the plan to have the 2025-34 Long-term Plan presented for final

approval on 25 June 2025.

|

|

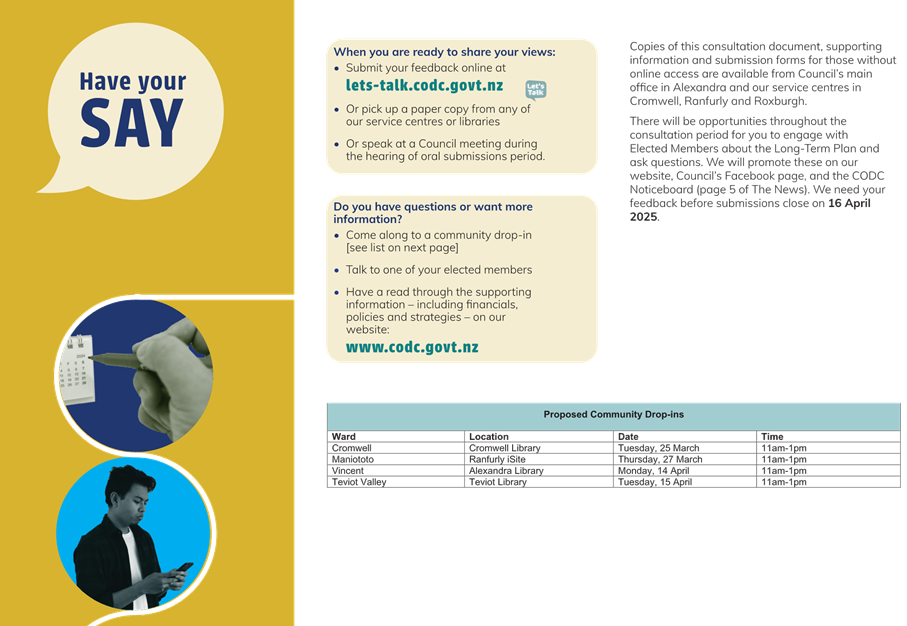

Significance, Consultation and Engagement (internal and external)

|

Once audited, these documents will be provided as part of the

material for the 2025-34 Long-term Plan consultation. Public consultation is

scheduled from 19 March to 16 April 2025.

|

7. Next

Steps

Following

Council agreement, the Consultation Document and supporting material will be

provided to Audit New Zealand, with the audit scheduled to commence 3 February

2025. Amendments will be made as required and presented back to Council on 17

March 2025 for approval to adopt these documents for formal consultation.

8. Attachments

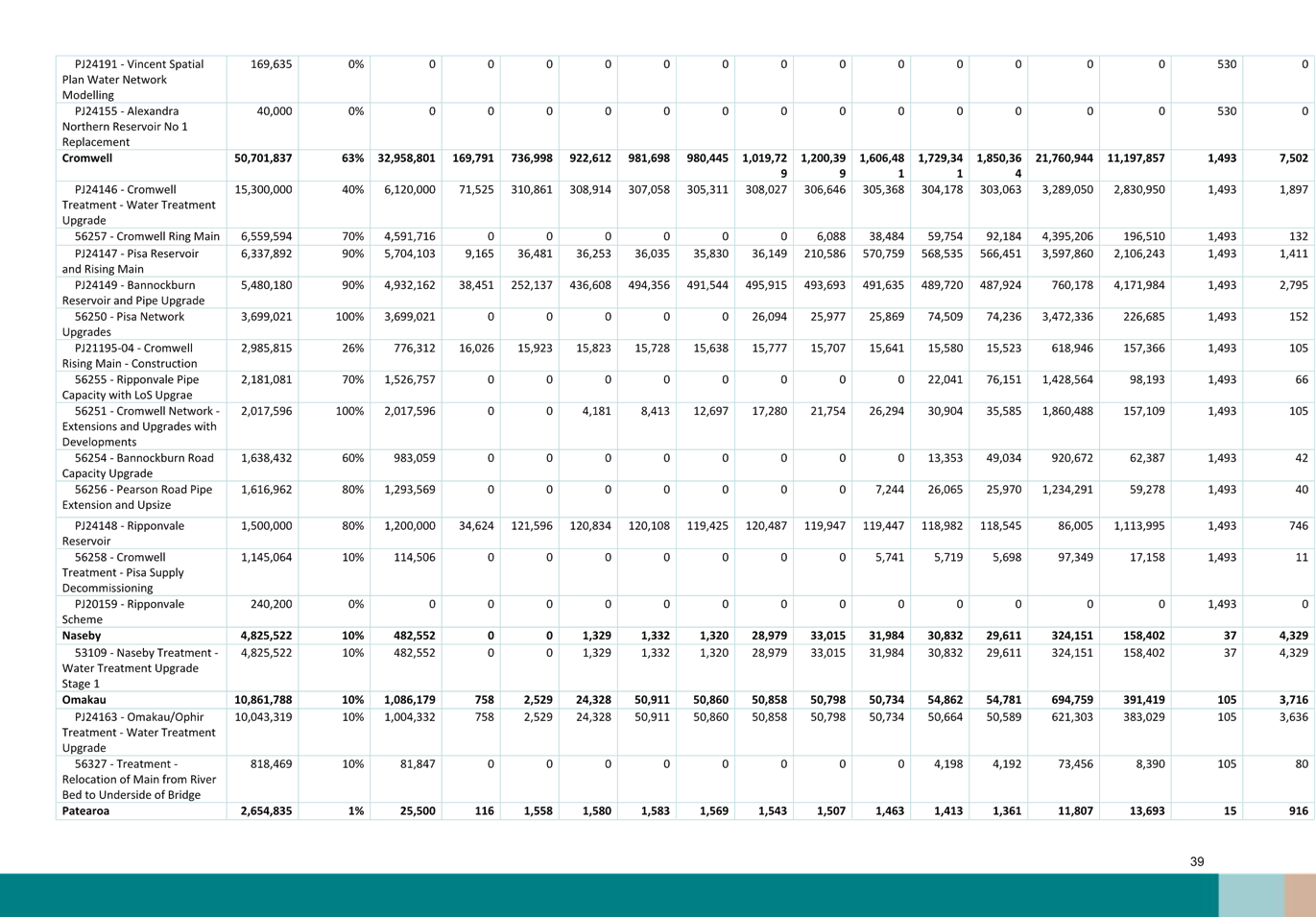

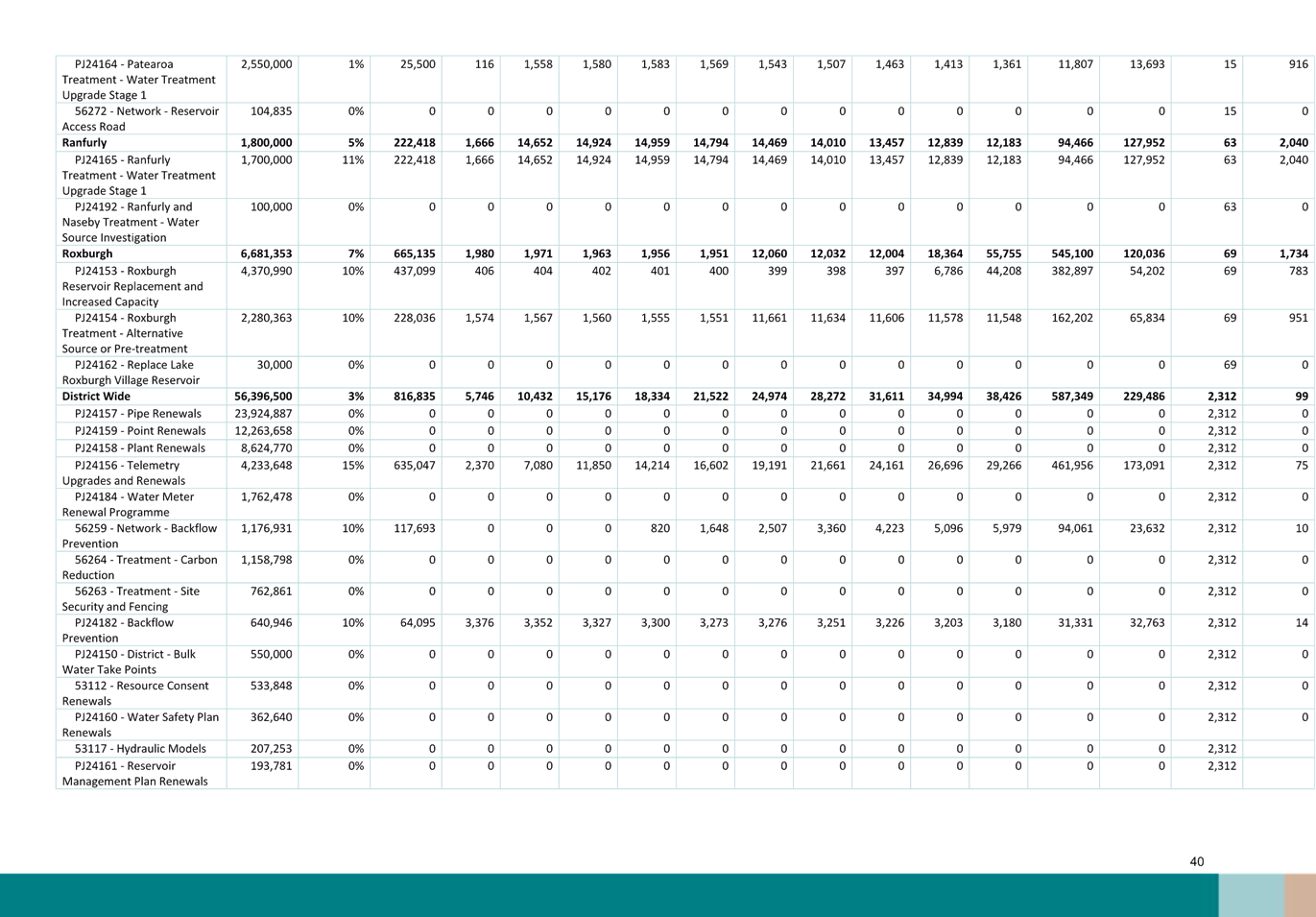

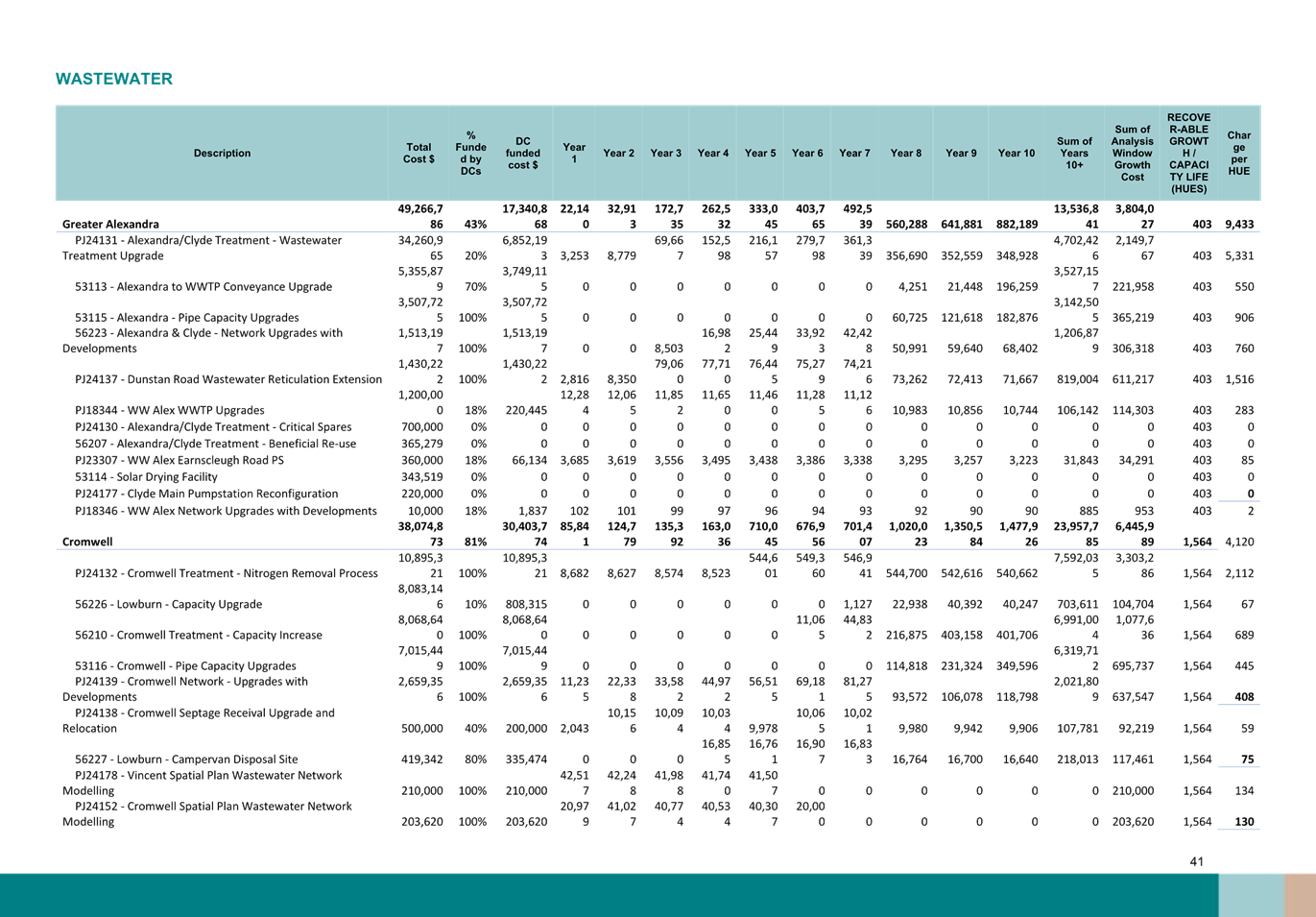

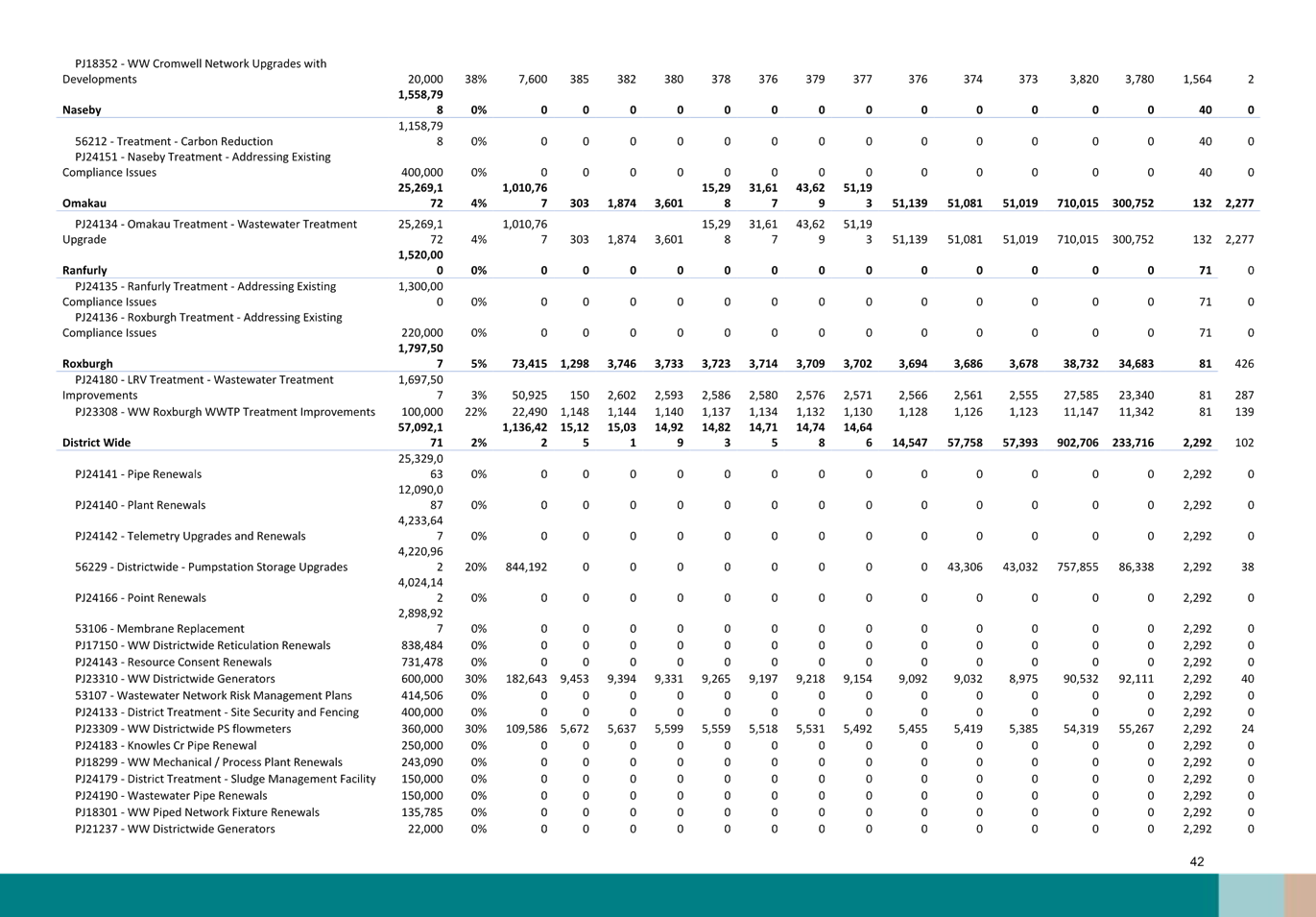

Appendix 1 - Draft Consultation

Document ⇩

Appendix 2 - Infrastructure

Strategy ⇩

Appendix 3 - Financial Strategy ⇩

Appendix 4 - Development and

Financial Contributions Policy ⇩

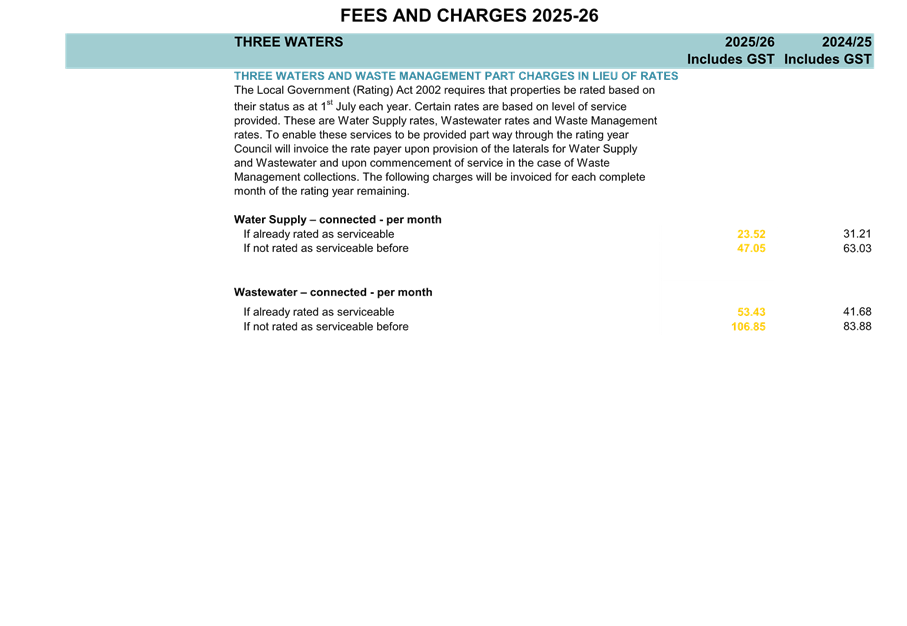

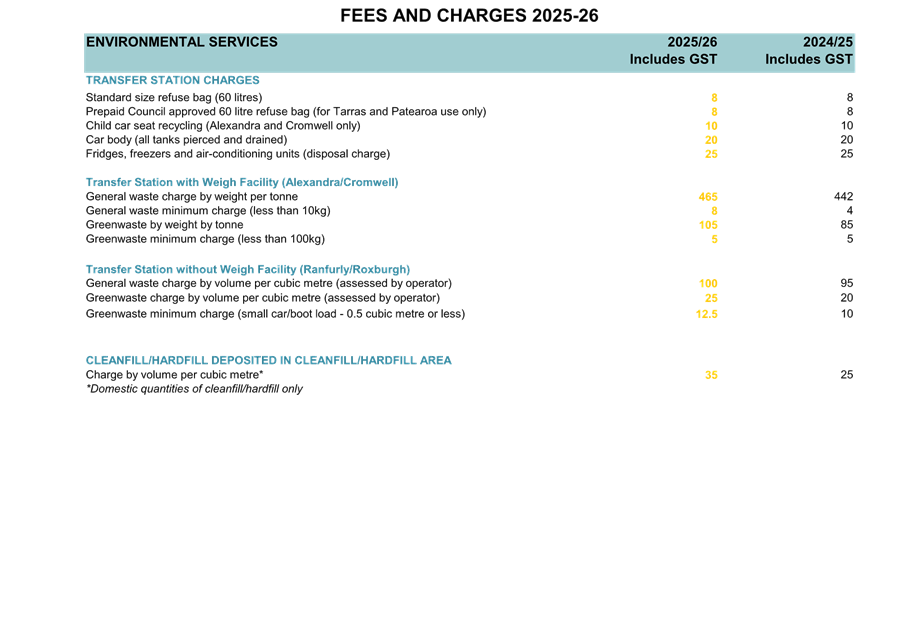

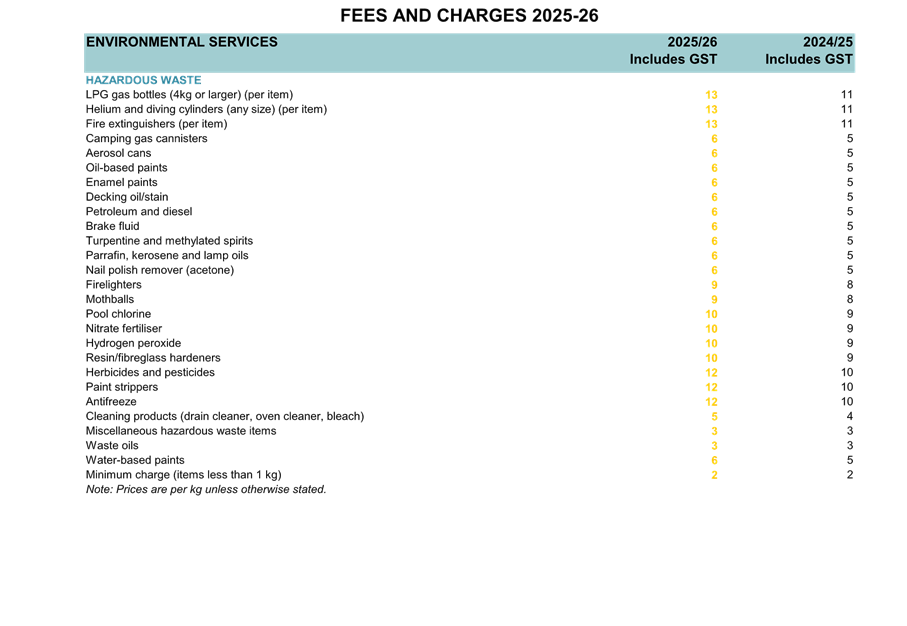

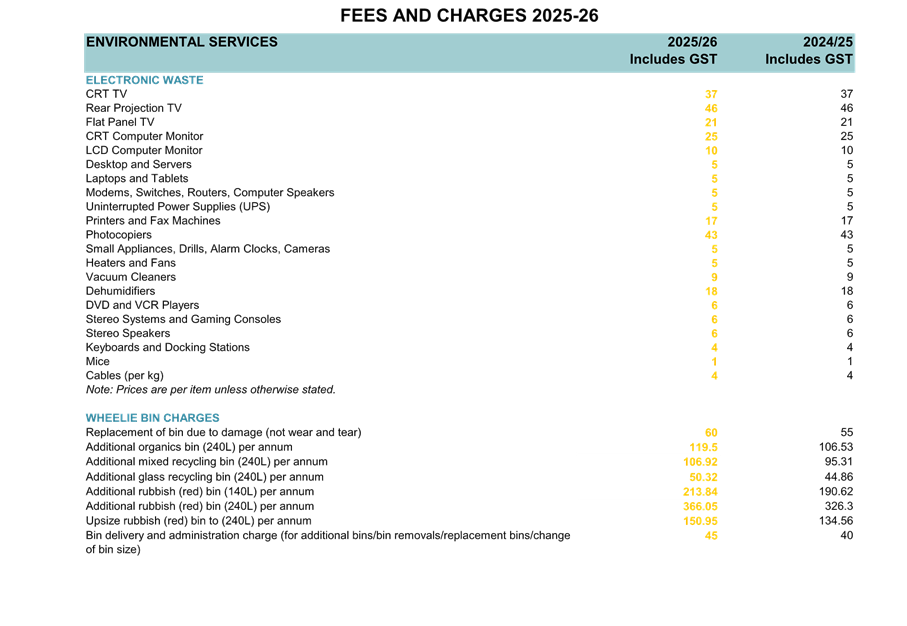

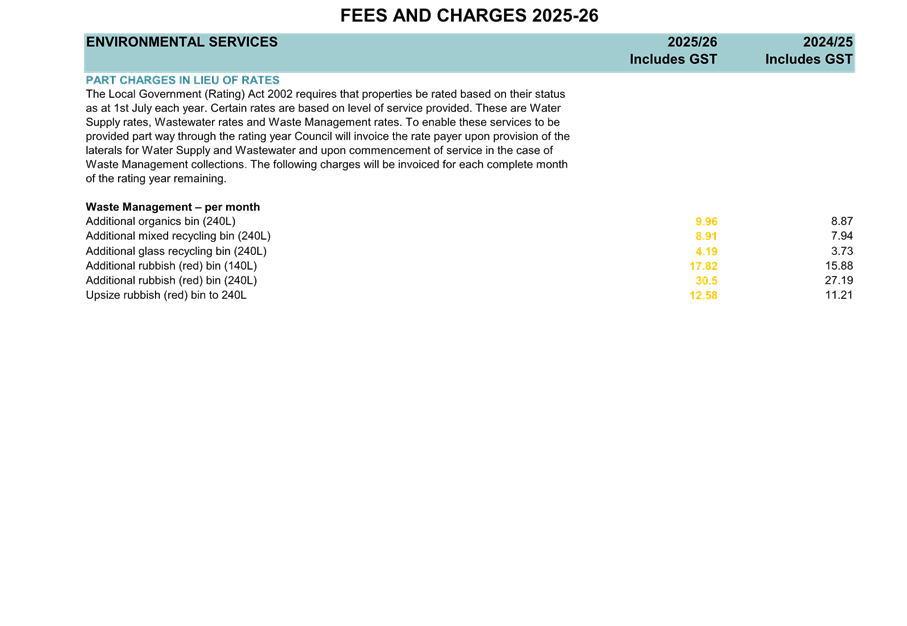

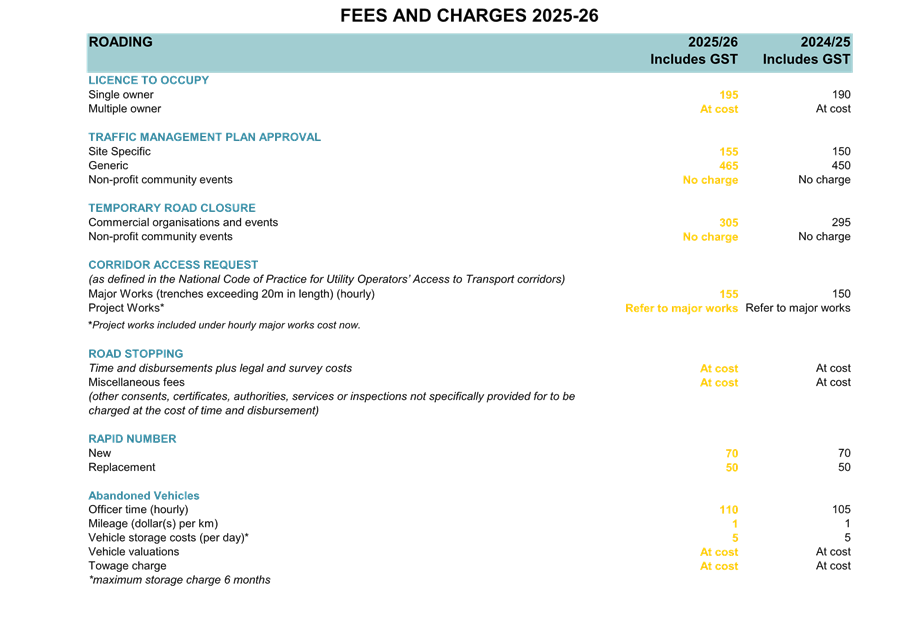

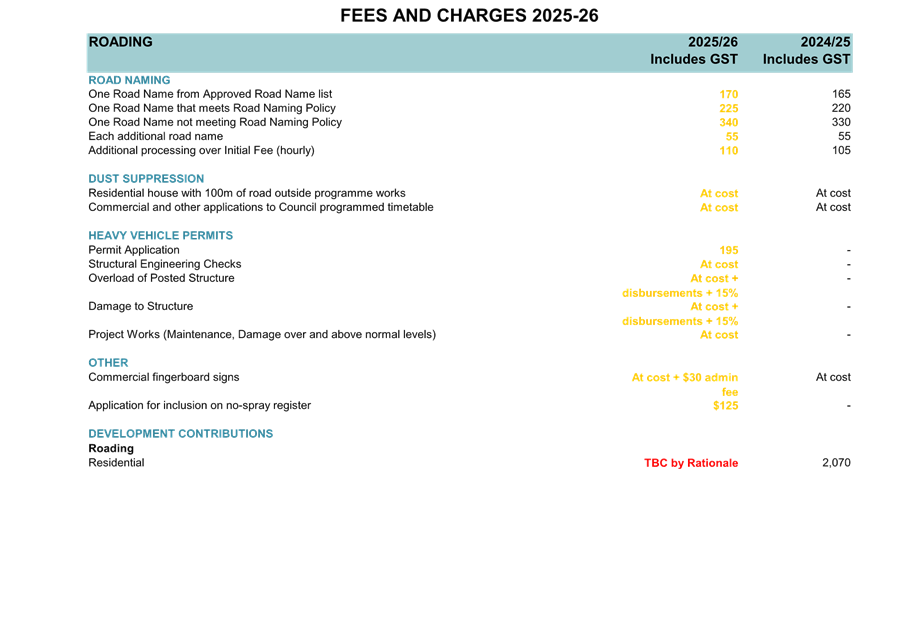

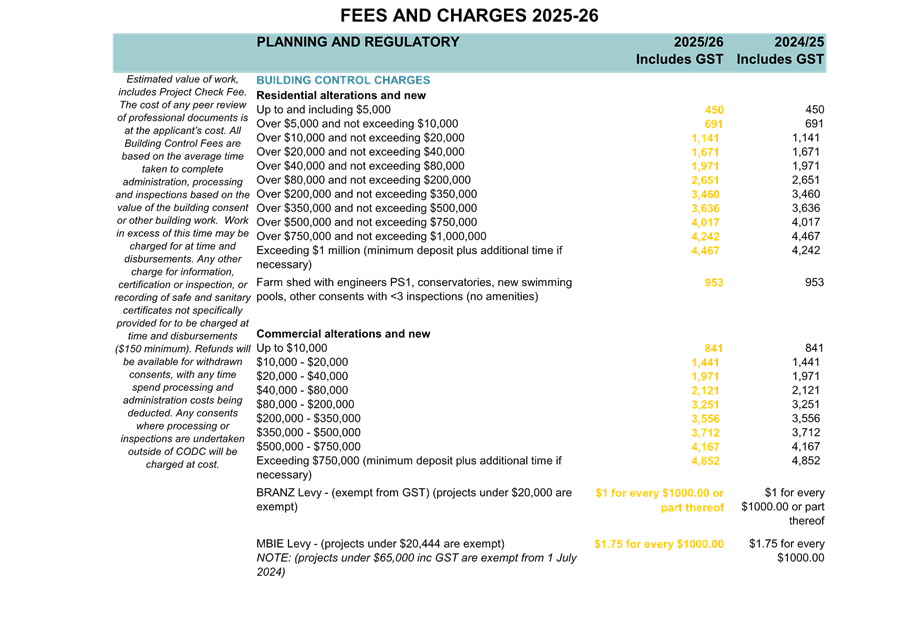

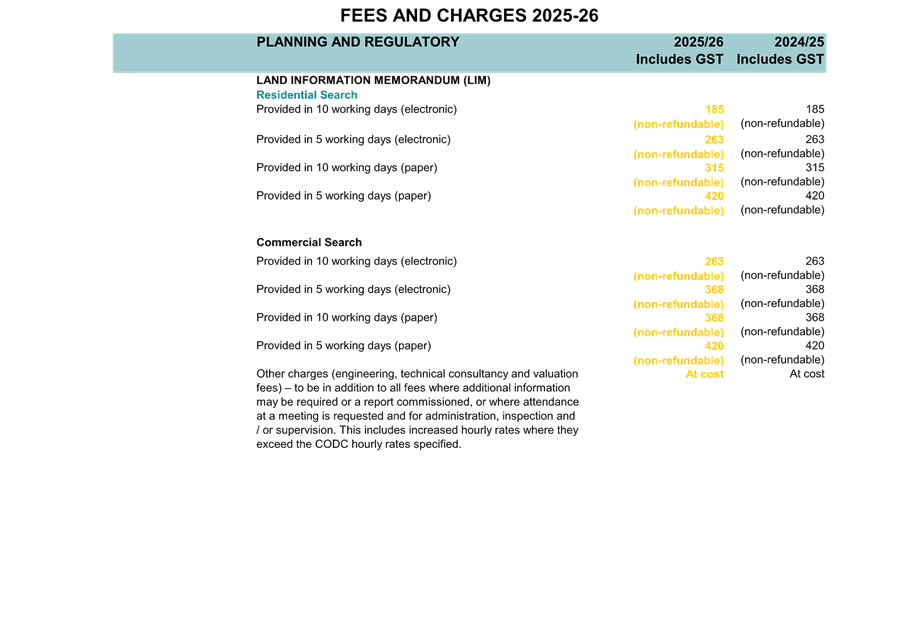

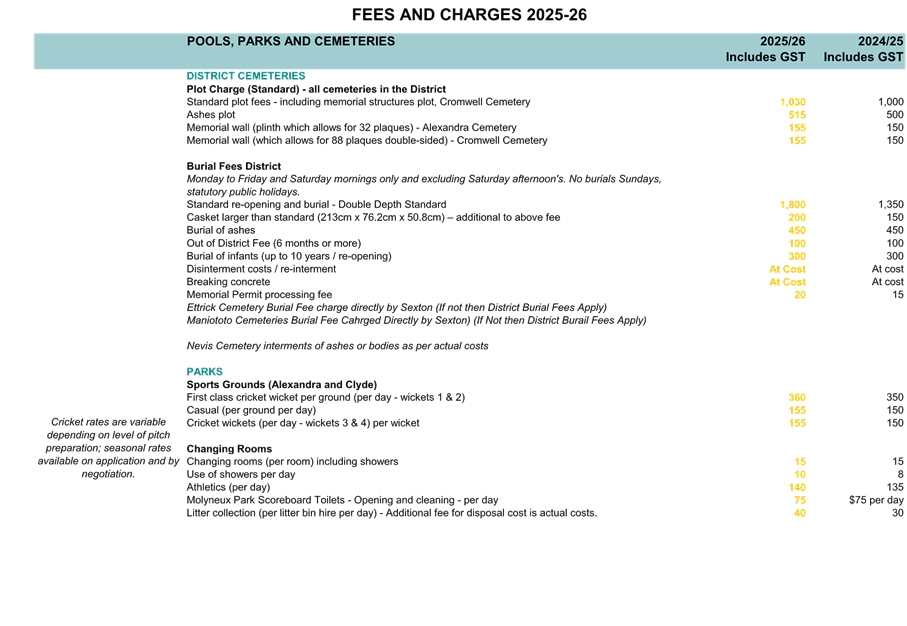

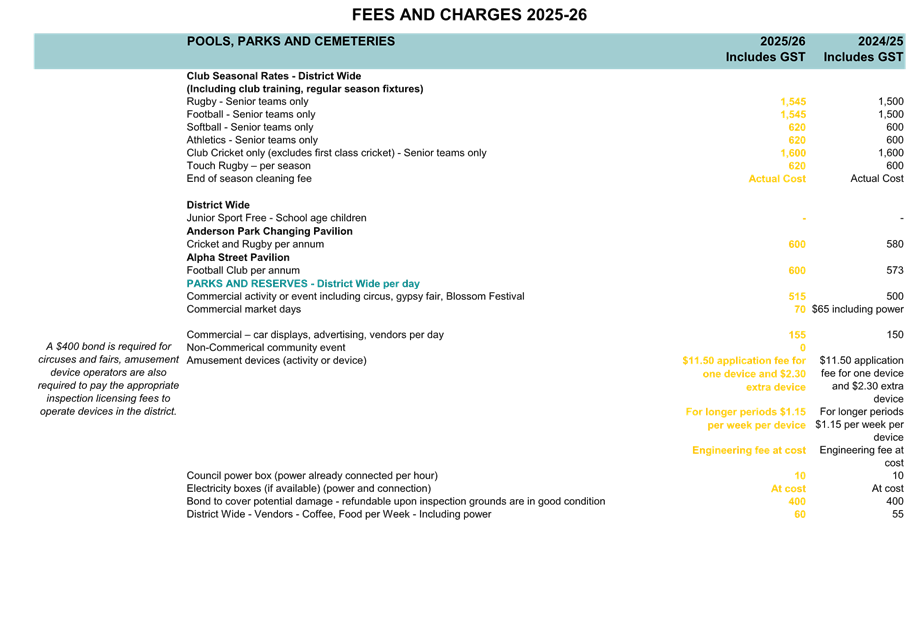

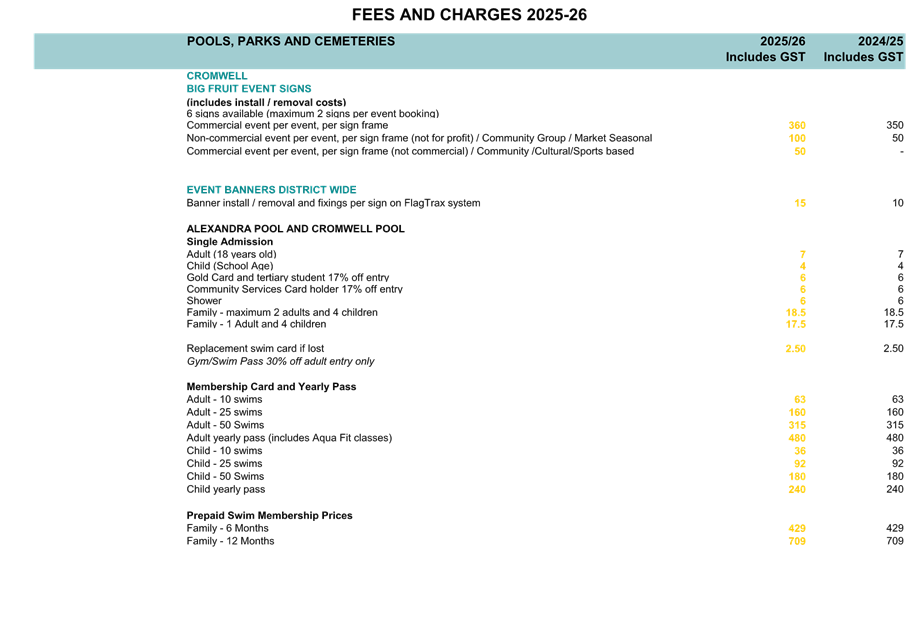

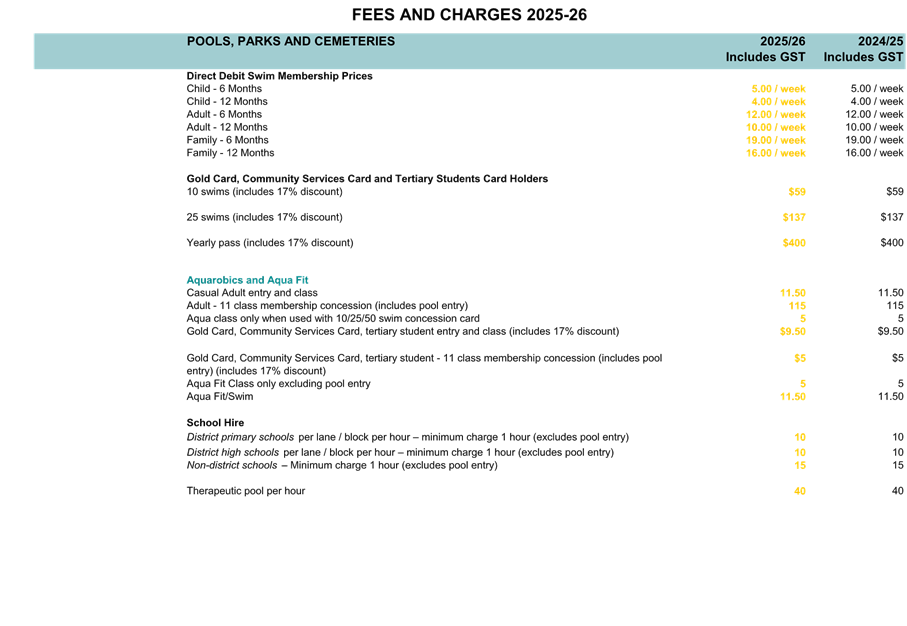

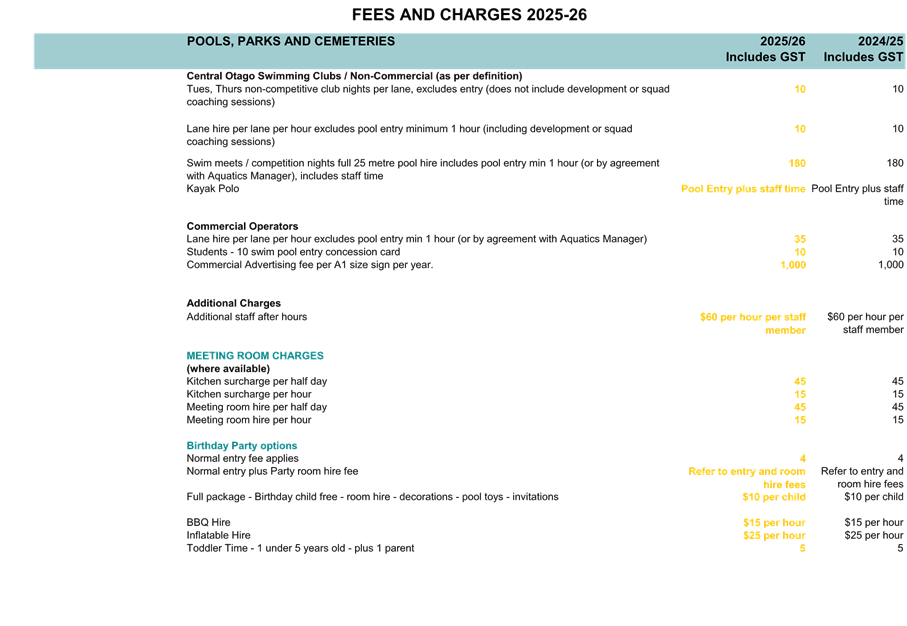

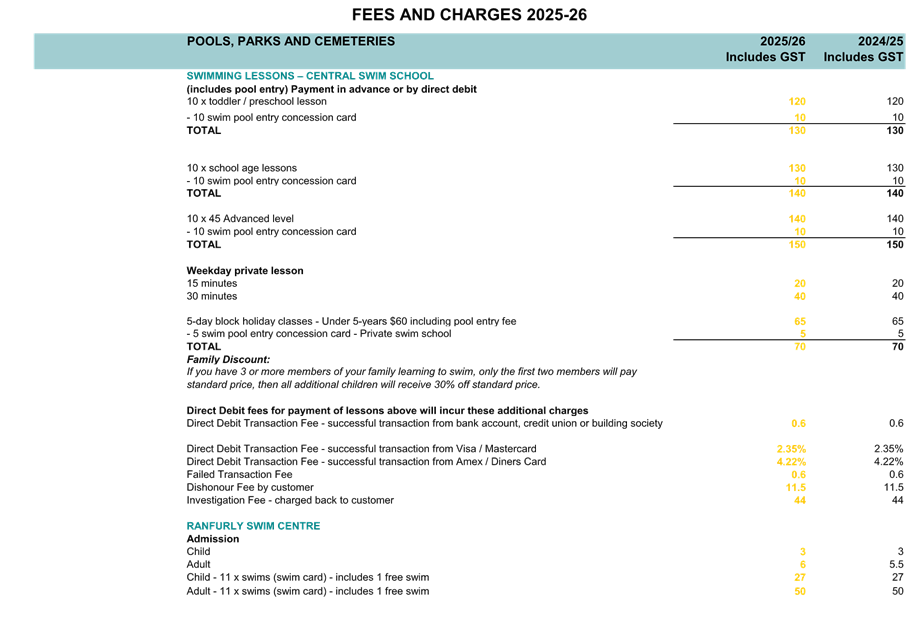

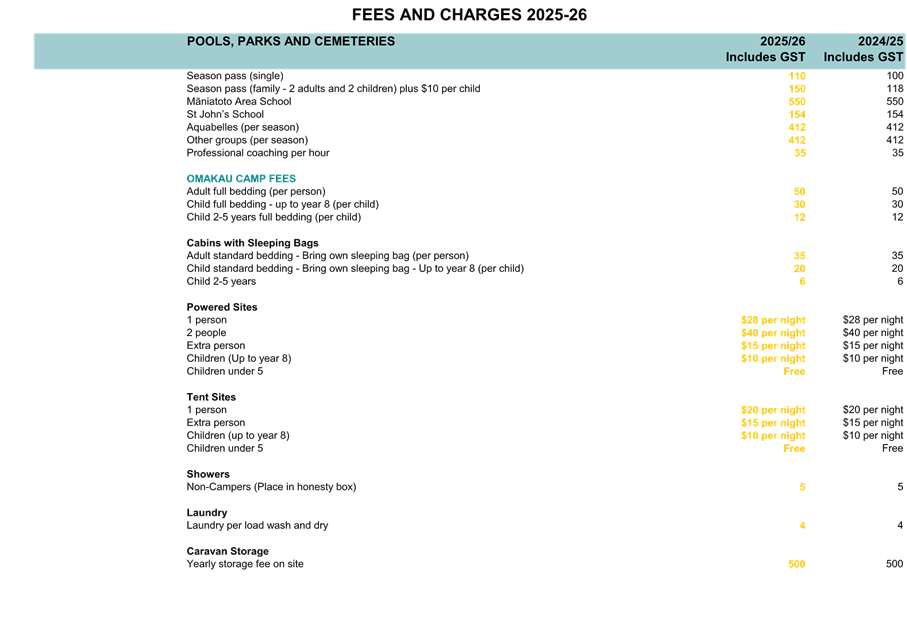

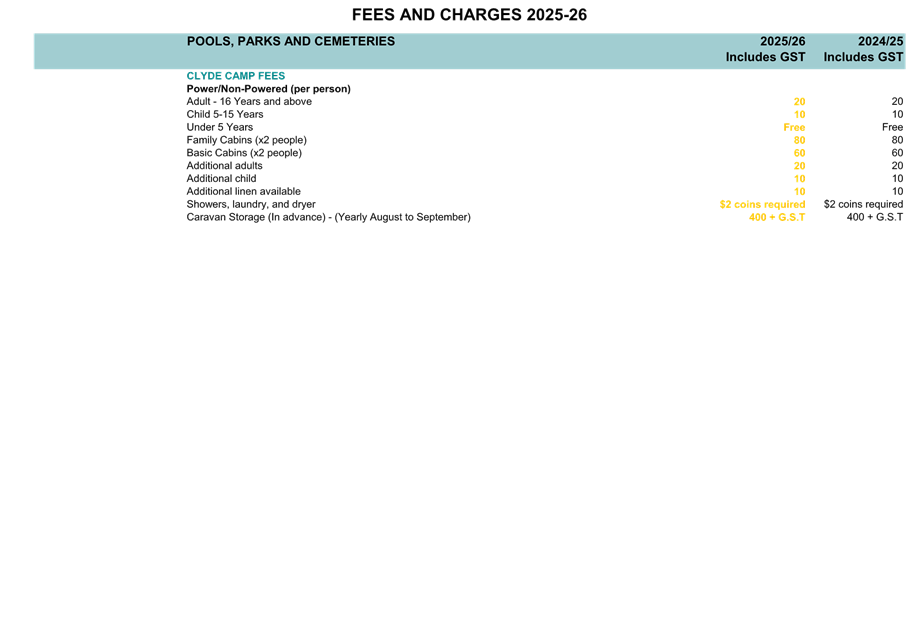

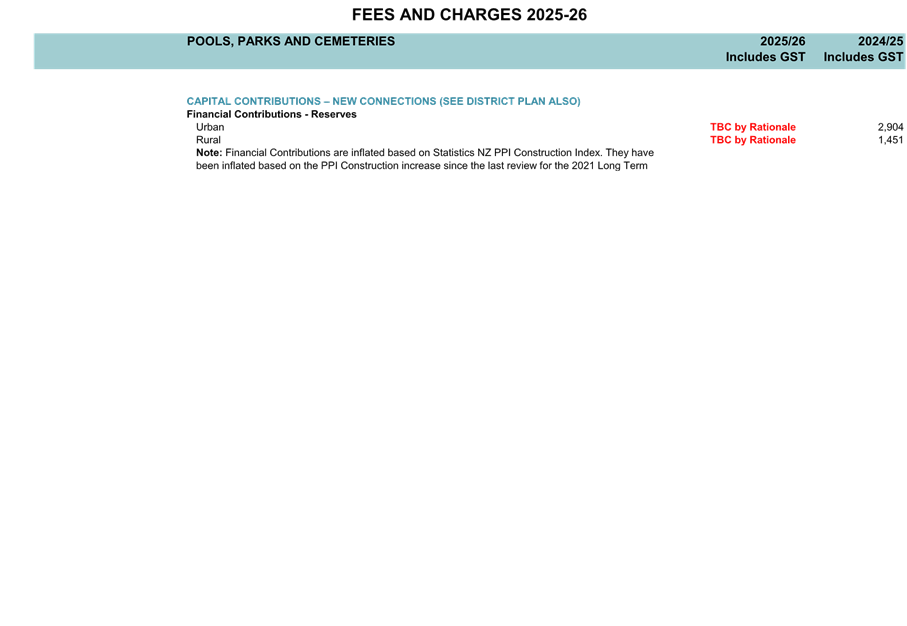

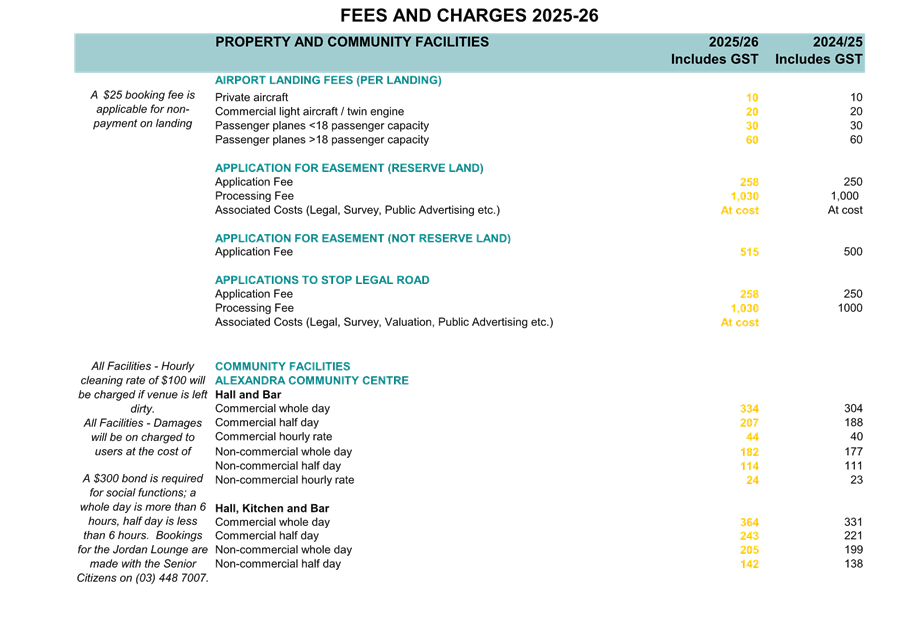

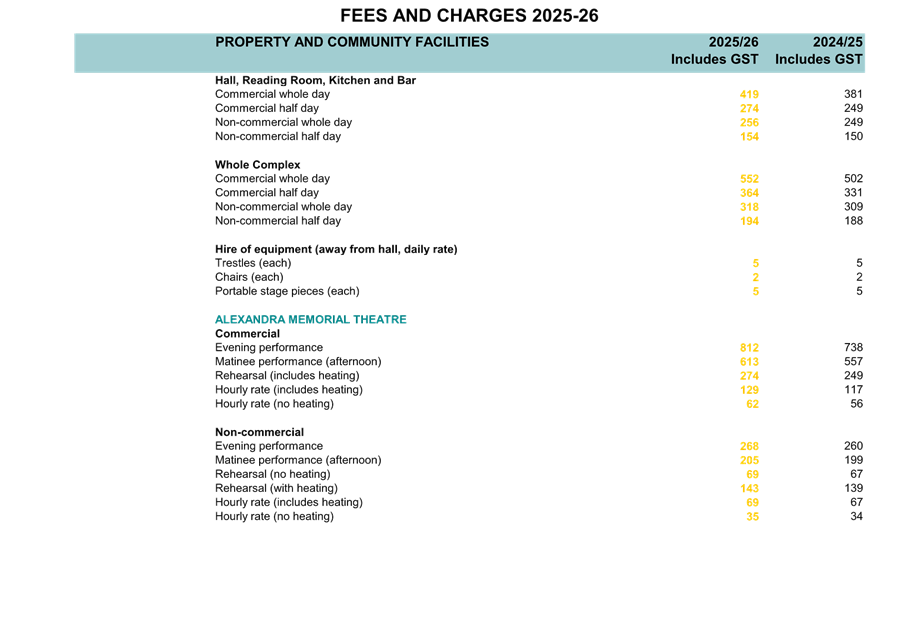

Appendix 5 - Fees and Charges

Schedule ⇩

Appendix 6 - Significance and

Engagement Policy ⇩

Appendix 7 - Revenue and Financing

Policy ⇩

Appendix 8 - Rates Remission and

Postponement Policy ⇩

Appendix 9 - Liability Management

Policy ⇩

Appendix 10 - Investment

Policy ⇩

Appendix 11 - Community

Outcomes ⇩

Appendix 12 - Significant

Forecasting Assumptions and Risks ⇩

Appendix 13 - Prospective

Financial Statements and Funding Impact Statements ⇩

Appendix 14 - Capital

Expenditure for Activity Groups ⇩