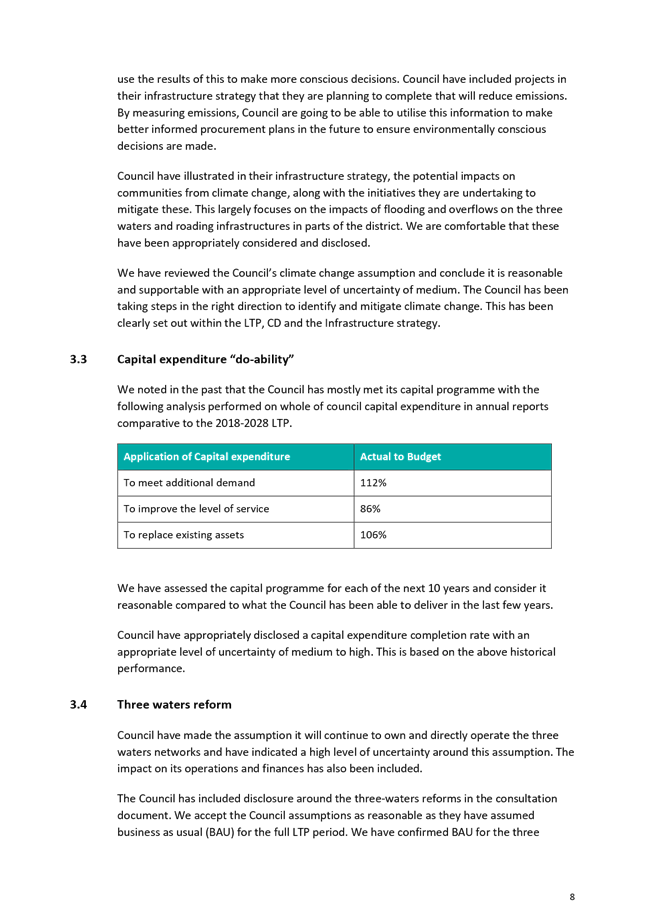

|

|

|

AGENDA

Audit and Risk Committee Meeting

Friday, 4 June 2021

|

|

Date:

|

Friday, 4 June 2021

|

|

Time:

|

9.30 am

|

|

Location:

|

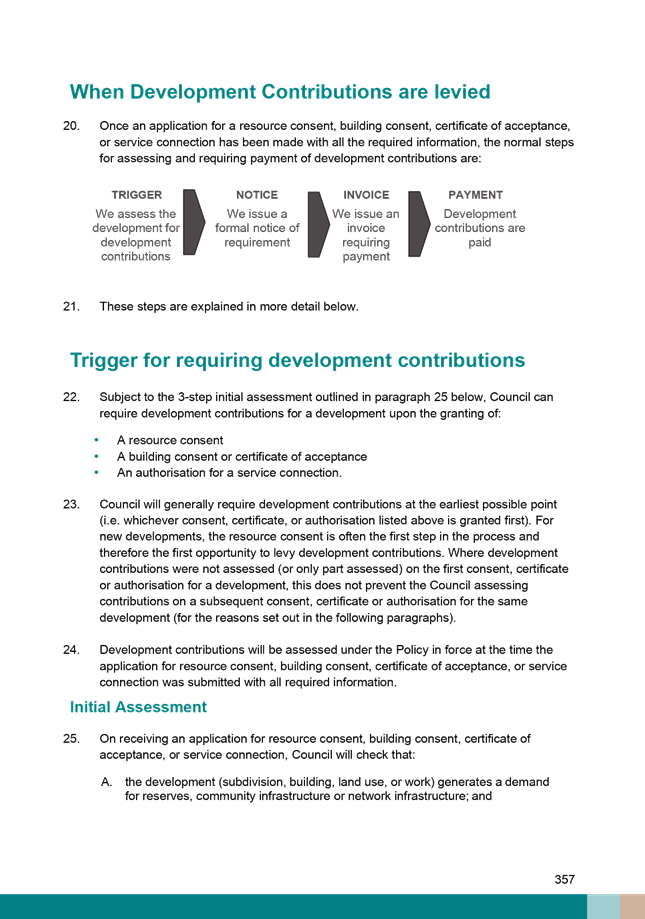

Ngā Hau e Whā, William Fraser Building,

1 Dunorling Street, Alexandra

|

|

(Unless Central Government changes COVID-19

meeting restrictions before then,

in which case it will be held

electronically using Microsoft Teams and livestreamed)

Sanchia Jacobs

Chief Executive Officer

|

Members Ms

L Robertson (Chair), His Worship the Mayor T Cadogan, Cr N Gillespie, Cr S Jeffery,

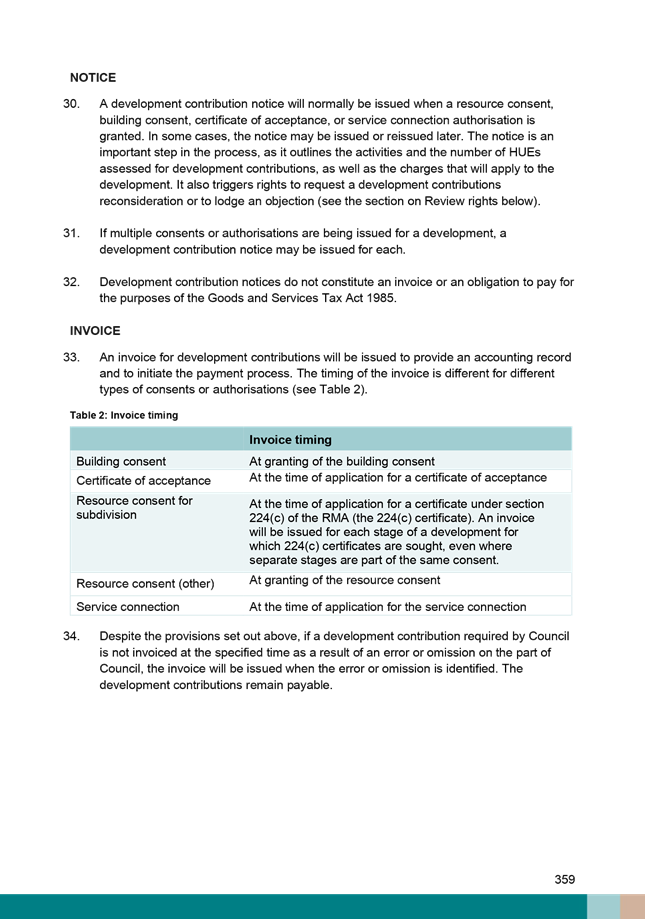

Cr N McKinlay,

In Attendance S Jacobs (Chief

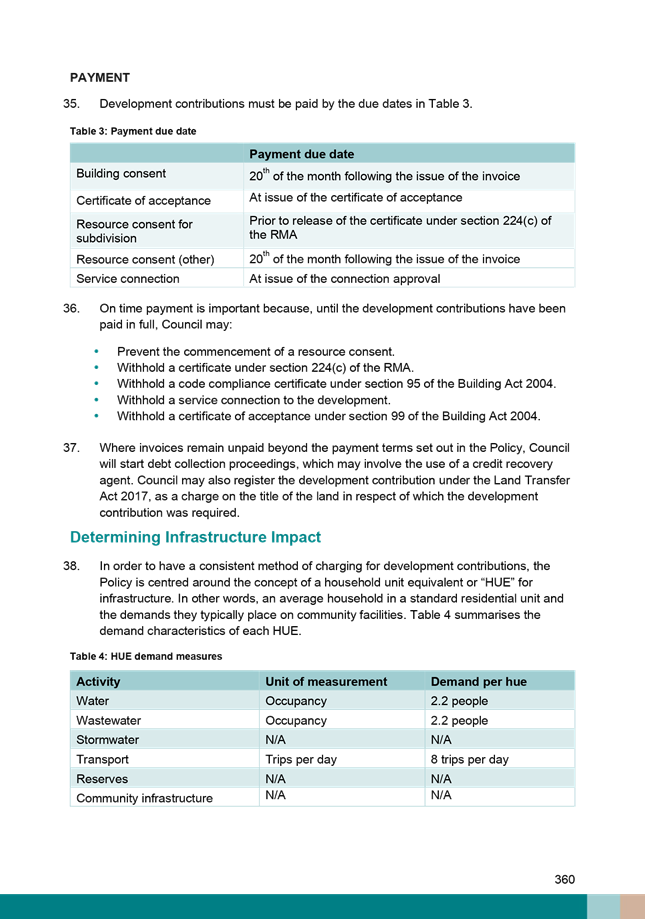

Executive Officer), L Macdonald (Executive Manager - Corporate Services), J

Muir (Executive Manager - Infrastructure Services), L van der Voort (Executive

Manager - Planning and Environment), S Righarts (Chief Advisor), G McFarlane

(Business Risk and Procurement Manager), R Williams (Governance Manager)

1 Apologies

An apology has been received from

Cr Gillespie.

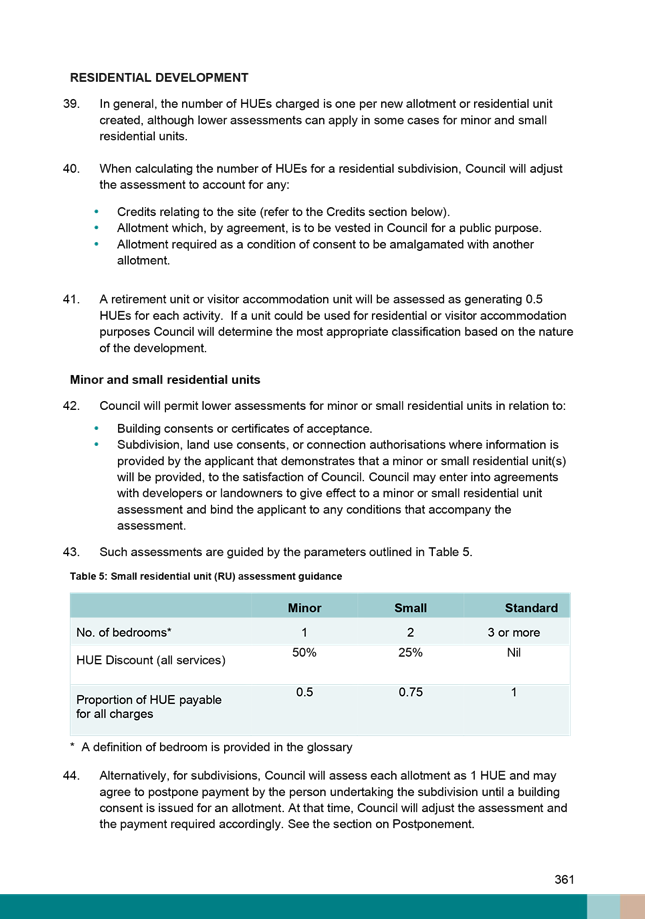

2 Public

Forum

3 Confirmation

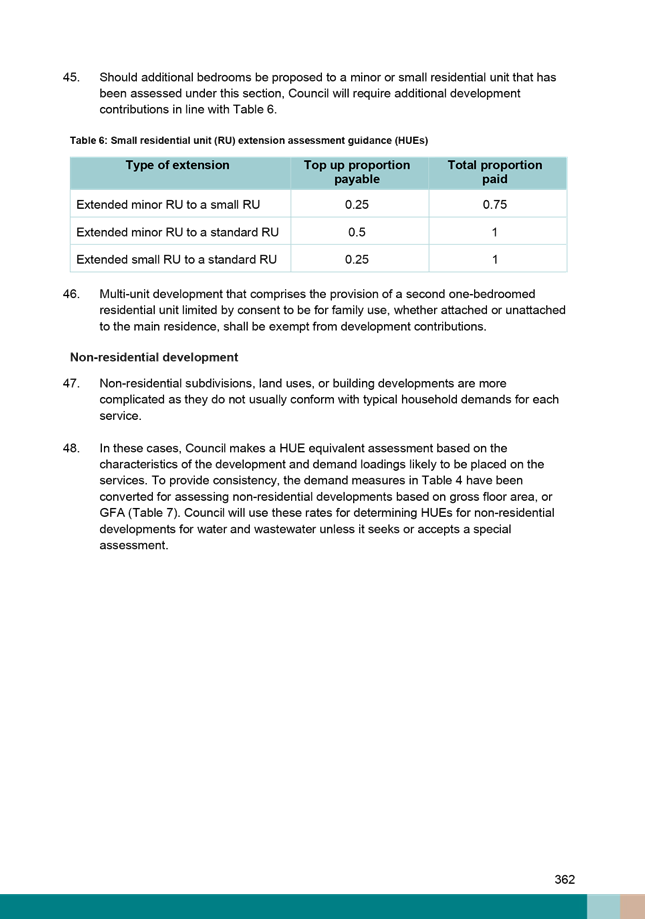

of Minutes

Audit and Risk Committee meeting -

24 February 2021

|

Audit and Risk Committee Agenda

|

4 June 2021

|

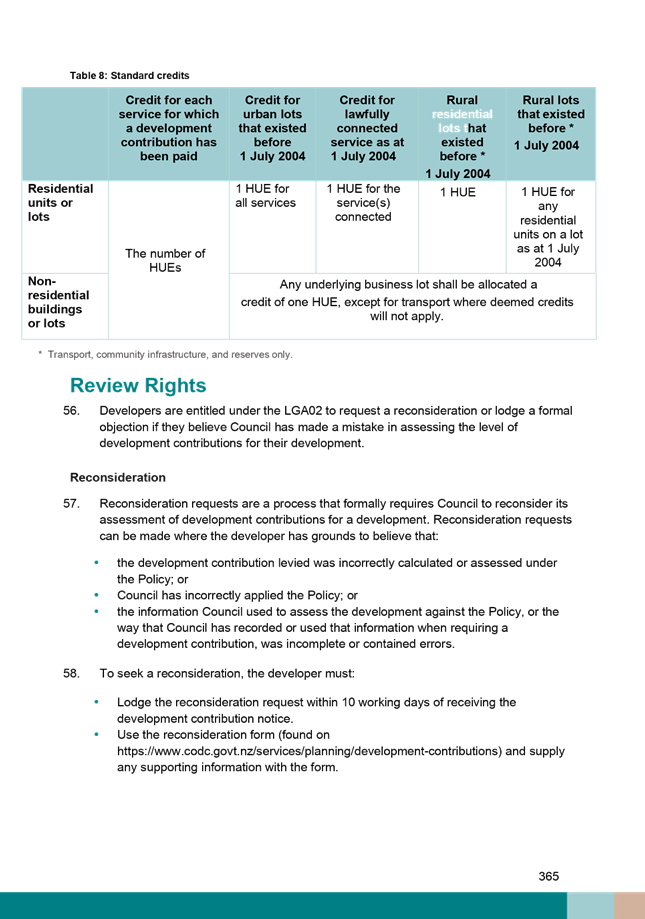

MINUTES

OF A MEETING OF THE Central Otago

District Council’s Audit and Risk Committee, HELD IN Ngā Hau e Whā, William

Fraser Building, 1 Dunorling Street, Alexandra ON Wednesday, 24 February 2021 AT

9.33 am

PRESENT: Ms

L Robertson (Chair), Cr N Gillespie, Cr S Jeffery, Cr N McKinlay

IN

ATTENDANCE: Cr T Paterson, S Jacobs (Chief Executive Officer), L

Fleck (Executive Manager – People and Culture), L Macdonald (Executive

Manager - Corporate Services), J Muir (Executive Manager - Infrastructure

Services), L van der Voort (Executive Manager - Planning and Environment), S

Righarts (Chief Advisor), G McFarlane (Business Risk and Procurement Manager),

K McCulloch (Corporate Accountant), D McKewen (Accountant), E Aucherlonie

(Project Manager) and R Williams (Governance Manager)

1 Apologies

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That apologies from His Worship the Mayor T Cadogan and Cr

T Alley be received and accepted.

Carried

|

2 Public

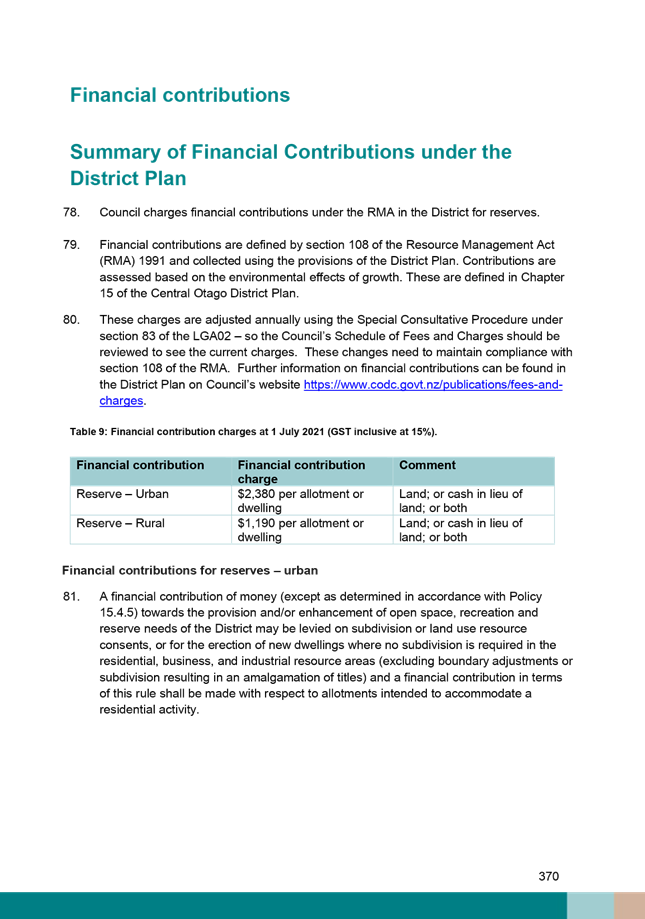

Forum

There was no public forum.

3 Confirmation

of Minutes

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That the minutes of the Audit and Risk Committee meeting

held on 14 December 2020 be confirmed as a true and correct record.

Carried

|

4 Declaration

of Interest

Members were reminded of their obligations in respect of

declaring any interests. There were no further declarations of interest.

5 Reports

for Information

|

21.1.3 An

update on the preparation of the 2021-31 Long-term Plan

|

|

To provide an update on the

progress in developing the 2021-31 Long-term Plan.

|

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That the report be received.

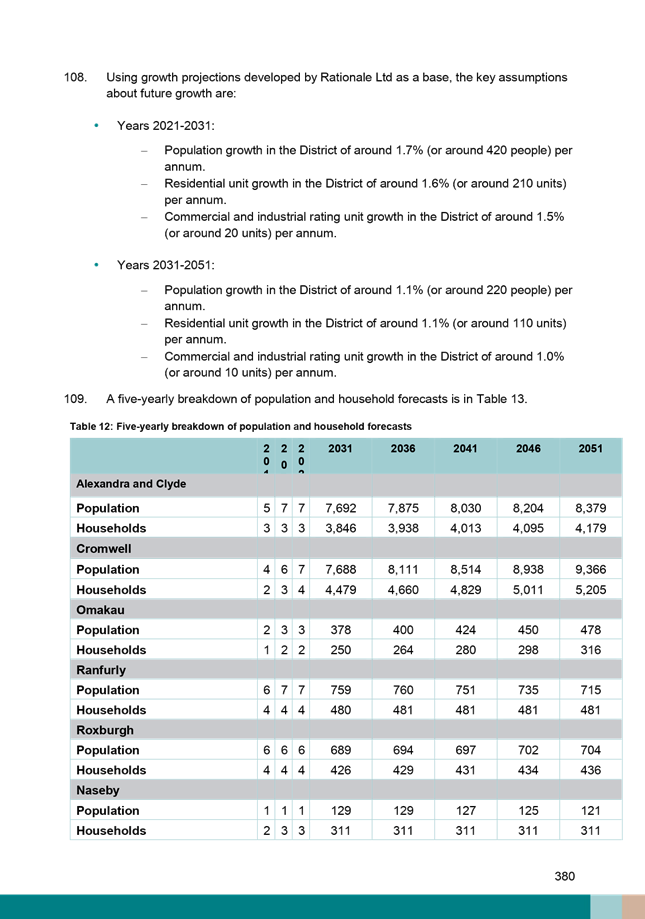

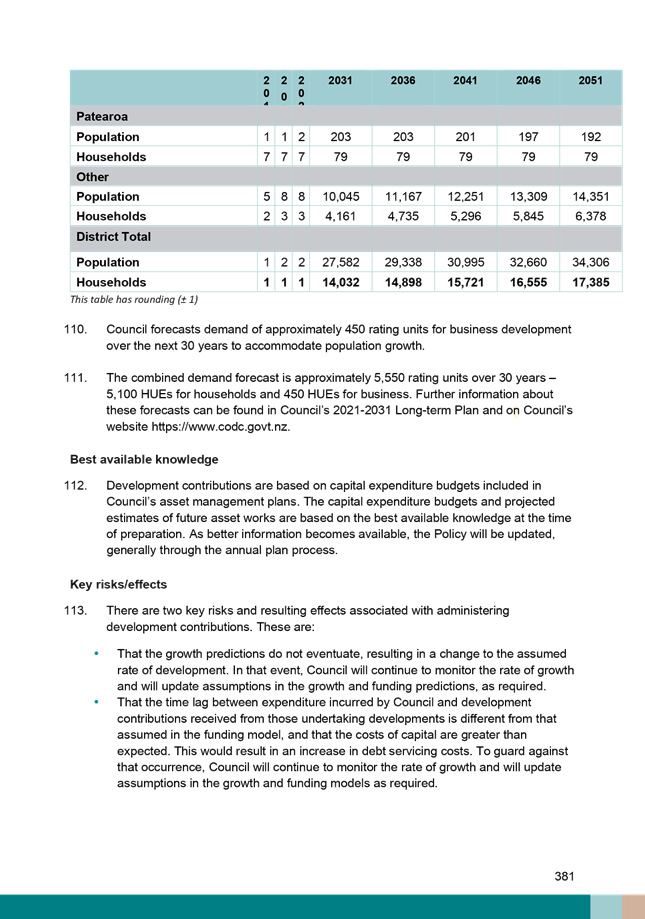

Carried

|

|

21.1.4 Policy

and Strategy Register

|

|

To present an updated register

of council’s policies and strategies.

|

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That the report be received.

Carried

|

|

21.1.5 Audit

NZ and Internal Audit Update

|

|

To update the Committee on the

status of the internal audit programme and any outstanding actions for

completed internal and external audits.

|

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That the Audit and Risk Committee receives the report.

Carried

|

|

21.1.6 Risk

Management Update

|

|

To consider the Risk Management

update.

|

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That the report be received.

Carried

|

|

21.1.7 Procurement

Update

|

|

To provide an update on

procurement activities at Central Otago District Council.

|

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That the report be received.

Carried

|

|

21.1.8 Financial

Report for year ending 31 December 2020

|

|

To consider the financial

performance for the period ending 31 December 2020.

|

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That the report be received.

Carried

|

|

21.1.9 Health

Safety and Well-being Report

|

|

To provide information on key

health and safety risks and the measures in place to mitigate those risks at

the Central Otago District Council.

|

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That the Committee receives the report.

Carried

|

6 Chair's

Report

|

21.1.10 Chair's

Report

|

|

The Chair advised that she would

be undertaking an evaluation of the performance of the Committee and would

seek input from the members, observers and the executive team. A report back

would be provided to the June meeting.

|

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That the report be received.

Carried

|

7 Members'

Reports

|

21.1.11 February

Members' Reports

|

|

It was noted that the June

meeting would mark the midpoint of the triennium and that the two observers

on the Committee would change from Crs Alley and Paterson to Crs Cooney and

Laws. The Chair acknowledged Crs Alley and Paterson’s participation

on the Committee.

|

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That the reports be received.

Carried

|

8 Status

Reports

|

21.1.12 February

Governance Report

|

|

To consider the legacy status

reports from previous meetings.

|

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That the report be received.

Carried

|

9 Date

of The Next Meeting

The date of the next scheduled meeting is 4

June 2021. Cr Gillespie noted that he would be an apology for that

meeting.

10 Resolution

to Exclude the Public

|

Committee Resolution

Moved: Robertson

Seconded: Gillespie

That the public be excluded from the following parts of

the proceedings of this meeting.

The general subject matter of each matter to be considered

while the public is excluded, the reason for passing this resolution in

relation to each matter, and the specific grounds under section 48 of the

Local Government Official Information and Meetings Act 1987 for the passing

of this resolution are as follows:

|

General subject of each matter to be

considered

|

Reason for passing this resolution in

relation to each matter

|

Ground(s) under section 48 for the

passing of this resolution

|

|

21.1.13 - Confirmation of Non-Public

Minutes from the Previous Meeting

|

s7(2)(a) - the withholding of the information is

necessary to protect the privacy of natural persons, including that of

deceased natural persons

s7(2)(c)(ii) - the withholding of the information

is necessary to protect information which is subject to an obligation of confidence

or which any person has been or could be compelled to provide under the

authority of any enactment, where the making available of the information

would be likely otherwise to damage the public interest

s7(2)(d) - the withholding of the information is

necessary to avoid prejudice to measures protecting the health or safety of

members of the public

s7(2)(i) - the withholding of the information is

necessary to enable Council to carry on, without prejudice or disadvantage,

negotiations (including commercial and industrial negotiations)

|

s48(1)(a)(i) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

21.1.14 - Cromwell Pool Update

|

s7(2)(d) - the withholding of the information is

necessary to avoid prejudice to measures protecting the health or safety of

members of the public

|

s48(1)(a)(i) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

21.1.15 - Lake Dunstan Water Supply

Project Audit - Implementation Plan

|

s7(2)(a) - the withholding of the information is

necessary to protect the privacy of natural persons, including that of

deceased natural persons

|

s48(1)(a)(i) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

21.1.16 - Litigation Report

|

s7(2)(g) - the withholding of the information is

necessary to maintain legal professional privilege

|

s48(1)(a)(i) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

|

21.1.17 - February 2021 Confidential

Governance Report

|

s7(2)(c)(ii) - the withholding of the information

is necessary to protect information which is subject to an obligation of

confidence or which any person has been or could be compelled to provide

under the authority of any enactment, where the making available of the

information would be likely otherwise to damage the public interest

s7(2)(d) - the withholding of the information is

necessary to avoid prejudice to measures protecting the health or safety of

members of the public

|

s48(1)(a)(i) - the public conduct of the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding would exist

under section 6 or section 7

|

Carried

|

The public were excluded at 10.42

am and the meeting closed at 11.13am.

4 Declaration

of Interest

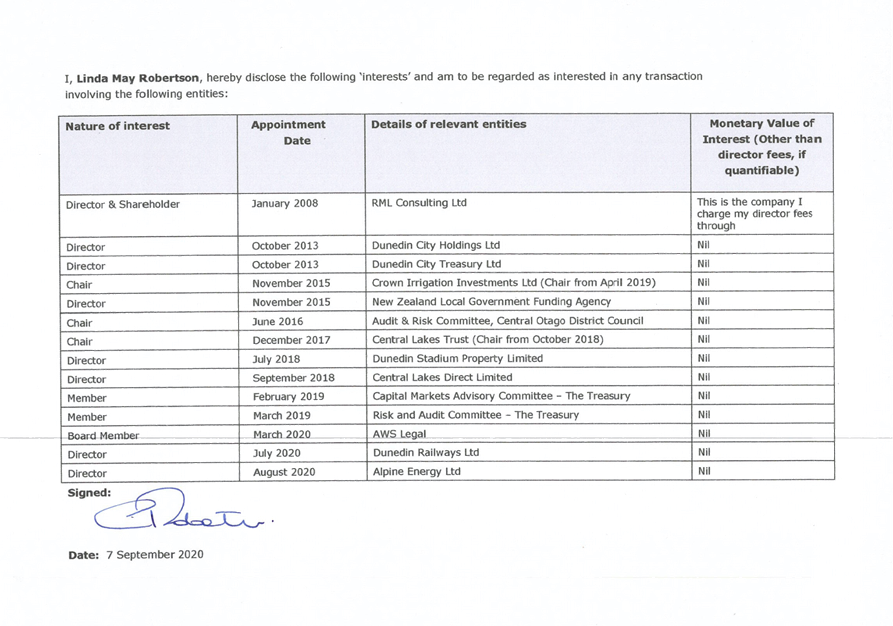

21.2.1 Declarations

of Interest Register

Doc ID: 532765

1. Purpose

Members are reminded of the need to be vigilant to stand

aside from decision making when a conflict arises between their role as a

member and any private or other external interest they might have.

2. Attachments

Appendix 1 - Declarations of

Interests ⇩

|

Audit

and Risk Committee meeting

|

4 June

2021

|

5 Reports

for Decisions

21.2.2 Audit

NZ and Internal Audit Update

Doc ID: 534574

1. Purpose of Report

To provide an update on the status of the internal audit

programme and any outstanding actions for completed internal and external

audits.

|

Recommendations

That the Audit and Risk Committee receives the report.

|

2. Background

Council has a legislative requirement to

complete external audits of annual reports through Audit New Zealand. Audit New

Zealand complete a governance report on their findings and any recommendations

for improvements. A schedule of actions is then created and allocated to

staff to manage the completion of these recommendations. The 2019-2020 Audit

New Zealand Management Report has been released, and once this has been

presented to the Committee at the June Audit and Risk meeting, any outstanding

actions will be transferred to the attached register.

The 2018-2019 Audit New Zealand Management

Report has one remaining action item.

In addition to external audits, council

carries out several internal audits a year to provide assurance over compliance

and to mitigate business risks. The cash-handling audit has been completed and any

outstanding actions will also be transferred to the attached resister.

The GST audit has been completed and will be reported on once Deloitte’s

have finalised their findings.

3. Discussion

Both internal and external audits result in

recommendations where council can make improvements. Staff create a register of

tasks associated with these recommendations and assign a staff member to manage

the implementation. Appendix 1 and 2 list the outstanding tasks and any

progress with these tasks. Once the Committee have viewed the completed tasks

these are removed from the schedule.

Currently the internal audit schedule has

five tasks remaining in progress and is on track to complete these within the scheduled

timeframe.

The following attachments include a status

update on the actions resulting from the auditors’ recommendations.

4. Attachments

Appendix 1 - Audit New Zealand -

Audit Action Register ⇩

Appendix 2 - Internal Audit Action

Register ⇩

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Gabi

McFarlane

|

Leanne

Macdonald

|

|

Risk and

Procurement Manager

|

Executive

Manager - Corporate Services

|

|

18/05/2021

|

25/05/2021

|

|

Urgent

|

Necessary

|

Beneficial

|

Assigned

|

Estimated Completion

|

Status

|

Comments

|

|

Audit NZ 2019 Management Report

|

|

|

|

|

|

|

|

|

Asset valuation recommendations and

processes (4.1)

|

|

|

|

|

|

|

|

|

Management should review and address the

asset valuation recommendations made by the District Council's valuer.

The valuation reports for both the roading and the 3-waters asset classes

made several recommendations for improvement opportunities. In reviewing the

valuation reports we concur with the valuer’s recommendations and have

noted the more significant recommendations below.

|

|

ü

|

|

Executive Manager - Infrastructure

Services and Executive Manager - Corporate Services

|

|

In progress

|

Bridges are contained within the RAMM

database, but are valued outside of RAMM as there are not standard rates that

can be used due to the varying materials used for bridge components, and the

different lives for these. Each bridge needs to be assessed by a structural

engineer and valued individually. This will be done again for the 2020

Activity Management Plan. The replacement options will also be confirmed

during the development of the 2020 bridge strategy, which also forms part of

the 2020 Activity Management Plan. Longer term the roading industry is considering

the development of a more specific bridge asset database for use in the New

Zealand environment.

A project is currently underway to enable component information to be

collected for water treatment sites. This will enable more accurate

valuations to be undertaken from 2020.

The engagement of valuers for the 2018/2019 valuation was delayed, until the

issues relating to the previously unaccepted 2017 valuation could be

clarified. The valuations are a costly process, and it was not financially

prudent to continue with these until the outstanding issues had been cleared

with Audit NZ. This has now occurred, and no delays are anticipated with

future valuations.

For the 2019/20 year the finance and Infrastructure staff created a timetable

for the valuation of each activity which is reviewed on an annual

basis. This improved the process somewhat. 2019/20 was the first time

since the asset management process was updated where parks, reserves and

pools assets have been revalued. Audit New Zealand were not expecting this,

as the revaluation cycle falls outside of the three-year cycle and so was

missed off their schedule. This contributed to increased audit fees.

Council planned to do the land and building valuation in 202/21 however with

the growth Council has been facing it was decided to do this in 2019, which

caused some delays for Audit New Zealand as well.

|

|

Roading – the valuer made assumptions

around installation dates for certain assets, as the construction date

information was not recorded in RAMM. It is recommended that management

review and update the dates for the next valuation. We note that management

has performed some work already to address this, identifying that some relate

to assets constructed as part of the Cromwell relocation when the Clyde Dam

was constructed.

|

|

|

|

|

|

|

|

Roading

– bridge assets were revalued outside of RAMM and it was recommended

these assets should be moved to RAMM. In addition it was identified that some

bridges may not be replaced at the end of their useful lives and the District

Council should consider this as part of its Bridging Strategy.

|

|

|

|

|

|

|

|

3-Waters – the valuers noted that detailed

component information for new plant projects completed since the previous

valuation, have not been included in the plant asset register. Instead, high

level project costs have been used.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Annual report preparation process (4.2)

|

|

|

|

|

|

|

|

|

Council should introduce a robust

internal quality review process over the draft annual report to improve the

quality of the draft information provided for audit.

|

|

ü

|

|

Executive Manager - Corporate Services /

Finance Manager

|

|

Ongoing

|

Preparation for the Annual Report has

been completed for 2019-20. For the first few weeks we had a more

experienced team and have met our internal timetable. We also requested

that Audit NZ meet their timeline. During the later part of the audit we lost

two key staff which created challenges for CODC and Audit NZ also struggled

with timelines due to reduced staff and delays across the councils due to

COVID-19 disclosures. While there were improvements, there is still

room for further improvement.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Processing of NZTA claims (4.4)

|

|

|

|

|

|

|

|

|

The NZTA claims are submitted on a

timelier basis, for example monthly.

|

|

ü

|

|

Executive Manager - Infrastructure

Services

|

|

Complete

|

The submission of NZTA claims was

sporadic due to changes in Roading Management. This task has now been

re-assigned and claims have been submitted monthly for 2019/20.

|

|

|

|

|

|

|

|

|

|

|

2017 Management Report

|

|

|

|

|

|

|

|

|

Review of general ledger reconciliations

|

|

|

|

|

|

|

|

|

We recommend that general ledger

reconciliations (e.g. bank, debtors and creditors) be independently reviewed,

dated and evidenced as such.

|

|

ü

|

|

Executive Manager - Corporate Services /

Finance Manager

|

|

Complete

|

General ledger reconcilations are being

digitally reviewed, dated and evidence provided.

|

|

|

|

|

|

|

|

|

|

|

2015 Management Report

|

|

|

|

|

|

|

|

|

Independent review of journals

|

|

|

|

|

|

|

|

|

We recommend, as best practice,

implementation of procedures to ensure that all journals posted into the

financial system have been reviewed and are complete.

|

|

ü

|

|

Executive Manager - Corporate Services /

Finance Manager

|

|

Complete

|

Journals and supporting documentation

are prepared by a member of the finance team and then reviewed by the Finance

Manager. Before posting journals, the finance team is ensuring appropriate

supporting documentation or narrative is provided and that the journal is

correctly coded. This is all provided to the Finance Manager who reviews the

documents and signs a monthly journal checklist form.

|

|

Audit and Risk Committee meeting

|

4 June 2021

|

|

Detailed Findings: Accounts Payable, Payroll and Information

Security Risk Review

|

|

Description

|

Detail

|

Risk Rating

|

Recommendation

|

Status

|

Due Date

|

Person Responsible

|

Any additional Comments

|

|

Payroll

|

|

Enhancement required for manual

timesheets

|

Central Otago District Council has both

waged and salaried employees. Timesheets for waged employees are manually

entered into the Pay Global system.

|

Moderate

|

Implementing an automated process of

capturing the time worked by the waged staff will increase efficiency and

reduce the possibility of errors.

|

In progress

|

1/03/2021 - move

to 31 July 2021

|

Finance Manager

|

Libraries are up and running. . Pay

Global, Payroll Software company has finished the summary report, which we

needed to complete pools. Pools should be finalised end of July 2021

We will not be 100% automated because any salary staff that works extra hours

is entered manually into the system.

|

|

Improvements required with respect to

payroll guidelines

|

Central Otago District Council does not

have an approved procedures manual in place.

|

Process Improvement

|

Consolidates and formalises the payroll

procedures manual and the desk profile process document.

|

In progress

|

Jun-21

|

Payroll Officer

|

The Payroll Officer has created an

informal step-by step guide, this needs to be consolidated.

|

|

Cyber Security Improvement Programme

update

|

|

Implement a register of all cloud

services and ensure termination of these services at the time of staff member

leaves council.

|

Immediately implement processes whereby

Human Resources are required to provide timely notice of staff enrolments and

departures. In association with this, implement a register of all cloud

services used by council staff members to ensure that access to these

services is terminated at the time a staff member ceases to provide services

to the council.

|

Process Improvement

|

Recommendation made as part of People

and Protective Technologies roadmap to utilise the new firewall capability

and monitor Cloud App activity.

|

In progress

|

Dec. 2021

|

Information Services Manager

|

Technology has been deployed. We are

currently monitoring the Cloud services being utilised. To date, we have not

found any unknown Cloud services.

We have staff exiting processes in place for known Cloud services.

|

|

|

|

|

|

|

|

|

|

Implement information leakage controls

and removable media

|

Implement controls to restrict the

opportunity for information leakage via the internet and removable media

including the locking down of USB devices.

|

Low

|

Implement controls to restrict the

opportunity for information leakage via the internet and removable media

including the locking down of USB devices.

|

In progress

|

Dec. 2021

|

Information Services Manager

|

This has been added to the people and

protective technology roadmap for executive team decision.

|

|

Replace the current ad hoc procedures

and processes within the Information Services Department

|

Establish a programme to formalise and

document system procedures and processes to replace the current ad hoc

processes that may exist in the Information Services Department.

|

Process Improvement

|

Establish a programme to formalise and

document system procedures and processes to replace ad hoc processes.

|

In progress

|

Dec. 2021

|

Information Services Manager

|

These have started to be drafted and

will be completed this year. These processes are already in place, just not

documented.

|

21.2.3 Sensitive

Expenditure Policy

Doc ID: 534487

1. Purpose

of Report

To review and recommend to Council the adoption of the

Sensitive Expenditure Policy, the Travel Policy and the Credit Card Policy.

|

Recommendations

That the Audit and Risk Committee

A. Receives

the report and accepts the level of significance.

B. Recommends

to Council that they approve the Sensitive Expenditure Policy, the Travel

Policy and the Credit Card Policy.

|

2. Background

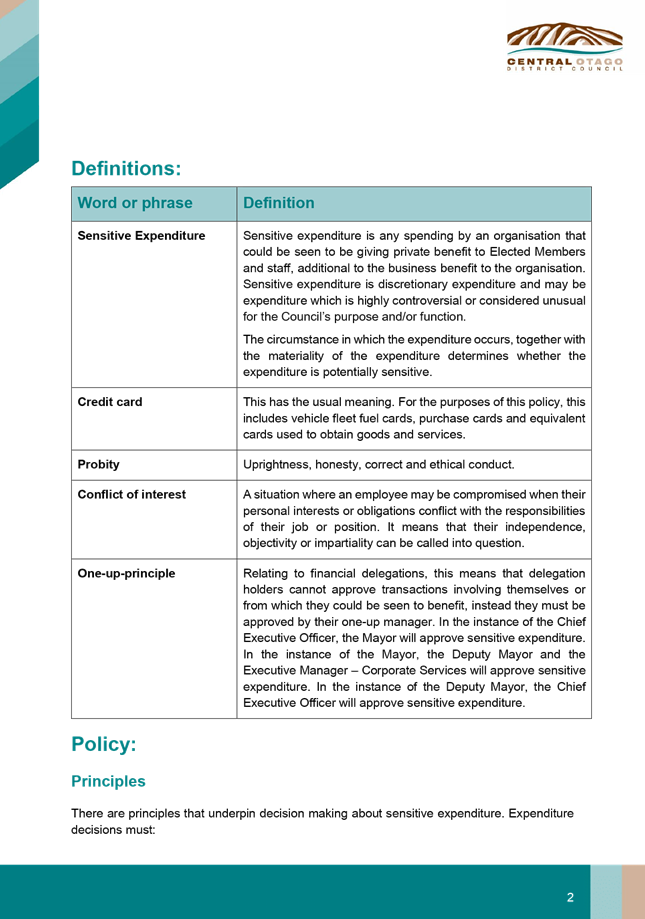

Council’s Sensitive Expenditure Policy has been

reviewed following the updated good practice guide on controlling sensitive

expenditure distributed by the Controller and Auditor-General.

As a result of this review, it was recommended that the

policy be revised and expanded, informing the creation of the Travel Policy and

the Credit Card Policy alongside the Sensitive Expenditure Policy.

Official Information Requests surrounding sensitive

expenditure and gifts are regularly received by Council, with spending

practices scrutinised by the public. Sensitive expenditure covers a broad range

of topics and it is important that both staff and elected members have clarity

and guidance surrounding these, often controversial, topics.

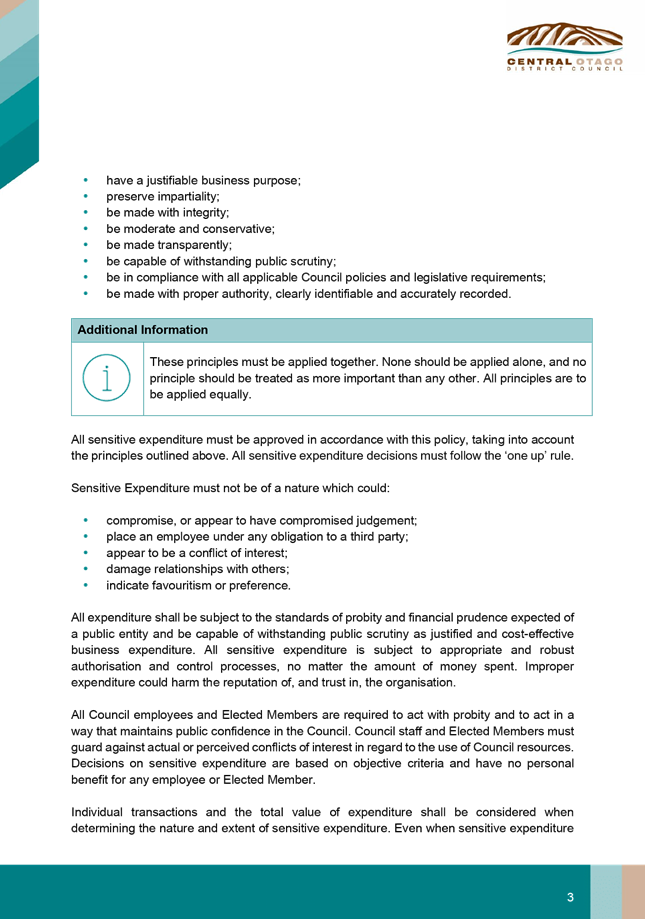

3. Discussion

The Controller and Auditor-General have provided updated

guidance around best practice, reinforcing the importance of performing in a

manner which stands up to public scrutiny. Issues of sensitive expenditure

arise often, and it is important that guidelines are in place and sensitive

expenditure is managed diligently and robustly.

The Sensitive Expenditure Policy, Travel Policy and Credit

Card Policy all provide practical guidance on specific types of expenditure and

outline principles for decision-making for situations which are not clear-cut.

Managing sensitive expenditure, and perceived sensitive expenditure, requires

good judgement, and these policies provide a guide from which to base

decisions.

There will be greater scrutiny on Sensitive Expenditure in

the coming years, and it is important that these documents are robust.

4. Options

Option 1 – (Recommended)

The Committee recommends to Council the adoption of the

Sensitive Expenditure Policy, the Travel Policy and the Credit Card Policy.

Advantages:

· Protects

Elected Members and Council staff by providing comprehensive guidance

surrounding sensitive expenditure

· Protects

Council’s reputation

· Reinforces

Council’s approach to appropriately managing risk

· Generates

awareness of the topic of Sensitive Expenditure

· Reinforces

a financial prudence approach

Disadvantages:

· None.

Option 2

The Committee retains the existing Sensitive Expenditure

Policy.

Advantages:

· None

Disadvantages:

· Lack

of guidance on sensitive expenditure

· Heighten

risk of public scrutiny on an item of importance

· Not

meeting the Controller and Auditor-General’s recommended best practice

5. Compliance

|

Local Government Act 2002 Purpose Provisions

|

This decision ensures the organisation conducts business in

an open, transparent and democratically accountable manner.

|

|

Financial implications – Is this decision consistent with

proposed activities and budgets in long term plan/annual plan?

|

Yes. The review of this policy,

and consequential creation of additional policies, have been conducted in

house and have not raised any financial implications. There are no costs

associated with the recommendation to adopt these policies.

Adequate guidance around sensitive expenditure will

reduce the likelihood of financial or reputational damage to Council.

|

|

Decision consistent with other Council plans and policies? Such as

the District Plan, Economic Development Strategy etc.

|

Yes. The suite of policies are a revision of the Sensitive

Expenditure Policy. The policies maintain consistency

with other Council policies and processes.

|

|

Considerations as to sustainability, the environment and climate

change impacts

|

There are no implications.

|

|

Risks Analysis

|

The existing policy is outdated.

Before the draft of these policies there was no clear and comprehensive

policy for travelling or the use of credit cards, which provides uncertainty

and therefore ineptness, leaving many aspects open for scrutiny and creating

a significant risk to the organisation. These policies reduce the risk to the

organisation.

For the mitigation of risk, these policies are

comprehensive, with the Travel Policy and Credit Card Policy being separated

out into standalone policies for the purposes of transparency and simplicity.

|

|

Significance, Consultation and Engagement (internal and external)

|

The changes proposed to the policy

are not significant and are therefore unlikely to generate community or media

interest.

No consultation

is required as this is not significant under the Significance and Engagement

Policy.

|

6. Next

Steps

The policy shall be taken to Council for adoption. Staff

will then be notified of the updated policy through the Council intranet.

7. Attachments

Appendix 1 - Sensitive Expenditure

Policy ⇩

Appendix 2 - Travel Policy ⇩

Appendix 3 - Credit Card Policy ⇩

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Gabi

McFarlane

|

Leanne

Macdonald

|

|

Risk and

Procurement Manager

|

Executive

Manager - Corporate Services

|

|

18/05/2021

|

24/05/2021

|

|

Audit

and Risk Committee meeting

|

4 June

2021

|

|

Audit and Risk Committee meeting

|

4 June

2021

|

|

Audit and Risk Committee meeting

|

4 June 2021

|

21.2.4 An

update on the preparation of the 2021-31 Long-term Plan

Doc ID: 535176

1. Purpose

To provide an update on the progress in developing the

2021-31 Long-term Plan.

|

Recommendations

That the report be received.

|

2. Discussion

Since the Committee’s last meeting on 24 February

2021, Council approved the consultation document and associated supporting

documents for public consultation. Public consultation occurred between 26

March and 25 April 2021. 852 submissions were received on topics contained in

the consultation document as well as other matters of interest to residents.

The four community boards have held their deliberations and made recommendations

to Council on matters pertaining to the respective wards. Council is

considering these recommendations alongside the content of all submissions at

their meeting on 1 and 2 June 2021. Audit New Zealand is due to be onsite from

the 8 June 2021 to conduct the final audit. The programme remains on

track for the final draft 2021-31 Long-term Plan to be presented at the 30 June

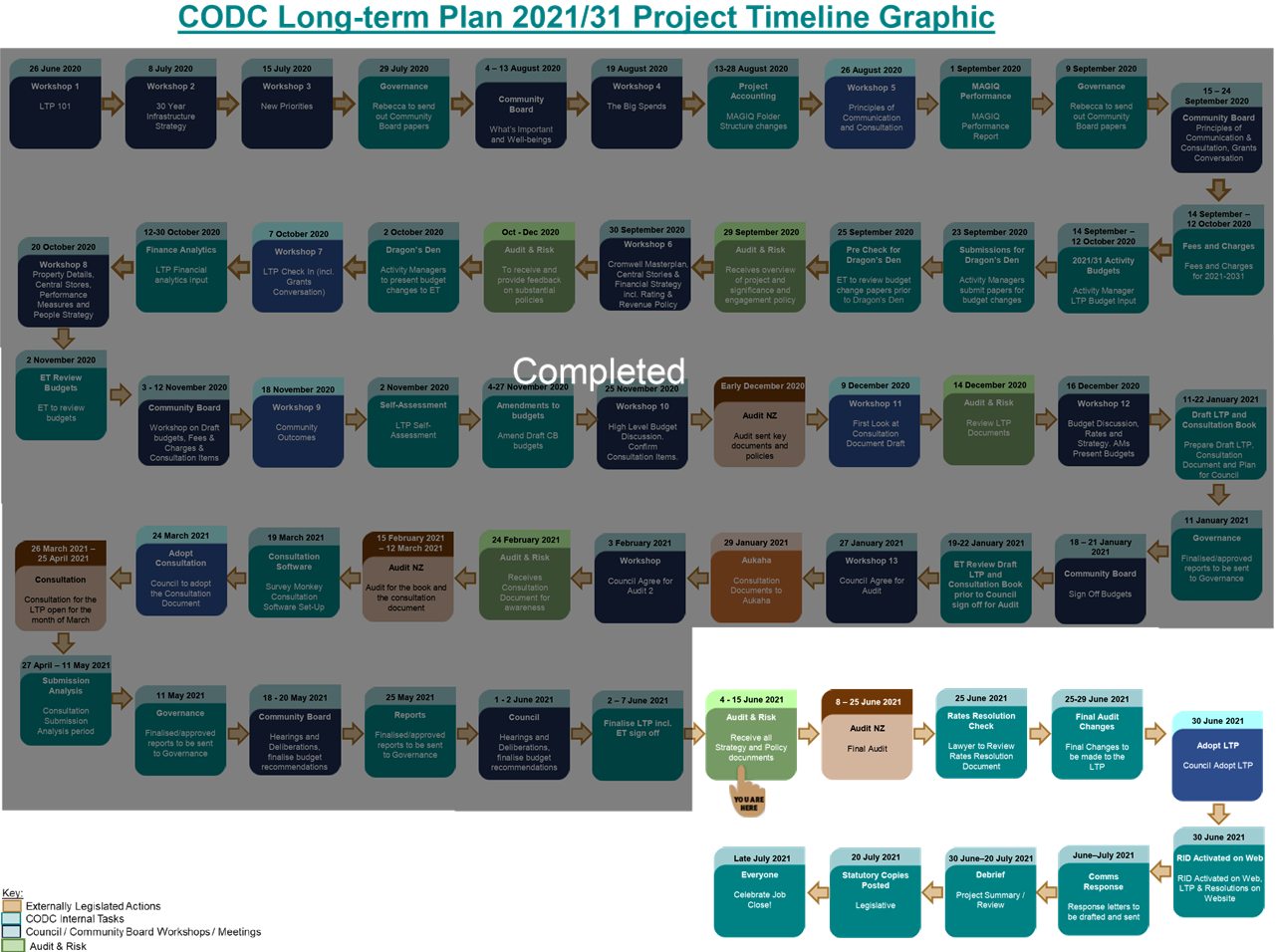

2021 Council meeting for adoption (see Appendix 1 for the 2021-31 Long-term

Plan timeline).

The Committee has considered the 2021-31 Long-term Plan

policies and strategies and provided feedback as they have been developed. At

the request of the Committee and for the sake of completeness attached is the

full suite of draft policies and strategies for the 2021-31 Long-term Plan

(refer to Appendix 2). Note that some sections are highlighted at the time of

writing as they may change depending on the outcome of Council’s

deliberations on 2 June 2021 and to advise Audit New Zealand of changes since

the February 2021 audit.

3. Attachments

Appendix 1 - 2021-31 Long-term

Plan Project Timeline ⇩

Appendix 2 - Draft 2021-31

Long-term Plan Strategies and Policies.pdf ⇩

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Saskia

Righarts

|

Sanchia

Jacobs

|

|

Chief

Advisor

|

Chief Executive

Officer

|

|

12/02/2021

|

15/02/2021

|

|

Audit

and Risk Committee meeting

|

4 June

2021

|

|

Audit

and Risk Committee meeting

|

4 June

2021

|

21.2.5 Audit

NZ Interim Report on the audit of the 2021-31 Long-term Plan Consultation

Document

Doc ID: 533836

1. Purpose

To receive Audit NZ’s Report to Council on the audit

of the 2021-31 Long-term Plan Consultation Document.

|

Recommendations

That the report be received.

|

2. Discussion

Central Otago District Council is in the

process of completing the 2021-31 Long-term Plan. The first stage is the

preparation of the Consultation Document and the supporting information behind

this. These documents are audited ahead of Council going out to

consultation. A second audit will commence 8 June, in which Audit NZ

audits the final 2021-31 Long-term Plan.

Audit NZ issued an unmodified audit report

on 24 March 2021. This included an emphasis of a matter regarding the

Government’s intention to make three waters reform decisions during 2021

and acknowledging the long term uncertainty of what this means to Council.

The report details the areas of focus and

these can be found in section 3 and 4 of the report. There appeared to be

no areas of concern raised by Audit New Zealand.

The next steps in the final audit of the

2021-31 Long-term Plan, is a tight turnaround of information as deliberations

are proposed to end 3 June 2021, leaving two working days to complete the LTP

book ahead of Audit NZ’s arrival on 8 June 2021. While council

staff are forward-planning as much as possible, there is a possibility that the

quality review ahead of 8 June audit commencement may be inadequate due to

resourcing and time constraints. The final LTP will be reviewed by the

executive team while Audit NZ is on site.

3. Attachments

Appendix 1 - Audit NZ - Management

Report for LTP Consultation Document - July 21 to 30 June 31 ⇩

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Leanne

Macdonald

|

Sanchia

Jacobs

|

|

Executive

Manager - Corporate Services

|

Chief

Executive Officer

|

|

12/05/2021

|

24/05/2021

|

|

Audit

and Risk Committee meeting

|

4 June

2021

|

21.2.6 Risk

Management Update

Doc ID: 534566

1. Purpose

To consider the Risk Management update.

|

Recommendations

That the report be received.

|

2. Discussion

The Strategic Risk Register remains under development. Four

workshops have been undertaken with the Executive Team, determining the top

strategic risks which the organisation faces. It is expected that the completed

Strategic Risk Register will be presented at the October 2021 Audit and Risk

meeting.

3. Attachments

Nil

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Gabi

McFarlane

|

Leanne

Macdonald

|

|

Risk and

Procurement Manager

|

Executive

Manager - Corporate Services

|

|

18/05/2021

|

24/05/2021

|

21.2.7 Financial

Reserves Policy

Doc ID: 534573

1. Purpose

of Report

To consider and provide feedback on the draft Financial

Reserves Policy before submitting to Council for consideration at their 30 June

meeting.

|

Recommendations

That the Audit and Risk Committee

A. Receives

the report and accepts the level of significance.

B. Review

and provide feedback on the draft Financial Reserves Policy.

C. Note

the Financial Reserves Policy will be considered at the Council 30 June

meeting.

|

2. Background

Council has a long record of managing financial reserves in

a financially prudent manner that promotes and protects the current and future

interests of the community.

Council is required to maintain a range of financial

reserves and has chosen to create other financial reserves for the purpose of

separately managing funds. Over time these funds have accumulated and now

total significant sums. It is therefore important that they are managed

consistently, accurately, and transparently.

A draft Financial Reserves Policy (refer appendix 1) has

been created to provide guidance to council staff so they are able to manage

reserves consistently, accurately and transparently with clearly defined

parameters.

3. Discussion

Council staff seek to manage the reserves in a clear and

transparent manner, to enable elected members comfort when authorising the use

of these reserves. The reserves form part of the end of year annual

report audits.

Reserves serve as a “rainy day fund” to lessen

the impact on rates or to fund unplanned, additional, or delayed programmes of

work as per Council or community board resolutions. Whether reserves have

accumulated by way of under-spending of an activity in a specific year or

collected for a specific targeted activity (such as an emergency event), the

expectation applies that the use of the reserves is in a consistent manner that

supports the initial intention behind the collection of the income relating to

the activity it has originated from.

This policy will give staff guidance when seeking permission

to use these funds to support operational and capital expenditure in the later

years and ensure that the use of these funds reflects the intent behind the

collection of these reserves, while offering transparency in the use of these

funds.

4. Options

Option 1 – (Recommended)

The Committee shall provide feedback to be incorporated into

the draft Financial Reserves Policy before its taken to Council for adoption.

Advantages:

· Maintain

a consistent approach to the review of policies

· Complies

with the Committee’s expectation of their role in policy overview

· Supports

the intention to maintain transparency, consistency, and accurate management of

reserve funds

· Protects

Council reputation

· Supports

the community’s expectation that council will use funds for the intention

that they were collected for.

Disadvantages:

· None

identified.

Option 2

Do not provide feedback and recommend to Council the

Financial Reserves policy for adoption.

Advantages:

· None

Disadvantages:

· A

lack of policy causes confusion at times when determining how and when to use

reserves.

· A

lack of understanding across Council as to when to use reserves and for which

purpose when requiring additional support to fund for operational and capital

expenditure in years when funding is not available.

· Inconsistencies

in the recording of such reserves may not balance with the expectation of staff

or elected members when seeking to use or when approving the use of specific

reserves.

· Lack

of guidance to council staff

· Staff

may seek to rate unnecessarily for activities that have appropriate reserves.

5. Compliance

|

Local Government Act 2002 Purpose Provisions

|

This decision enables democratic local decision making and action

by, and on behalf of communities through the annual planning and reporting

process.

AND

This decision promotes the economic well-being of communities, in

the present and for the future by prudently managing the financial reserves

of the Council on their behalf.

|

|

Financial implications – Is this decision consistent with

proposed activities and budgets in long term plan/annual plan?

|

The financial implications of this new policy have been considered

and is consistent with the proposed activities contained within the long-term

and annual planning processes.

|

|

Decision consistent with other Council plans and policies? Such as

the District Plan, Economic Development Strategy etc.

|

Other council policies and plans have been considered when

creating this policy.

|

|

Considerations as to sustainability, the environment and climate

change impacts

|

There are no implications.

|

|

Risks Analysis

|

Whilst there is no current policy to consider, this new policy

supports best practice with no known risks.

|

|

Significance, Consultation and Engagement (internal and external)

|

No consultation is required in the creation of this policy.

There are no significant issues arising from this new policy and

should not generate media or community interest.

|

6. Next

Steps

This policy will be taken to Council for

adoption, with recommended amendments (if any). Staff will be notified of

the update and uploaded on the Council website.

7. Attachments

Appendix 1 - Financial Reserves

Policy ⇩

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Leanne

Macdonald

|

Sanchia

Jacobs

|

|

Executive

Manager - Corporate Services

|

Chief

Executive Officer

|

|

21/05/2021

|

24/05/2021

|

|

Audit

and Risk Committee meeting

|

4 June

2021

|

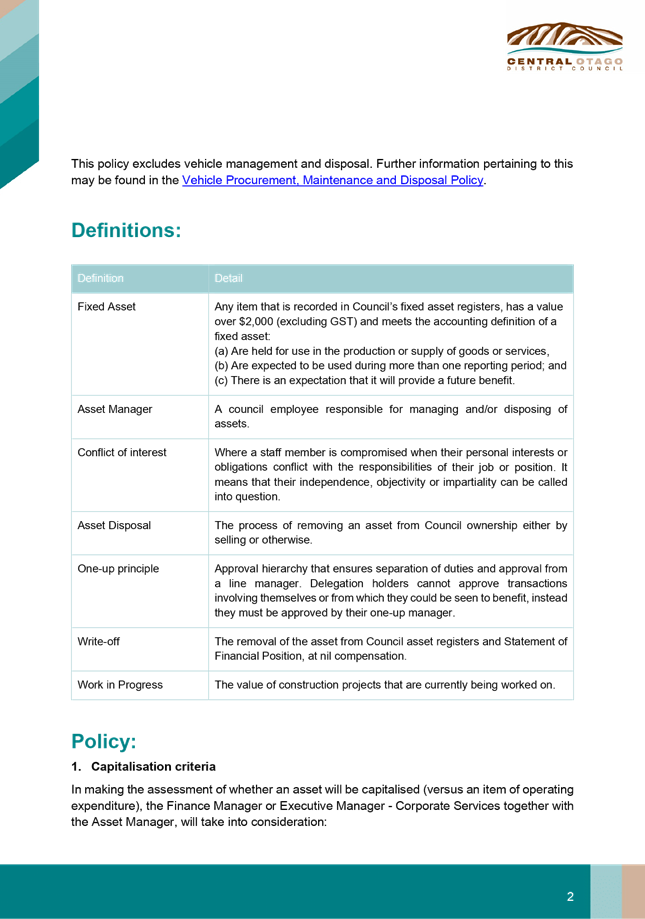

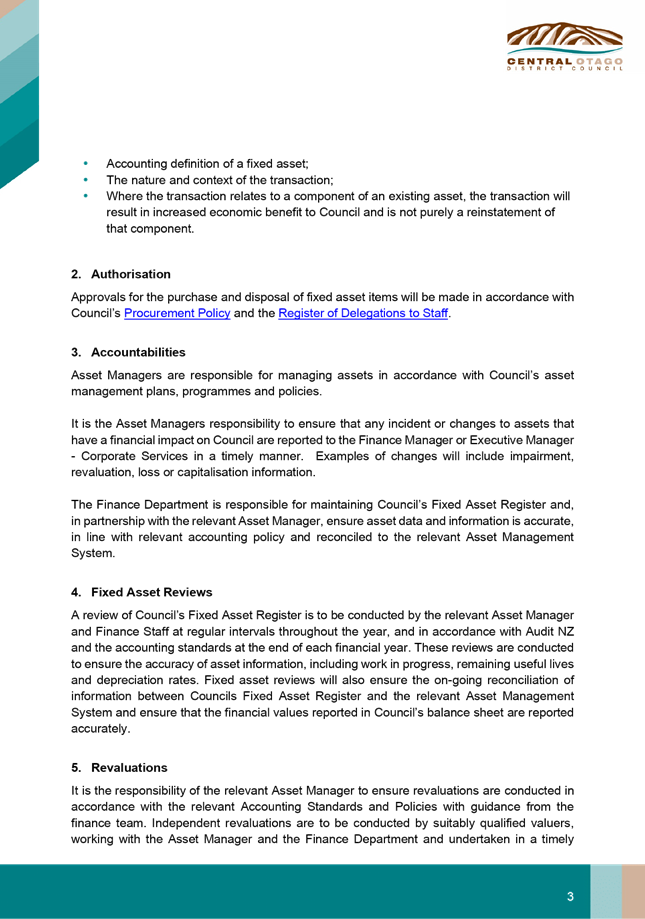

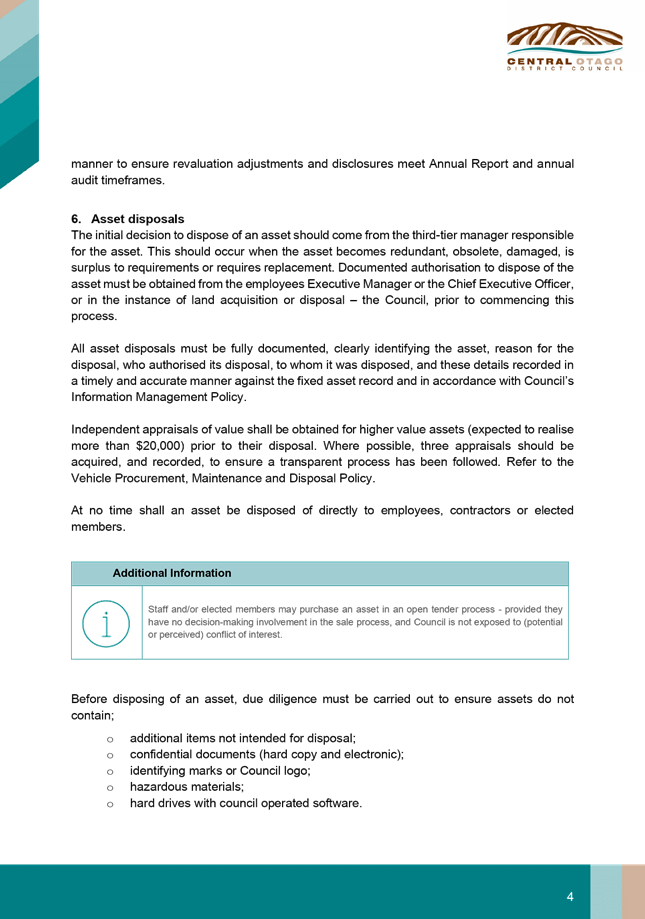

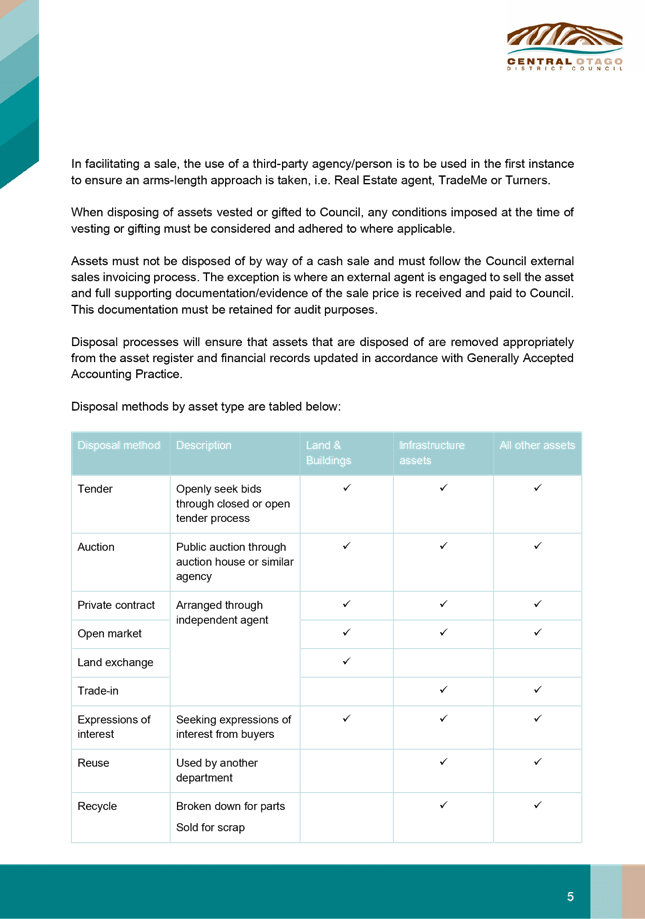

21.2.8 Fixed

Asset and Disposal Policy

Doc ID: 535074

1. Purpose

of Report

To consider and provide feedback on the draft Fixed Asset

and Disposal Policy before requesting that the Chief Executive approves this

policy for council staff use.

|

Recommendations

That the Audit and Risk Committee

A. Receives

the report and accepts the level of significance.

B. Review

and provide feedback on the draft Fixed Asset and Disposal policy.

C. Note

the draft policy, with any amendments, will be signed-off by the Chief

Executive and issued to staff for implementation.

|

2. Background

Council and staff have a requirement to manage all assets in

a fiscally responsible manner that best protects the community’s

interest.

Council assets make up a significant component of the

council’s balance sheet. The value of these assets is audited on an

annual basis. It is therefore important that they are managed

consistently, accurately, and transparently.

A draft Fixed Asset and Disposal

Policy (refer appendix 1) has been created to provide guidance to council

staff, so they are able to appropriately manage assets with clearly defined

parameters, particularly when disposing of assets.

3. Discussion

Council staff seek to manage and dispose of assets in a

clear and transparent manner. Staff also aim to maximise the life of assets and

minimise the cost to rate-payers for managing and disposing of these

assets. It is important when disposing of assets to protect the

reputation of staff and Council through a transparent, arms-length disposal

process. This also gives the community an assurance that their assets are

being managed to best protect their interests.

This policy seeks to provide assurance across a wide group

of stakeholders.

4. Options

Option 1 – (Recommended)

The Committee provides feedback to be considered and

incorporated into the draft Fixed Asset and Disposal Policy before Chief

Executive sign-off.

Advantages:

· Maintain

a consistent approach to the review of policies

· Complies

with the Committee’s expectation of their role in policy overview

· Supports

the intention to maintain transparency, consistency, and fiscally responsible

management and disposal of council assets

· Protects

Council and staff reputation

· Supports

the community’s expectation that council will manage council assets on

their behalf in a fiscally responsible and ethical manner

· Meets

Audit New Zealand’s expectations and supports the annual reporting

process.

Disadvantages:

· None

identified.

Option 2

Do not recommend to the Chief Executive the Fixed Asset and

Disposal Policy for sign-off.

Advantages:

· None

Disadvantages:

· Council

assets may be disposed of in a manner that could cause reputational harm to

council

· The

selling of assets if not managed in a transparent manner, with the appropriate

arm-length process could result in council receiving a lower price than the

asset is worth

· A

potential lack of confidence by the community and by Audit NZ

· Council

staff do not meet the Committee’s expectations in the deliverance of a

policy

· There

is a risk that the management and subsequent disposal of council assets may not

be consistent with best practice and council expectations

· Risk

of reputational harm to council and staff

· Lack

of guidance to council staff

· The

rate-paying community may not have confidence in council’s management of

rate-funded asset

· Challenges

in meeting Audit New Zealand’s expectations and receiving an annual

report clearance.

5. Compliance

|

Local Government Act 2002 Purpose Provisions

|

This decision enables democratic local decision making and action

by, and on behalf of communities through the annual planning and reporting

process.

AND

This decision promotes the economic well-being of communities, in

the present and for the future by prudently managing the assets of the

Council on their behalf.

|

|

Financial implications – Is this decision consistent with

proposed activities and budgets in long term plan/annual plan?

|

The financial implications of this new policy have been considered

and is consistent with the proposed activities contained within the long-term

and annual planning processes.

|

|

Decision consistent with other Council plans and policies? Such as

the District Plan, Economic Development Strategy etc.

|

Other council policies and plans have been considered when

creating this policy.

|

|

Considerations as to sustainability, the environment and climate

change impacts

|

There are no implications, as the asset management plans consider

the implications to sustainability, environment and climate change impacts.

|

|

Risks Analysis

|

This new policy supports best practice and through the policy

mitigates the risk of reputational and fiscal harm to Council, staff and the

community.

|

|

Significance, Consultation and Engagement (internal and external)

|

No consultation is required in the creation of this policy.

There are no significant issues arising from this new policy and

should not generate media or community interest.

|

6. Next

Steps

This policy will be taken to Chief

Executive for sign-off with recommended amendments (if any). Staff will

be notified of the update and the policy will be uploaded on the Council

intranet.

7. Attachments

Appendix 1 - Draft Fixed Asset and

Disposal Policy ⇩

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Leanne

Macdonald

|

Sanchia

Jacobs

|

|

Executive

Manager - Corporate Services

|

Chief

Executive Officer

|

|

21/05/2021

|

24/05/2021

|

|

Audit

and Risk Committee meeting

|

4 June

2021

|

21.2.9 Financial

Report for the period ending 31 March 2021

Doc ID: 531295

1. Purpose

To consider the financial performance for the period

ending 31 March 2021.

|

Recommendations

That the report be received.

|

2. Background

The Committee has requested regular financial updates.

3. Financial

Reporting

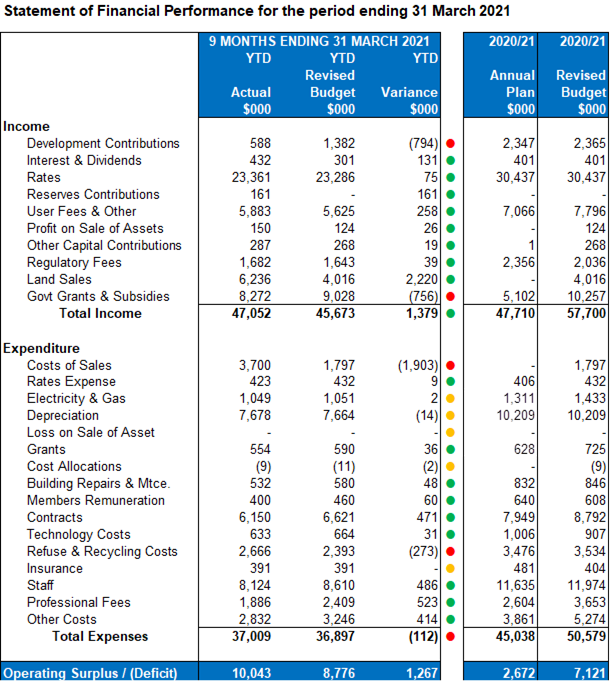

March 2020-21 YTD operating surplus is $10.04M and is

largely the result of external funding received for the Three Waters reform and

land sales. The activity managers have reforecast their budgets in

February 2021 based on year-to-date actuals as of 31 December 2020. This

forecast was approved by Council in March and subsequently the revised budget

has been updated to incorporate the forecast.

i. Land

sales of $6.2M which relates to the Gair Avenue development and Cemetery

Road/Harvest Road creating a $2.2M positive variance in income. This income is

partly offset by $3.7M of costs that council has incurred including developer

costs and profit-sharing costs.

ii. Funding

received for the Three Waters reform is $4.73M.

iii. Expenditure

is higher than budget by $112k attributed to a late settlement of Harvest Road

from 2018 as well as refuse and recycling costs.

Attached to this report is the Council financial report

presented in March 2021, which includes a variance analysis against the general

ledger profit and loss statement, plus an activity level variance (Appendix 1).

The report also details the expenditure of the capital

works programme across activities to enable oversight on progress of these

projects.

4. Accounts

Receivable

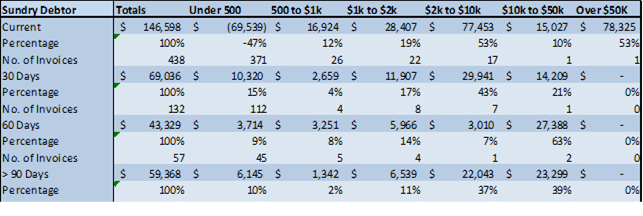

As of 31 March 2021, council had $59k outstanding in

accounts receivables greater than 90 days. Resource consents are the key

contributors and include:

The Canyon Vineyard $13.3k (objections to fees heard by

hearings panel)

M N Shaw $8.5k (awaiting payment options)

Other includes:

ZK – RMH Trust $10k (dispute relating to airport

rental)

Top Shelf Productions $5.7k (agreement to fund people on

Bikes Series 2)

Debt is

actively managed and monitored and if a debtor is past our three-month

threshold, their information is sent to our debt collection agency, Receivables

Management Limited.

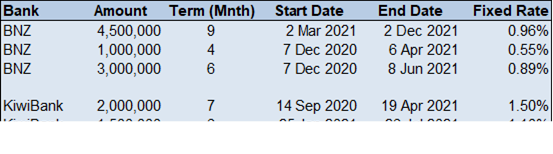

5. Investment

As at 31 March 2021, Council had cash balances of $13.5M,

of which term deposits of $6M mature within 90 days.

Weighted average interest rates for all council term

deposits is 1.02%.

6. Internal

Loans

Forecast closing balance for 30 June 2021 is

$4.270M.

7. External

Community Loans

The total amount of external loans at the beginning of the

financial year 2020-21 was $241k and as of 31 March 2021, the outstanding

balance was $202k. Council has received $38k in principal payments and $9.3k in

interest payments.

|

Owed By

|

Original Loan

|

1 July 2020 Actual

Opening Balance

|

Principal

|

Interest

|

31 Mar 2021 Actual

Closing Balance

|

|

Cromwell College

|

400,000

|

164,184

|

24,877

|

6,711

|

139,306

|

|

Maniototo Curling

|

160,000

|

48,743

|

9,750

|

1,666

|

38,993

|

|

Oturehua Water

|

46,471

|

28,122

|

4,098

|

1,004

|

24,024

|

|

|

606,471

|

241,049

|

38,725

|

9,381

|

202,324

|

8. Attachments

Appendix 1 - Financial Report for

the period ending March 2021 ⇩

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Kim

McCulloch

|

Leanne

Macdonald

|

|

Corporate

Accountant

|

Executive

Manager - Corporate Services

|

|

14/05/2021

|

14/05/2021

|

|

Audit

and Risk Committee meeting

|

4 June 2021

|

ATTACHMENT 1

AUDIT

& RISK COMMITTEE – FINANCIALS FOR THE PERIOD ENDING 31 MARCH 2021

This table has rounding (+/- 1)

The

financials for March 2021 show an overall favourable variance of $1.26M. The

main driver is in land sales at $2.2M being the delayed settlement of the

Cemetery Road/Harvest Road land sale from 2018.

Overall income has a favourable variance

against the revised budget of $1.3M. This relates to the above delayed

settlement of Cemetery Road/Harvest Road.

Expenditure has an unfavourable variance

of ($112k). The main drivers behind the unfavourable variance is the cost of

sales related to the delayed settlement of Cemetery Road/Harvest Road, and

refuse and recycling costs. Offsetting this is favourable variance are

contracts, staff, professional fees, and other costs.

Income of $47.052M against the

year-to-date budget of $45.673M

The main variances are:

· Development

contributions has an unfavourable variance of ($794k). Lower than expected

contributions are linked with the timing of developments in Cromwell and

Alexandra with the balance in district roading. It should be noted that $417k

has been received from two developments in April 2021.

· Government

grants and subsidies revenue of $8.27M is ($756k) unfavourable against budget. The unfavourable variance is due the timing of the Waka

Kotahi New Zealand Transport Agency (Waka Kotahi) roading subsidy. These

subsidies are claimed based on the roading work programme. The capital roading

work programme is running behind schedule largely due to the timing of the

Clyde Heritage Precinct project.

· Interest

and dividends revenue is favourable against budget by $131k. This is partly due

to interest received from the delayed settlement of Cemetery Road offset by

lower interest rates received on term deposit investments.

· Reserves

contributions has a $161k favourable variance. These contributions are

dependent on developers’ timeframes and therefore difficult to gauge when

setting budgets.

· User

fees and other of $5.8M is $258k favourable against budget. Contributing to the

favourable variance is a Ministry of Business Innovation and Employment (MBIE)

tourism grant for freedom camping, fencing and toilets of $48k, which is in

addition to $95k received earlier in the financial year. Other areas with

favourable variances include planning (regulatory) income of $98k and property

rental and hire income of $44k from Murray Terrace.

Expenditure of $37M against

the year-to-date budget of $36.89M

The main variances are:

· Costs

of sales of $3.7M is above budget by ($1.9M). As mentioned earlier this relates

to the delayed settlement of Cemetery Road/Harvest Road from 2018.

· Refuse

and recycling costs of $2.66M has an unfavourable variance of ($273k).

This is mainly due to the timing of the Central Otago District Council emission

trading scheme contribution of ($277k), the budget is reflected in May 2021.

· Contracts

of $6.15M is $471k favourable against budget. The main favourable variances are

planned maintenance of $127k, district-wide un-subsidised roading work of $103k

and subsidised roading work of $231k. As with income, the capital roading

programme is running behind schedule due to the timing of the Clyde Heritage

Precinct Project.

· Staff

costs of $8.124M has a $486k favourable variance against budget. This relates

to the timing of vacant positions and positions that are in the process of

being recruited.

· Professional fees of $1.87M is $523k favourable against the

budget. This is due to the timing of professional fees within the District Plan

along with the timing of management consultant fees in water and wastewater.

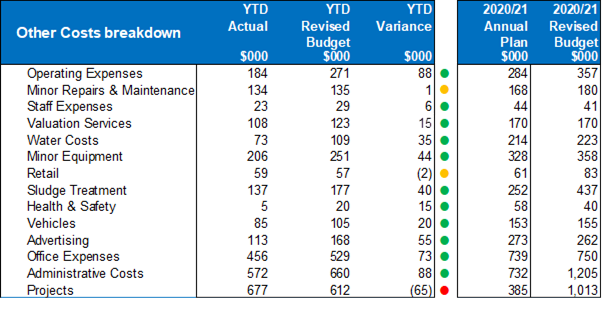

Other

costs breakdown is as below:

This table has rounding (+/- 1)

This table has rounding (+/- 1)

· Operating expenses

are $88k favourable against budget. This is largely due to underspends in

waste water operations.

· Advertising and

office expenses are $128k favourable. This is largely due to underspends

across the organisation.

· Administrative

costs are $88k favourable. This is largely due to an underspend in weed

control and compliance schedules.

· Projects are

($65k) unfavourable against budget. This variance is mainly due to Three Waters

reactive maintenance expenses from the January 2021 flood of ($170k). This

expense is still to be adjusted to reflect the resolution of 21.2.14, January

2021 Weather event – water report. In this resolution it was agreed to

allow for an increase in expenditure as opposed to using the Emergency Event

Reserve. This is offset by underspends in operating projects like the Community

Development MBIE projects, Regional Identity Branding project and Road Safety

projects.

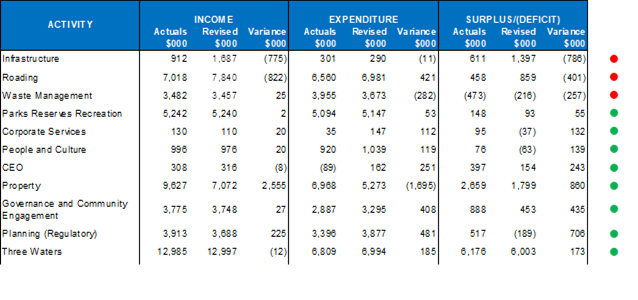

Profit and Loss by Activity -

31 March 2021

This table has rounding (+/- 1)

* The funding activity has

been removed as this is not an operational activity.

· Infrastructure

– income has an unfavourable variance of ($775k). This variance is due to

development contributions received being lower than budgeted. Lower than

expected contributions are linked with the timing of subdivision developments

in Cromwell and Alexandra. It is expected that development contribution income

will remain lower than budget due to subdivision developments being pushed into

the next financial year. Expenditure is over budget by $11k.

· Roading

– income has an unfavourable variance of ($822k). This is predominately

due to the Waka Kotahi subsidy, which moves in tandem with subsidised roading

expenditure, which is favourable $421k. Both are due to the timing

of the capital work programme which is running behind schedule largely due to the

Clyde Heritage Precinct Project.

· Waste

Management - income has a favourable variance of $25k. This is mainly due to

the timing of green waste income. Expenditure has an unfavourable variance of

($282k). This is mainly due to the timing of the Central Otago District Council

emission trading scheme contribution of ($277K).

· Parks

and Recreation – the favourable income variance relates to the MBIE

tourism grant of $48k received and updated in the revised budget. Expenditure

has a favourable variance of $53k. This relates to a contestable grant for

trail maintenance, that is subject to funding applications being

received.

· Corporate

Services – income has a favourable variance of $20k. This is due to

profit on the sales of vehicle assets. Expenditure is $112k lower than budget

mainly due to the timing of information services operating expenditure.

· People

and Culture – income has a favourable variance of $20k driven by a grant

received from New Zealand Libraries Partnership Programme. Expenditure has a favourable

variance of $119k. Driving this favourable variance are underspends in Human

Resources $46k, Health and Safety $42k and Administration $30k.

· CEO

– Expenditure has a favourable variance of $251k which is mainly due to

the Strategic Pay allocation which by end of year should be reflected in

increased costs across the organisation, as the pay review impacts across the

activities.

· Property

– favourable income of $2.5M relates to the delayed settlement on

Cemetery Road from 2018. Expenditure is unfavourable due to the costs

associated with this delayed settlement.

· Governance

and Community Engagement – income has a favourable variance of $27k due

to grants received in tourism. Expenditure has a favourable variance of $408k.

This is due to underspends in promotions and tourism $135k, governance $90k,

economic development $81k, community development $63k, visitor centres $39k and

regional identity $10k.

· Planning

(Regulatory) – has a favourable income variance of $225k, this is mainly

due to the recovery of costs incurred from external professionals related to

resource consents and an increase in building permit revenue. The favourable

expenditure variance of $481k is due to lower-than-expected staff costs and

planning consultant (review) fees with further work required to progress the District Plan programme.

· Three

Waters – income has an unfavourable variance of ($12k). This is due to

lower revenue from septage fees. Expenditure has a favourable variance of $185k

due to lower-than expected management consultants and operating costs.

Capital Expenditure

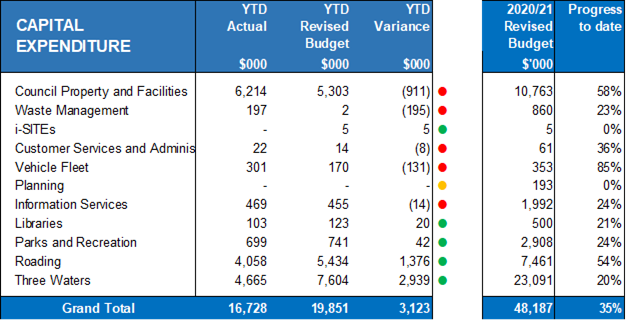

Year-to-date, 35% of the total capital spend against the full

year’s revised capital budget, has been expensed.

Council Property and Facilities ($911k) unfavourable

against budget:

This includes the purchase of

Murray Terrace land approved by the Cromwell Ward in December 2020, which

Council authorised as per resolution 20.40.3 in July 2020.

Waste Management

($195k) unfavourable against budget:

This variance is due to the progression of the glass crushing

plant project, which Council authorised as per resolution 20.7.31 in August

2020.

Vehicle Fleet ($131k) unfavourable

against budget:

Vehicle replacements are tracking well against the full year

budget. At the end of April all vehicles have been purchased and should be

delivered by the end of the year, and remain within the full-year budget.

Information Services ($14k) unfavourable against

budget:

Records digitisation staff costs have been allocated to the

project after the forecast creating an unfavourable variance, this will smooth

out as the budget is released over the remainder of the year.

Libraries $20k favourable against budget:

Small favourable variance relating to the timing of library

book and e-book purchases.

Parks and Recreation $42k

favourable against budget:

Parks and recreation have a favourable variance due to

projects in cemeteries where contracts have been awarded in April with

completion date expected to be end of June.

Roading $1.3M favourable against budget:

Subsidised roading projects are behind, this is mainly due to

delays to the capital programme. A month in the work programme has been lost

due to the flooding event in January 2021.

Three Waters is $2.9M favourable against budget:

The favourable variance is due to the timing of construction

projects. The main drivers include the Cromwell and Omakau water supply

improvements and the Clyde wastewater reticulation network construction.

Internal Loans

Forecast closing balance for 30 June 2021 is $4.27M.

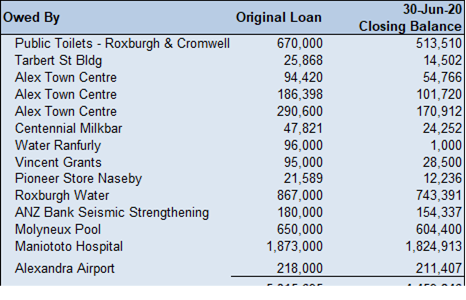

|

OWED BY

|

Original Loan

|

1 July 2020

Opening

Balance

|

30 June 2021 Forecast

Closing Balance

|

|

Public Toilets -

Roxburgh & Cromwell

|

670,000

|

513,510

|

491,239

|

|

Tarbert St Building

|

25,868

|

14,502

|

13,067

|

|

Alexandra Town Centre

|

94,420

|

54,766

|

49,759

|

|

Alexandra Town Centre

|

186,398

|

101,720

|

91,041

|

|

Alexandra Town Centre

|

290,600

|

170,912

|

155,412

|

|

Centennial Milkbar

|

47,821

|

24,252

|

21,284

|

|

Vincent Grants

|

95,000

|

28,500

|

19,000

|

|

Pioneer Store Naseby

|

21,589

|

12,236

|

10,949

|

|

Roxburgh Water

|

867,000

|

743,391

|

717,829

|

|

ANZ Bank Seismic

Strengthening

|

180,000

|

154,337

|

149,030

|

|

Molyneux Pool

|

262,000

|

604,000

|

571,900

|

|

Maniototo Hospital

|

1,873,000

|

1,824,913

|

1,775,142

|

|

Alexandra Airport

|

218,000

|

211,407

|

204,485

|

|

Total

|

4,831,696

|

4,458,446

|

4,270,137

|

External Loans

The total amount of external loans

at the beginning of the financial year 2020-21 was $241k and as at 31 March

2021 the outstanding balance was $202k. Council has received $38k in principal

payments and $9.3k in interest payments.

21.2.10 Policy

and Strategy Register

Doc ID: 534537

1. Purpose

of Report

To present an updated register of the Council’s

policies and strategies.

|

Recommendations

That the Audit and Risk Committee

A. Receives

the report.

|

2. Background

The Register has been updated to be correct as at 26 May

2021.

Since the last meeting of the Committee, the Waste

Management and Minimisation Bylaw and Community Development Strategy have been

adopted.

The following changes have been made as a result of

legislative complexity and prioritisation of workloads:

People and Culture

· Staff

Interests Policy checked and still on track for July 2021. Is a soft refresh

and won’t go to Committee

· Leave

Management Policy is not due until December 2023 but is being updated early to

reflect changes to legislation

· Performance

Management Policy is in the final stages and expected to be completed in May

2021

Information Services

· Information

Management Policy updated to June 2021

· Privacy

Policy updated to October 2021

· LGOIMA

Policy updated to October 2021

· Digital

Strategy updated to June 2022

Parks and Property

· Molyneux

Pool CCTV Policy updated to late 2021

Regulatory

· Enforcement

Strategy delayed due to staff change. Currently assessing likely timeframe and

will update at next meeting.

Environmental Engineering

· Water

Bylaw changed from expected July 2021 to December 2022 due to Three Waters

Review process

· Water

Policy changed from expected July 2021 to December 2022 due to Three Waters

Review process

· Sewer

Lateral Policy will be reviewed with Three Waters work for December 2022.

Roading

· Speed

Limit Bylaw expected in July 2021

Community and Engagement

· Museum

Strategy stage one completion changed to June 2021. The final draft is

currently with the sector for review.

Finance

· Asset

Disposal Policy has been renamed Fixed Asset and Disposal Policy. It will be

considered at this meeting.

· Protected

Disclosures (Whisteblowing) Policy updated to October meeting.

General

· 30

Year Vision has been put on hold and staff workload reprioritised to focus on

the Council vision/organisational strategy.

3. Attachments

Appendix 1 - Policy and Strategy

Register ⇩

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Alix

Crosbie

|

Saskia

Righarts

|

|

Senior

Strategy Advisor

|

Chief

Advisor

|

|

26/05/2021

|

26/05/2021

|

|

Audit and Risk Committee meeting

|

4 June 2021

|

6 Reports

for Information

21.2.11 Tourism

operator compliance records

Doc ID: 535124

1. Purpose

To give an overview of a known new compliance issue and

actions taken to remedy.

|

Recommendations

That the report be received.

|

2. Discussion

It has recently come to the attention of staff that council

run i-SITEs had no mechanisms in place to ensure tourism operators they are

on-selling have up to date compliance certifications.

The previous process had seen all businesses that paid to be

promoted through a council run i-SITE required to supply evidence of their

compliance relevant to their operation at the point of sign up. There was never

a mechanism established to ensure that as certifications lapsed, the operator

supplied updated documentation.

In the past this may have been acceptable given ultimate

responsibility lies with the operator to be compliant and carry the correct

certifications. However, in light Worksafe bringing charges against both the

tourism operators and the third parties who sold tours to Whakaari (White

Island), i-SITEs as a reseller also carry responsibility to ensure the products

they are on-selling have relevant certifications.

In May 2021, staff contacted all partner tourism operators

they sell and asked for evidence of compliance. That evidence will be

catalogued and a date for follow up noted when certifications are due to

expire. All businesses have been advised that after the 30th of June

2021 should i-SITEs not have received the requested evidence, council run

i-SITEs will no longer be able to resell their product.

Staff will continue to assess the outcome of the Whakaari

tragedy court proceedings and adjust future processes to align with the

court’s findings.

3. Attachments

Nil

|

Report

author:

|

Reviewed

and authorised by:

|

|

|

|

|

Dylan

Rushbrook

|

Sanchia

Jacobs

|

|

General

Manager Tourism Central Otago

|

Chief

Executive Officer

|

|

21/05/2021

|

24/05/2021

|

21.2.12 Update

on progress of the Lake Dunstan Water Supply and Clyde Wastewater Reticulation

Projects

Doc ID: 534575

1. Purpose

To provide an update on progress of the Lake Dunstan Water

Supply Project and the Clyde Wastewater Reticulation Project.

|

Recommendations

That the report be received.

|

2. Background

The Lake Dunstan Water Supply Project involves extending the

existing borefield above Clyde, constructing a new water treatment plant and

piping treated water to the Alexandra Northern reservoir and the Clyde

reservoir.

Construction of the pipeline between Alexandra and Clyde is

complete.

Final design of the borefield extension, and treatment plant

is underway which will then enable construction to commence. The finished

project will meet the requirements of the New Zealand Drinking Water Standards.

The Clyde Wastewater Reticulation Project

involves construction of a reticulated wastewater scheme in the Stage 1 area of

Clyde, connection of over 200 properties and construction of a pump station and

pipeline to the Alexandra wastewater treatment plant. The pipeline

between Clyde and the Manuherekia River is complete.

Budgets

The budget for the remaining work on the Lake Dunstan Water

Supply Project is t $9.2M. The budget for

construction of Stage 1 of the Clyde Wastewater Reticulation is $8.5M.

Programme

More detail is provided in the appended project reports.

Lake Dunstan Water Supply:

|

Project

Stage

|

Expected

Completion Date

|

|

Agree

contract terms

|

May

2021

|

|

Detailed

Design, updating estimate and creating delivery programme.

|

June

– October 2021

|

|

Review

design estimate against Council budget.

|

October

2021

|

|

Construction

of Water Treatment Plant, balance rank and bore field

|

November

2021 – June 2022

|

|

Commission

new Lake Dunstan Water Supply Scheme

|

Mid

2022

|

Clyde Wastewater Reticulation Stage 1:

|

Project

Stage

|

Expected

Completion Date

|

|

Construction commenced.

|

January

2021

|

|

Main

pipelines

|

January

2021 – February 2022

|

|

Laterals

from mains to properties

|

June

2021 – May 2022

|

|

“Winter